Updated May 17, 2026: Strengthened the verdict, removed in-article affiliate CTAs, and added a “skip all four” branch for freelancers earning under $25k. Pricing remains verified as of May 4, 2026.

This guide covers the best bank accounts for freelancers in 2026. Four banking apps want your freelance business. One of them won’t even let a sole proprietor open an account. Here’s the honest comparison nobody else writes.

You opened a free business checking account three years ago because Reddit told you to. It worked fine. Then last month a $4,800 client payment hit, the app froze your account for “review,” and support replied four days later asking for documents you’d already uploaded twice.

That story shows up in every fintech complaint thread on Reddit and Trustpilot. It’s the single biggest reason freelancers switch banks, and it’s the reason this comparison exists.

Found, Relay, Novo, and Mercury are the four names that come up most when freelancers ask where to put their business money in 2026. They look similar from the outside. They’re all fintechs, none are actual banks, and they all promise no monthly fees on the entry plan. The differences only show up when you read the fee schedules, the FDIC structure, the sole-prop eligibility rules, and the customer-support gaps.

This guide walks through what each one actually charges in 2026, what protection your money has if something goes wrong, who can and cannot open an account, and which one fits which freelance situation. By the end you’ll have a defensible answer for your specific setup, not a generic top-pick badge.

Why a separate business account matters (and what the IRS actually requires)

The IRS does not require a sole proprietor to have a separate business bank account. You can run your freelance business out of your personal checking and file Schedule C without ever opening a second account. That’s the legal answer.

The practical answer is different. Mixing personal and business spending in one account is the single biggest reason freelancers underclaim deductions and overpay tax at year-end. When January arrives and you’re trying to reconstruct what was business and what was personal across 1,400 transactions, you cut corners. You skip the legitimate $42 charge because you can’t remember if it was the client lunch or the date night. Multiply that across a year and you’ve handed the IRS several thousand dollars you didn’t owe.

A separate account also matters if you ever form an LLC. The legal protection of an LLC depends on keeping business and personal funds separate. Lenders, courts, and the IRS all treat commingled funds as evidence the entity is a sham. If you’re already running clean books in a separate account, the LLC step is easier to take when you’re ready.

For more on when to make that move, our guide to sole proprietorship vs LLC vs S-Corp for freelancers walks through the income thresholds where each structure starts to make sense.

