Jordan earns $85,000 a year as a graphic designer — the product of the rates Jordan charges. Here is where every Adobe charge, the Cintiq, the font licenses, and the client print invoices actually go on Schedule C, line by line.

Jordan is a graphic designer in Austin. Last April, Jordan’s Schedule C had one real expense line filled in: about $14,000 dumped into Line 22, “supplies.” The Cintiq, the Adobe subscription, the printer invoices, the Upwork fees, all of it in one box. The return went through fine. It also left money on the table by skipping the deductions designers routinely miss, including the home office. The single-line return also would have been hard to defend if the IRS asked questions.

We already walked Maya, a freelance writer making $68,000, through every line on the main Schedule C instructions guide. Design changes which lines matter. A writer rarely buys a $3,499 pen display or fronts a print run for a client. You do. This is the designer version, built around Jordan’s actual $85,000 year, and it sits alongside the rest of our freelancer finance guides.

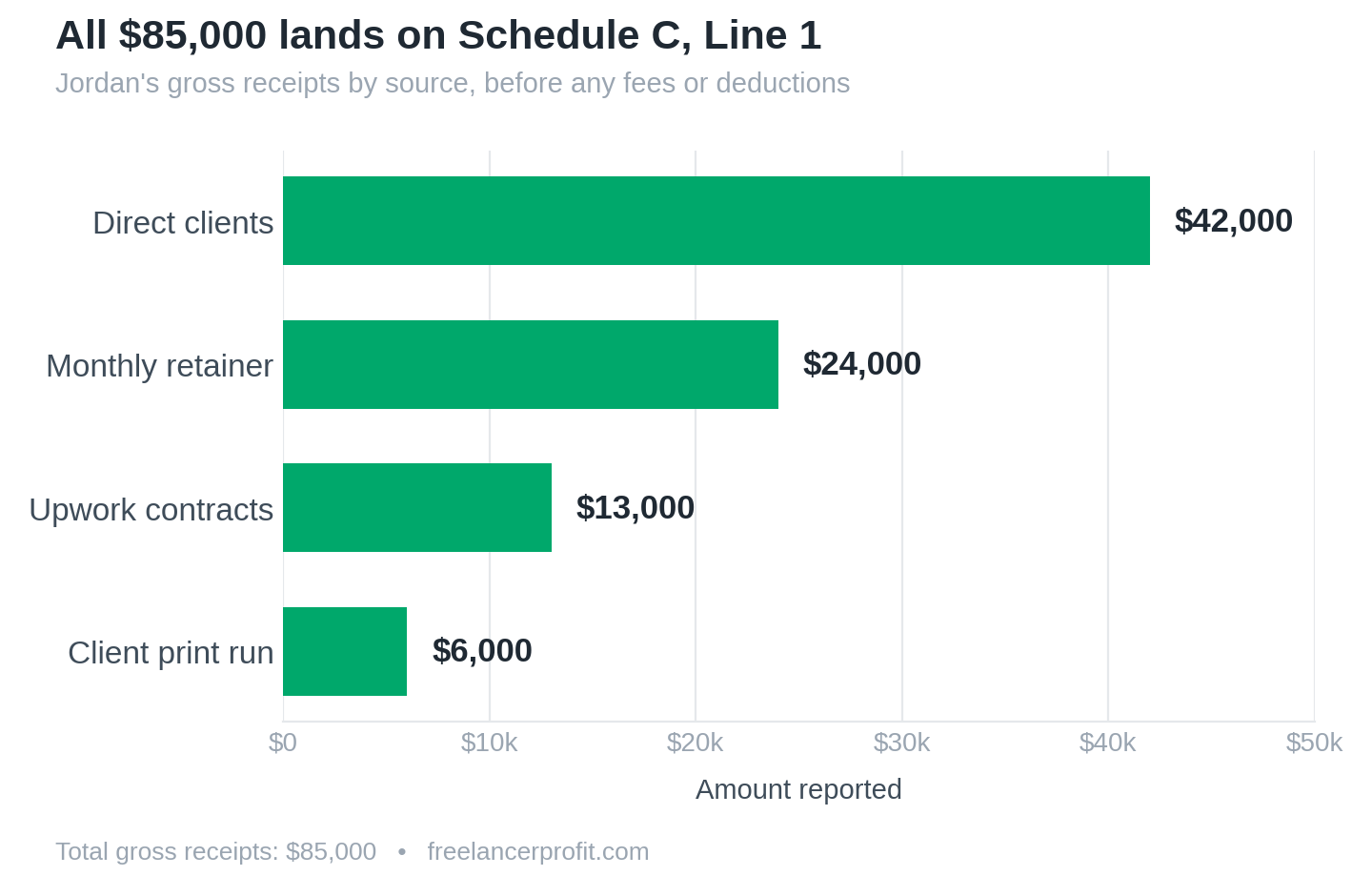

How $85,000 from four sources lands on Line 1

Jordan’s income came in four ways last year. Direct clients paid $42,000. A monthly retainer brought $24,000 at $2,000 a month. Upwork contracts added $13,000 before Upwork took its cut. One client paid $6,000 for a print run Jordan arranged through a local printer. That totals $85,000, and all of it goes on Line 1, gross receipts — which is exactly the total a good invoicing tool should hand you at year end.

You report the total regardless of which forms show up. Direct clients send a 1099-NEC if they paid you $600 or more. Upwork issues a 1099-K only if you clear $20,000 and 200 transactions, the federal threshold the One Big Beautiful Bill Act restored for 2025 after years of lower limits (see the 1099 threshold update). At $13,000, Jordan gets no 1099-K from Upwork at all. Line 1 is still $85,000. A missing form does not make the income disappear.

Upwork’s freelancer service fee is not income you keep, so it comes back out on Line 10, commissions and fees. Upwork dropped its flat 10 percent fee in May 2025 for a variable rate between 0 and 15 percent set per contract, though most designers still land near 10 percent. Jordan’s contracts averaged about 10 percent, so roughly $1,300 comes off the $13,000. PayPal and Stripe processing fees sit on the same line, and they are easy to miss because the money never reaches your account.