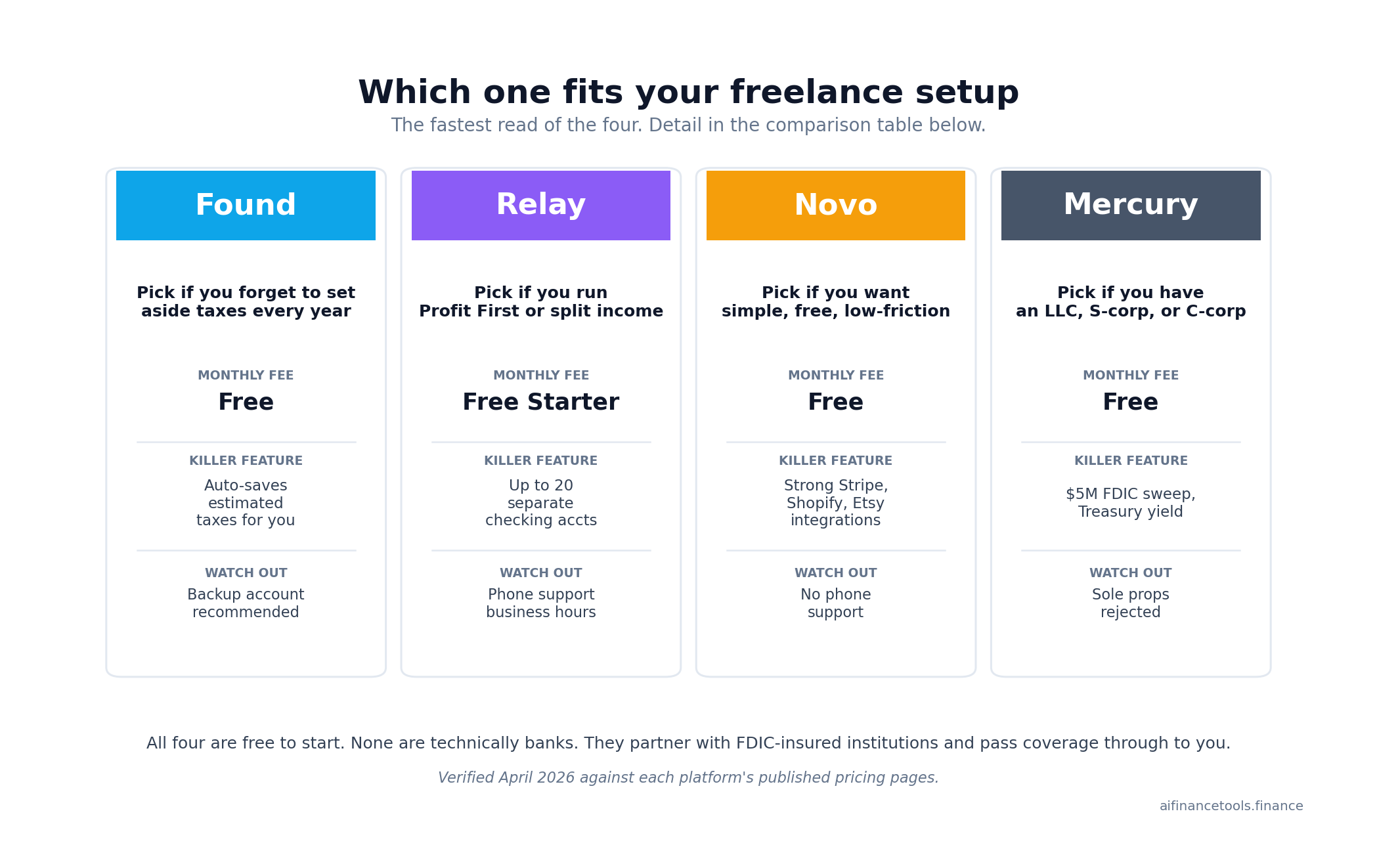

Found: built for solo freelancers who hate bookkeeping

Found is the most freelancer-specific of the four. The platform combines a business checking account with built-in invoicing, automatic expense categorization, contractor payments with 1099-NEC generation, and a tax-savings tool that holds back a percentage of every deposit toward your estimated taxes. Lead Bank provides the FDIC backing.

Found pricing in 2026

- Found Free — $0/month, no minimum balance, no monthly maintenance fee. Includes invoicing, expense categorization, tax estimation, and 1 custom rule plus 1 custom tag plus 1 custom category.

- Found Plus — $35/month or $315/year. Adds 1.50% APY on balances up to $20,000, unlimited custom rules and categories, scheduled tax payments to the IRS, and detailed financial reports.

- Found Pro — $80/month or $720/year. Adds 2.50% APY on all balances with no cap, 1% cashback on qualifying card spend, dedicated account manager, and lower wire fees.

The transactional fees on the free plan add up if you’re not paying attention. Instant transfers cost 1.75% (with a $0.50 minimum). Domestic outgoing wires are $15 ($10 on Pro). Cash deposits at retail locations cost $1.75. Card payments accepted from clients via the built-in Stripe integration run 2.9%. There’s a $10 dormancy fee if your account sits unused for 12 consecutive months.

What real Found users report in 2026

Found’s Trustpilot rating sits at 4.5 stars across more than 1,283 reviews as of early 2026. The positive reviews focus on the tax-savings feature and the quality of the mobile invoicing. Reviewers like Courtney N. praise that money feels safe and transfers run on time. The recurring praise across reviews: bookkeeping and banking in one place, automatic tax savings, and clean Stripe integration.

The Better Business Bureau tells a different story. Found has an F rating from the BBB based on 146 complaints, with the dominant theme being sudden account closures and frozen funds. Reddit threads in r/freelance and r/smallbusiness echo the same pattern: accounts frozen with no warning, support reachable only by email, funds tied up for weeks while documents get re-uploaded. NerdWallet has confirmed that frozen-account holders only have access to email support, not phone.

Who Found fits among the best bank accounts for freelancers

Found works for sole proprietors making $30,000 to $90,000 a year who want banking, invoicing, and basic tax-set-aside in one app, but with a caveat. Found currently holds an F rating with the BBB based on 146 complaints, with the dominant theme being sudden account closures and frozen funds. If you go with Found, do not use it as your only business account, and do not park more than 30 days of operating cash here. Use a second bank for reserves. The invoicing, tax estimation, and 1099-NEC issuance are genuinely useful features, but the support model and freeze risk make Found a better second account than a primary one.

Found does not fit you if you ever park more than $250,000 in the account (the FDIC ceiling), if you take cash regularly (each retail deposit costs $1.75 plus the trip), or if you need same-day support for an account problem. Keep a backup account at a second institution if Found is your primary.

Relay: built for the Profit First crowd and growing freelance businesses

Relay is the bank Mike Michalowicz fans gravitate toward. Its core feature is the ability to open up to 20 individual checking accounts (each with its own routing and account number) under a single business profile. That structure lets you run a Profit First system without spreadsheets: one account for taxes, one for owner pay, one for operating expenses, one for profit, all linked to a single dashboard. Thread Bank provides the FDIC backing through a sweep network. If you’re deciding between the two for a solo setup, see our head-to-head on Relay vs Mercury for sole proprietors.

Relay pricing in 2026

- Relay Starter — $0/month. Up to 20 checking accounts (10 for sole proprietors), 2 savings accounts, 50 debit cards. Free incoming and outgoing ACH. Savings APY 0.91%.

- Relay Grow — $30/month. Adds same-day ACH, automated bill pay, advanced accounting integrations. Savings APY 1.55%.

- Relay Scale — $90/month (promotional, regular $120/month). Higher account limits, lower transaction fees, AI-powered cash flow tools. Savings APY 2.68%.

The standout feature is the FDIC coverage. Relay routes deposits through Thread Bank’s insured cash sweep program, providing FDIC coverage up to $3 million per account. That’s 12 times the standard $250,000 limit. For a freelancer parking a tax-savings reserve plus operating cash, that buffer matters.

The Thread Bank issue (and why it’s mostly resolved)

The FDIC issued an enforcement action against Thread Bank in 2024, citing concerns about its banking-as-a-service program (which Relay is part of) and asking for stronger suspicious-activity monitoring. The order was terminated in December 2025 after Thread Bank addressed the issues. No customer funds were ever at risk during the action, and the FDIC’s termination of the order is a positive signal. Federal enforcement actions against partner banks are uncommon but not unheard of in the fintech space, and the resolution suggests the underlying issues have been corrected.

That said, Trustpilot reviews and Reddit threads from late 2025 and early 2026 still describe occasional account freezes when Thread Bank’s fraud detection flags activity. Relay launched a dedicated Account Protection Team in early 2026 to speed up resolution. The pattern is real but less severe than Found’s.

Who Relay fits

Relay fits freelancers running a Profit First system, anyone who wants separate accounts for taxes and operating expenses without juggling logins, and any freelancer with more than $250,000 sitting in business reserves at any point in the year. It also fits well if you work with a bookkeeper, since the QuickBooks Online and Xero integrations are clean on every plan including the free tier. For more on cash flow management with multiple buckets, see our guide to managing freelance cash flow.

Relay does not fit you if you take cash deposits regularly (it accepts cash via Allpoint+ ATMs and Green Dot Network retailers, but the latter charges up to $4.95 per deposit). It also doesn’t have built-in invoicing, so you’ll pair it with a tool like FreshBooks or Wave. For invoicing options, our best invoicing software guide covers the leading picks.