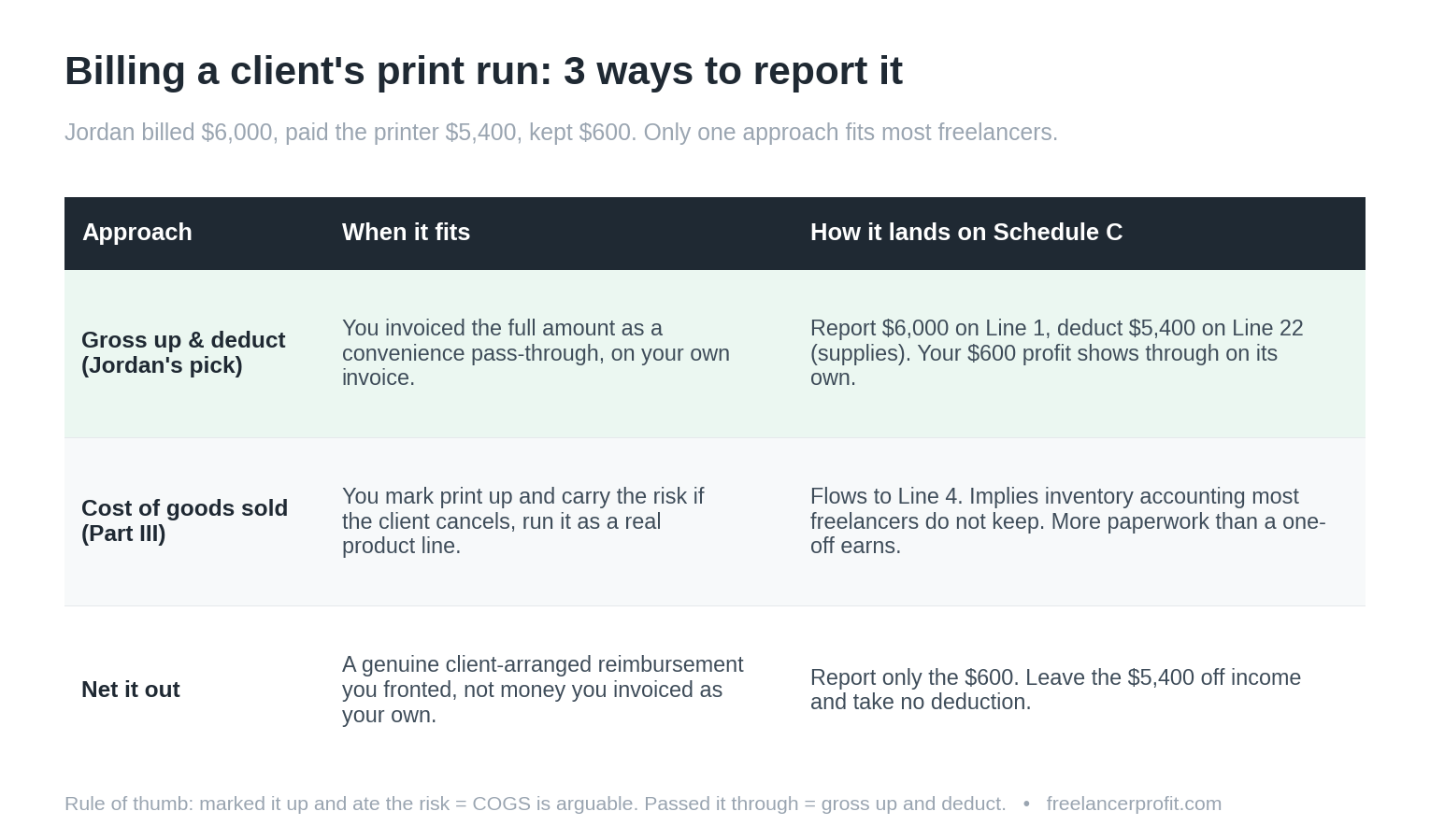

Do I report the full print amount or just my markup?

This trips up almost every designer who handles print. Jordan billed the client $6,000 and paid the printer $5,400, keeping $600. There are three ways to treat it, and only one of them is wrong for most people.

- Gross up and deduct (what Jordan did). Report the full $6,000 on Line 1, deduct the $5,400 printer cost on Line 22, supplies. Your real $600 profit shows through on its own. Simple, defensible, matches how the invoice read.

- Cost of goods sold (Part III). Only sensible if you buy print, mark it up, carry the risk, and run it as a product line. Part III flows to Line 4 and implies inventory accounting most freelancers do not keep. For a one-off pass-through, it is more paperwork than it earns.

- Net it out. Exclude the $5,400 from income and skip the deduction, reporting only the $600. Defensible only if it was a genuine client-arranged reimbursement you fronted, not money you invoiced as your own.

The five-minute version: did you mark it up and eat the risk if the client canceled? If yes, COGS is arguable. If you passed it through on your own invoice as a convenience, gross up and deduct. If the client basically reimbursed you, net it out. Unless print is a real product line for you, skip Part III.

Every designer expense and the exact line it belongs on

Here is the part the writer walkthrough does not cover. These are the expenses a working designer actually has, mapped to the line the IRS expects them on. Print this once and you will stop guessing.

| Designer expense | Schedule C line | Designer note |

|---|---|---|

| Adobe Creative Cloud Pro, Figma, software subscriptions | Line 27a (Part V, “software subscriptions”) | Line 18 also accepted. Pick one and stay consistent. |

| Wacom Cintiq, Mac, iPad Pro, monitors | Line 13 (via Form 4562) | Equipment lasting over a year. 100% write-off in 2025 under bonus depreciation. |

| Font and typeface licenses | Line 27a (Part V, “font licensing”) | Desktop, web, and foundry licenses all count. The line designers throw away most often. |

| Adobe Stock, mockups, stock assets | Line 27a or Line 22 | Consumable creative assets used in client work. |

| Upwork, Fiverr, marketplace fees | Line 10 (commissions and fees) | The platform’s cut, now a variable 0-15% per contract on Upwork. |

| PayPal, Stripe processing fees | Line 10 or Line 27a | Comes out before payout, so it rarely feels like an expense. |