Novo: the lightweight option for solo freelancers who hate fees

Novo is the simplest of the four. One checking account, no monthly fee, no minimum balance, no APY, and a clean interface designed for solo entrepreneurs. Middlesex Federal Savings provides the FDIC backing at the standard $250,000 limit. The platform serves more than 200,000 customers and holds a 4.5-star rating on Trustpilot.

Novo pricing in 2026

Novo is genuinely free. There’s no monthly maintenance fee, no minimum balance, no transaction limits, no fees for incoming wires, no fees for ACH transfers in or out, and no fees for sending mailed paper checks. The only listed fees are a $27 insufficient-funds charge and a $27 uncollected-funds return fee. Novo also refunds up to $7/month in third-party ATM fees automatically.

What Novo gives up to be free

The trade-offs are real. Novo pays 0% APY on checking balances, so any tax reserves you park there earn nothing. The platform doesn’t accept cash deposits at all (you’d need to buy a money order and deposit that via mobile check). Domestic wire transfers are in beta and not available to all users. Customer support is email-only and operates Monday to Friday during US business hours, with no phone support except for fraud reports.

The strong points are the integrations. Novo connects directly to Stripe, Shopify, Etsy, eBay, and Wise, and through those connections to QuickBooks, Xero, and PayPal. Novo Boost speeds up Stripe payouts by as much as 95%, which matters if your clients pay through Stripe and you’re tired of three-day waits. The built-in invoicing tool lets you create unlimited custom invoices and accept payment via ACH, Venmo, PayPal, Stripe, or Square.

Who Novo fits

Novo fits solo freelancers earning $20,000 to $80,000 a year who want a simple business checking account with zero fees and don’t need APY on idle cash because they sweep tax reserves into a separate high-yield savings elsewhere. It’s particularly good for freelancers who get paid through Stripe (Novo Boost speeds payouts) or who run a side e-commerce business through Shopify, Etsy, or Amazon.

Novo doesn’t fit you if you regularly handle cash, if you need same-day phone support, or if you keep more than $250,000 in business reserves. It also doesn’t fit if earning interest on idle cash matters to you, since the 0% checking APY means inflation eats real money on larger balances. For comparison, Bluevine pays 1.30% APY on balances up to $250,000 with $3 million in FDIC sweep coverage.

Mercury: the option most freelancers can’t actually use

Mercury is the most polished and best-funded of the four, and it doesn’t accept sole proprietorships. That single rule disqualifies most US freelancers. Mercury requires a registered business entity (LLC, S-Corp, C-Corp, or partnership) with an EIN. If you file Schedule C as a sole prop using your Social Security Number, you can’t open an account with Mercury, full stop.

For freelancers who have formed an LLC or made the S-Corp election, Mercury is genuinely excellent. Choice Financial Group and Column N.A. provide the FDIC backing through sweep networks, with coverage up to $5 million. There’s no monthly fee, no minimum balance, no overdraft fees, and free domestic and international USD wires (a 1% conversion fee applies to non-USD wires).

Mercury pricing in 2026

- Mercury checking — $0/month, $0 minimum balance, free USD wires (domestic and international), free ACH, no overdraft fees. FDIC up to $5 million via sweep network.

- Mercury Treasury — for balances over $500,000. Yields up to ~3.65% via SEC-registered investment products. Not FDIC-insured but SIPC-covered up to $500,000.

- Mercury IO credit card — 1.5% cashback on all spend. Available to qualifying account holders.

Mercury applied for its own national bank charter and FDIC insurance in December 2025, which would eliminate the partner-bank dependency that’s caused issues for other fintechs. As of mid-2026 the application is still pending, and Mercury continues to operate through Choice Financial Group and Column N.A.

The partner-bank history matters

Choice Financial Group received an FDIC enforcement action in 2023 related to its banking-as-a-service program. Evolve Bank & Trust (a former Mercury partner) received a Federal Reserve enforcement action in 2024 and was implicated in the Synapse collapse the same year, which left more than 100,000 fintech customers locked out of approximately $265 million in deposits for months. Mercury moved its banking partnerships during this period and now uses Choice Financial Group and Column N.A. exclusively. The Synapse situation underscored why FDIC insurance only protects against bank failure, not the failure of the fintech middle layer.

Who Mercury fits

Mercury fits freelancers who have formed an LLC or S-Corp, have larger cash balances ($50,000 or more), and frequently send wires (international clients, vendor payments overseas). It also fits anyone planning to raise capital or scale into a small agency, since Mercury’s investor introductions and treasury products are designed for that path.

Mercury does not fit sole proprietors. It also doesn’t fit anyone who handles cash, since cash deposits are not supported. And the support model (email and chat, with phone support limited and weekday-only) means urgent issues get answered slower than at a traditional bank.

Side-by-side: Found vs Relay vs Novo vs Mercury in 2026

| Feature | Found | Relay | Novo | Mercury |

|---|---|---|---|---|

| Free plan monthly fee | $0 | $0 | $0 | $0 |

| Top paid tier | $80/mo (Pro) | $90/mo promo (Scale) | No paid tiers | No paid tiers |

| FDIC coverage | $250K (Lead Bank) | $3M sweep (Thread Bank) | $250K (Middlesex Federal) | $5M sweep (Choice + Column) |

| Sole prop allowed? | Yes (SSN) | Yes (SSN, 10-account limit) | Yes (SSN) | No (EIN required) |

| APY on free plan | 0% | 0.91% (savings) | 0% | 0% checking; up to 3.65% Treasury |

| Sub-accounts | No | Up to 20 checking | Reserves (virtual buckets) | Yes |

| Built-in invoicing | Yes | No | Yes | Yes |

| Tax savings tool | Yes (auto) | Manual via sub-account | No | No |

| Cash deposits | Yes ($1.75 fee) | Yes (Allpoint+ free, retail up to $4.95) | No | No |

| Domestic wire fee | $15 ($10 on Pro) | $5 incoming via Payment Request; outgoing varies by plan | Beta, limited | Free (USD) |

| Phone support | Weekdays | Yes (chat + email + phone) | Email only (fraud 24/7) | Limited, weekdays |

| Best for | Solo freelancers wanting tax automation | Profit First users, larger reserves | Stripe-paid or e-commerce solos | LLC/S-Corp with $50K+ balance |

Pricing and APYs verified May 4, 2026 from each vendor’s official pricing page. Subject to change.

The decision: a five-minute framework

You don’t need to read 5,000 words to pick. Here’s the framework I’d run if I were doing this in five minutes:

Three of these four banks are workable. Mercury locks out sole proprietors entirely (most readers of this guide). Of the remaining three, Relay is the only one I’d recommend as a primary business account: it has the strongest FDIC sweep coverage ($3M), Profit First-style sub-accounts, and the least concerning support and freeze pattern. Found and Novo work as backup accounts or secondary accounts. Use one as your primary only if you’re a sub-$60k freelancer with no cash reserves and accept the operational risk of fintech-style support.

- Do you currently earn under $25,000 a year in freelance income with fewer than 50 business transactions? If yes, skip all four. Open a second personal checking account at your existing bank, call it your “business” account in your head, and route all client payments there. A spreadsheet handles your bookkeeping at this volume. Come back to this guide when you cross $25k and 100 transactions.

- Are you a sole proprietor? If yes, Mercury is out. Move on.

- Do you ever hold more than $250,000 in business reserves? If yes, Relay (up to $3M sweep) or Mercury (up to $5M sweep) are your only safe choices. Found and Novo cap at $250K.

- Do you want automated tax savings built into your bank? If yes, Found is the only one with this feature out of the box.