| Subcontracted illustrator or animator | Line 11 (contract labor) | Issue a 1099-NEC if you paid one person $600 or more in 2025. That threshold rises to $2,000 for 2026 payments. |

| Print run sent to a printer for a client | Line 22 (supplies), or Part III COGS | Depends on your markup model. See the section above. |

| Portfolio site, Behance Pro, domain | Line 8 (advertising) | It promotes your work, so it lives here. |

| Coworking desk rent | Line 20b (rent or lease, other) | Separate from the home office deduction. |

| Liability or errors-and-omissions insurance | Line 15 (insurance) | Health insurance does NOT go here. That is Schedule 1. |

| Design conference travel and meals | Line 24a (travel), Line 24b (meals at 50%) | Adobe MAX, regional conferences, client press checks. |

| Driving to clients and the print shop | Line 9 (car and truck) | 70 cents per mile for 2025, 72.5 cents for 2026. |

| Dedicated workspace at home | Line 30 | Simplified at $5 per square foot, or actual via Form 8829. |

Do I depreciate my Cintiq or write it off in one year?

Jordan bought a Wacom Cintiq Pro for $3,499 in March 2025. Equipment that lasts more than a year is a capital asset, so it goes on Line 13, not Line 22. The old worry was spreading the cost over five years. That worry is mostly gone for 2025.

The One Big Beautiful Bill Act, signed July 4, 2025, permanently restored 100 percent bonus depreciation for qualifying equipment acquired and placed in service after January 19, 2025. Before the bill, the 2025 rate was scheduled to fall to 40 percent. Jordan writes off the full $3,499 in 2025 on Line 13, filed through Form 4562. A new Mac or iPad Pro used for work follows the same path.

One shortcut sits below all of this. The de minimis safe harbor lets you expense any item costing $2,500 or less outright, with no depreciation, if you make the election on your return. A $1,200 monitor qualifies and can go straight to expenses. The $3,499 Cintiq is over the limit, so it takes the Line 13 route. Watch the purchase date too: gear bought on or before January 19, 2025 falls under the old 40 percent rule for that year. Section 179 is the alternative election, capped at $2.5 million for 2025, but it cannot create a loss, so for a single tablet bonus depreciation handles it automatically.

Where does the Adobe subscription and font licensing go?

Adobe replaced the All Apps plan with Creative Cloud Pro in 2025. It now runs $69.99 a month, around $780 a year on the annual plan, up from the old $60-a-month All Apps price. It is a recurring software cost, so it belongs on Line 27a in Part V, labeled “software subscriptions,” alongside Figma and anything else you pay for monthly. Line 18, office expense, is also accepted. The IRS cares that you are consistent, not which of the two you pick.

Font licensing is the deduction designers throw away most often. A $200 desktop license from a foundry for a logo project, a webfont license bought for a client site, a Monotype subscription: all deductible, all Line 27a. If you bought the type to do paid work, it is a business expense. Track it the year you buy it, because nobody remembers a font invoice in April.