- Do you run a Profit First system or want separate accounts for taxes, owner pay, and operating expenses? If yes, Relay’s 20 sub-accounts are the only true match.

- Do you get paid through Stripe and want fast payouts? Novo Boost is the differentiator here.

- Are you an LLC or S-Corp moving meaningful money via wires? Mercury’s free domestic and international USD wires save real money compared to the others.

If two options match, the tiebreaker is your support tolerance. Found and Novo are weakest on this dimension. Relay and Mercury have more responsive support but still aren’t a traditional bank. None of them have branches.

The fintech risk nobody talks about (but you need to)

None of these four are banks. They’re fintech companies that partner with FDIC-insured banks. That distinction usually doesn’t matter. Until it does.

In April 2024, a fintech middleware company called Synapse filed for Chapter 11 bankruptcy. Synapse sat between fintech apps (like Yotta, Juno, and others) and the underlying FDIC-insured banks (most notably Evolve Bank & Trust). When Synapse collapsed, more than 100,000 customers were locked out of approximately $265 million in deposits for months. The CFPB, multiple federal agencies, and a Yale Journal investigation all documented the same lesson: FDIC insurance protects you against the failure of the bank, not against the failure of the fintech middle layer.

Two practical takeaways for your business:

- Always keep a backup checking account at a different institution. Even $500 at a credit union or a basic Chase Business Complete account is enough to keep paying rent and utilities if your fintech account goes dark for two weeks.

- Don’t keep more than 30 days of operating expenses in any single fintech account. Sweep larger reserves into Relay (which has the highest sweep coverage among the freelancer-friendly options at $3M) or split across two providers.

This is the freelancer version of risk management. You don’t need a treasurer, but you need to understand that the FDIC sticker on a fintech app means something different from the FDIC sticker on a Wells Fargo branch.

What about the other names? Bluevine, Lili, Chase Business

Three other accounts come up often enough to mention.

Bluevine business checking earns 1.30% APY on balances up to $250,000 with $3 million in FDIC sweep coverage through Coastal Community Bank. It’s a strong fifth option if you want a fintech alternative with real interest on checking. The catch is that the high APY requires either $5,000 in monthly debit card spend, $2,500 in monthly customer payments, or $1,000 in monthly direct deposits. Most freelancers will hit one of these.

Lili sits in the same category as Found, with built-in tax tools and invoicing. It’s been through several pricing changes over the past two years, which makes it harder to recommend with confidence. Verify current pricing on lili.co before committing.

Chase Business Complete Banking is the right choice if you take cash regularly and need physical branches. It carries a $15 monthly fee with several waiver paths (the most common being a $2,000 minimum daily balance, though Chase has multiple other waiver options that can apply). The trade-off is a real-bank backstop in exchange for a less freelancer-tailored interface.

Get the freelance bank picker checklist

I built a one-page checklist that walks through the seven questions you need to answer before opening any business account: sole prop or entity, monthly cash flow, peak balance, cash deposit needs, wire frequency, support tolerance, and tax-savings preferences. Match your answers to the table and you’ll know which of the four (or which of the alternatives) actually fits.

Drop your email below and I’ll send it.

One thing to do this week

If you’re still using a personal account for business income, open a Found Free or Novo account this week. Both take under 10 minutes to set up, neither requires an EIN, and both are genuinely free at the entry tier. Move your next client invoice through the new account and start the year-end cleanup with one clean line of transactions instead of 1,400 mixed ones.

For deeper guidance on what comes next (estimated taxes, bookkeeping, and the deductions you’ll be able to claim once you have clean records), see our guides on filing quarterly estimated taxes, how much to set aside for taxes, and Schedule C line by line.

How to actually open one of these accounts

If you want to move forward, here’s the order I’d take: open a Relay account first if you want sub-accounts or have over $250k in reserves at any point in the year. Open a Novo account if you just want a clean, free, simple checking and you get paid via Stripe. Open a Found account as a secondary account if you want the tax-savings automation, but keep your reserves elsewhere. Mercury is only relevant once you’ve formed an LLC or S-Corp. Take the direct path: search the bank’s name in your browser, open the account directly from their site, and avoid affiliate redirect chains for accounts you’ll trust with business income.