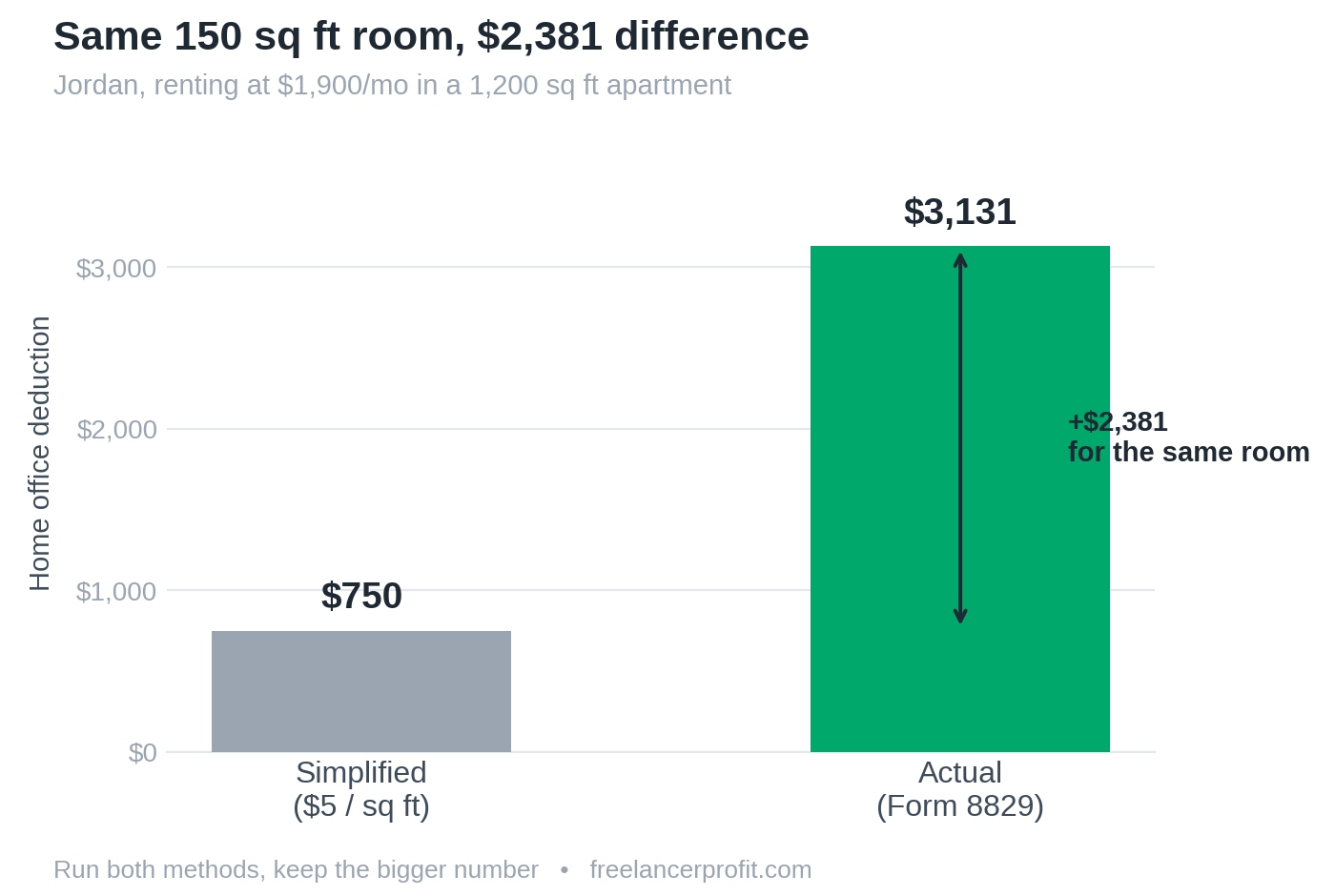

Simplified or actual home office method for designers?

Jordan works from a 150 square foot room used only for design. The simplified method pays $5 per square foot up to 300 square feet, so Jordan’s simplified deduction is $750. Quick, no forms, fine if your rent is low.

The actual method is worth far more for renters in expensive cities. Jordan pays $1,900 a month in a 1,200 square foot apartment, so the office is 12.5 percent of the home. Apply that to rent ($22,800), plus utilities and renter’s insurance (about $2,250), and the deduction works out near $3,131 through Form 8829. That is roughly $2,380 more than the simplified number for the same room. Designers renting in California, New York, or Illinois almost always win with the actual method. Run both and keep the bigger one. The full math sits in the home office deduction guide.

The mistake designers make every April

The pattern shows up constantly in r/tax and r/freelance threads: a designer writes off a $3,500 tablet as “supplies” on Line 22 instead of putting it on Line 13. The total deduction often lands close either way, so the return passes. The problem is the audit trail. Equipment on a supplies line is a flag, and you lose the clean depreciation record that protects you. We trace every number we publish back to primary sources, which you can read about on our methodology page.

Two more cost real money. Defaulting to the simplified home office method because it is easier, when the actual method would pay $2,000 more. And putting health insurance premiums on Line 15. Health insurance for the self-employed is an above-the-line deduction on Schedule 1, not a Schedule C expense, and it is capped at your net business income. Get that one wrong and you either lose the deduction or claim it twice.

Jordan’s bottom line

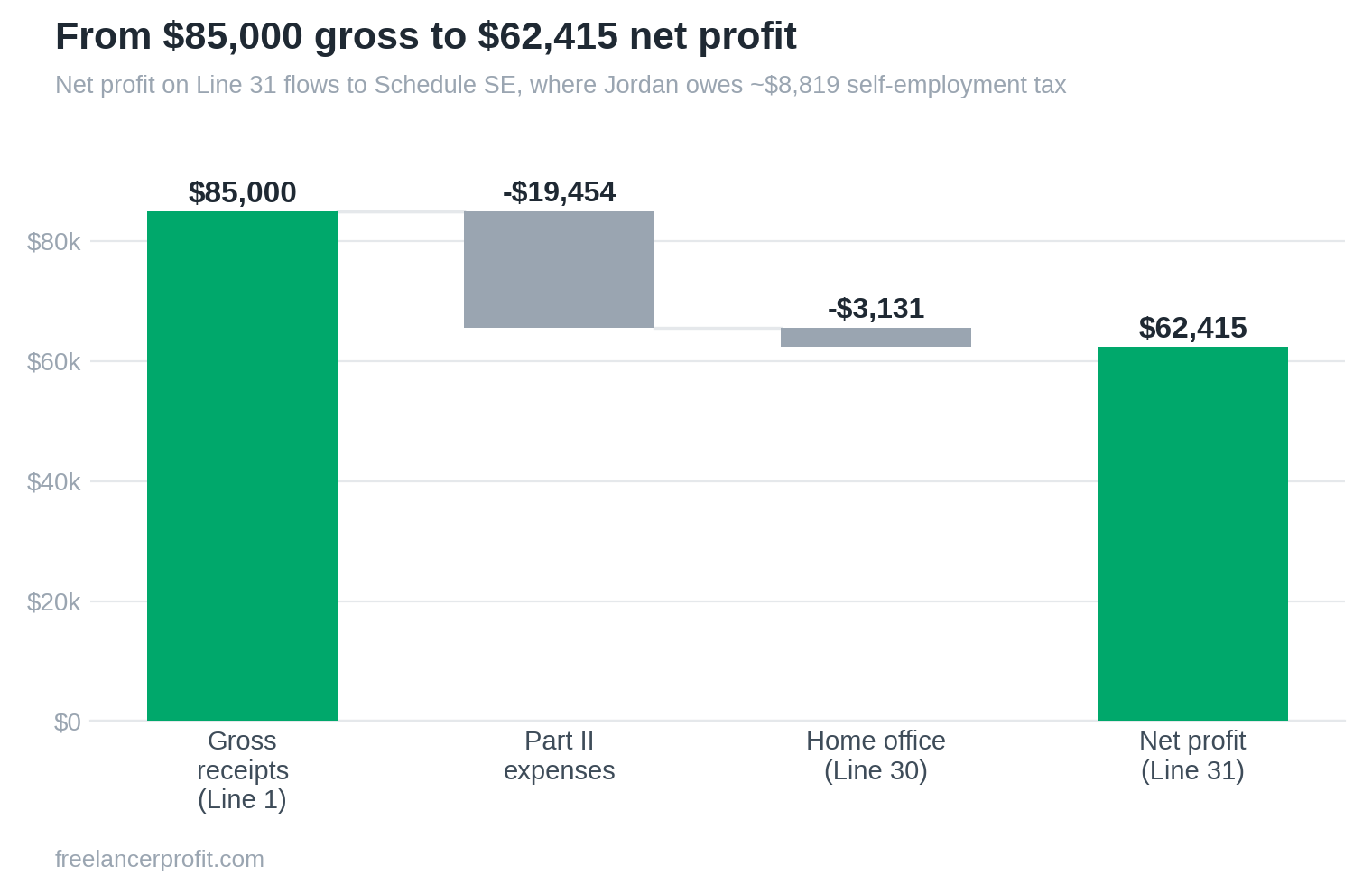

Add up Jordan’s expenses across Part II and the total comes to $19,454, including the $5,400 print cost, the $3,499 Cintiq, the Upwork fees, software, fonts, travel, and mileage. That leaves $65,546 on Line 29. Subtract the $3,131 home office on Line 30 and Jordan’s net profit is $62,415 on Line 31. That number flows to Schedule SE.