What I haven’t done

Full disclosure: I have not opened accounts with all four banks myself. The analysis above synthesizes BBB complaint patterns, Trustpilot reviews, Reddit threads on r/freelance and r/smallbusiness, the FDIC enforcement records on Thread Bank and Choice Financial Group, and each bank’s published pricing pages verified May 4, 2026. If you’ve opened one of these accounts and your experience differs from what’s described above, leave a comment. I update these guides when freelancers correct them.

Frequently Asked Questions

Do I really need a separate business bank account if I’m a sole proprietor?

Legally no. The IRS doesn’t require a sole proprietor to have a separate business account. Practically yes. Mixing personal and business spending in one account is the single biggest reason freelancers underclaim deductions and overpay tax. A separate account also protects you if you convert to an LLC later, because lenders and the IRS treat commingled funds as evidence of a non-business operation.

Can I open Found, Relay, or Novo without an EIN?

Yes. All three accept sole proprietors using a Social Security Number instead of an EIN. Mercury is the exception and requires an EIN tied to a registered business entity. If you form an LLC later, you can apply for an EIN free at IRS.gov in about 10 minutes.

What if my Found or Relay account gets frozen?

Keep a backup checking account at a different institution and don’t let a single fintech account hold more than 30 days of operating expenses. If a freeze happens, contact support immediately, document every interaction in writing, and ask for a written explanation. Most freezes resolve within 7 to 21 days. The FDIC and CFPB have escalation paths if a freeze drags on longer.

Is the FDIC coverage on these accounts as safe as a regular bank?

FDIC insurance protects you against the failure of an insured bank up to coverage limits ($250,000 standard, higher with sweep programs). It does not protect you against the failure or fraud of the fintech middle layer. The Synapse collapse in 2024 left more than 100,000 customers locked out of approximately $265 million for months even though the underlying banks were FDIC-insured. Keep balances reasonable and a backup account active.

Which account is best for accepting client payments via Stripe or PayPal?

Novo and Found both have first-class Stripe integration. Novo Boost speeds Stripe payouts by up to 95% in many cases. Found’s invoice product uses Stripe under the hood and lets you accept card payments at 2.9% per transaction. Relay and Mercury support Stripe and PayPal as payment processors but don’t have built-in invoicing as polished as Novo or Found.

Can I switch banks mid-year without messing up my taxes?

Yes. Download a CSV export of every transaction from your old account before you close it. When you file, combine both accounts’ transactions in your bookkeeping software or a spreadsheet. The IRS doesn’t care how many accounts you used during the year, only that you accurately report income and expenses on your Schedule C.

What about Bluevine, Lili, or Chase Business?

Bluevine is a strong fifth option with 1.30% APY on checking balances up to $250,000 (subject to monthly activity requirements) and FDIC coverage up to $3 million through Coastal Community Bank. Lili is closer to Found in design but has had more pricing changes recently. Chase Business is the right answer if you take cash regularly and need branches, though Chase Business Complete carries a $15 monthly fee with several waiver paths.

Does Mercury really not allow sole proprietors?

Correct. Mercury’s eligibility rules require a registered US business entity with an EIN. That excludes sole proprietors operating under a DBA with just an SSN, which is the default structure for most freelancers in their first year. If you form an LLC and obtain an EIN, you become eligible. Mercury applied for its own national bank charter in December 2025, but the eligibility rules have not changed as of mid-2026.

Pricing and APYs in this article were verified on May 4, 2026 from each vendor’s official pricing page and may change. This is informational content, not tax, legal, or financial advice. Verify current rules at IRS.gov and on each vendor’s site before opening an account. For your specific situation, consult a qualified CPA or financial advisor.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.