Self-employment tax runs 15.3 percent on 92.35 percent of net profit, so Jordan owes about $8,819, and half of that comes back as a deduction on Schedule 1. The qualified business income deduction reduces the taxable amount further, 20 percent for 2025 and 23 percent starting 2026 after the One Big Beautiful Bill Act made it permanent. Graphic design is not a specified service business, and at $62,415 Jordan is well under the income threshold anyway, so the full QBI deduction applies. For the set-aside math behind all of this, see how much to set aside and the quarterly estimated taxes guide.

One thing to do this week: pull last year’s Schedule C, find every expense you dumped into a single box, and re-sort it against the table above. If your $3,000-plus equipment is sitting on Line 22, that is the first thing to move. Tracking it cleanly from day one is the whole point of a real expense system, and the right accounting software for designers tags most of these to the correct line automatically.

The designer’s Schedule C line map

The table above, on one page you can stick next to your monitor. Every designer expense, the exact Schedule C line, and the catch to watch for, including the print-versus-COGS decision and the bonus depreciation date trap. Pull it out once a month when you categorize and April takes minutes instead of an afternoon.

Frequently Asked Questions

What NAICS code do graphic designers use on Schedule C?

Graphic designers use NAICS code 541430, Graphic Design Services, in box B (your principal business code) at the top of Schedule C. Web and UX designers sometimes fit 541511, Custom Computer Programming Services, depending on whether the work is visual design or build. The code does not change your tax. It just classifies your business, so pick the one that best describes what you actually do for clients.

Can I deduct my Adobe Creative Cloud subscription?

Yes. Adobe Creative Cloud is fully deductible if you use it for paid work. Put it on Line 27a in Part V, labeled “software subscriptions,” next to Figma, Sketch, or any other monthly tool. Line 18, office expense, also works. Adobe replaced All Apps with Creative Cloud Pro in 2025 at $69.99 a month, around $780 a year, so it is one of your larger recurring deductions. Do not let it disappear into a vague catch-all.

Do I have to depreciate my Cintiq or can I write it off in one year?

For 2025 you can write the whole thing off in one year. The One Big Beautiful Bill Act restored 100 percent bonus depreciation for equipment acquired and placed in service after January 19, 2025. A $3,499 Cintiq goes on Line 13 and you claim the full amount through Form 4562. Smaller gear costing $2,500 or less per item can be expensed outright under the de minimis safe harbor, so a budget monitor may skip Line 13 entirely.

Where does Upwork’s fee go on Schedule C?

Upwork’s freelancer service fee goes on Line 10, commissions and fees. Report your gross Upwork earnings on Line 1, then deduct the fee on Line 10. Upwork moved from a flat 10 percent to a variable 0 to 15 percent rate in May 2025, though most designers still pay close to 10 percent, so on $13,000 expect roughly $1,300. PayPal and Stripe processing fees go on the same line.

Is graphic design a specified service business for QBI?

Graphic design is generally not treated as a specified service trade or business, so the qualified business income deduction is not restricted the way it is for consulting, law, or accounting. Even if it were, the limits only bite above the income threshold ($197,300 single for 2025). A designer netting in the $60,000 to $90,000 range sits well below that and claims the full deduction, 20 percent for 2025 and 23 percent from 2026.

Do I report the full amount a client pays for print, or just my markup?

If you invoiced the client for the full print cost, report the full amount on Line 1 and deduct what you paid the printer on Line 22, supplies. Your markup shows through as profit on its own. Cost of goods sold in Part III is only worth it if you run print as a marked-up product line with inventory. If the client simply reimbursed money you fronted, you can leave it off income entirely and skip the deduction.

Tax laws change every year and the figures here reflect the 2025 and 2026 rules as of the review date above. This is informational only, not tax or legal advice. Verify current numbers at IRS.gov and check anything that affects your return with a qualified CPA.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.