If you freelance as a sole proprietor, one of these banks will reject your application before you finish filling it out. The other opens with your SSN in about ten minutes. Here’s which one fits your setup, and where each quietly costs more than it advertises.

Most Relay vs Mercury comparisons are written for small businesses that already have an LLC and an EIN in hand. You might not have either. File a Schedule C under your own name with just your Social Security number, and the biggest difference between these two banks has nothing to do with features. It’s whether they’ll let you open an account at all.

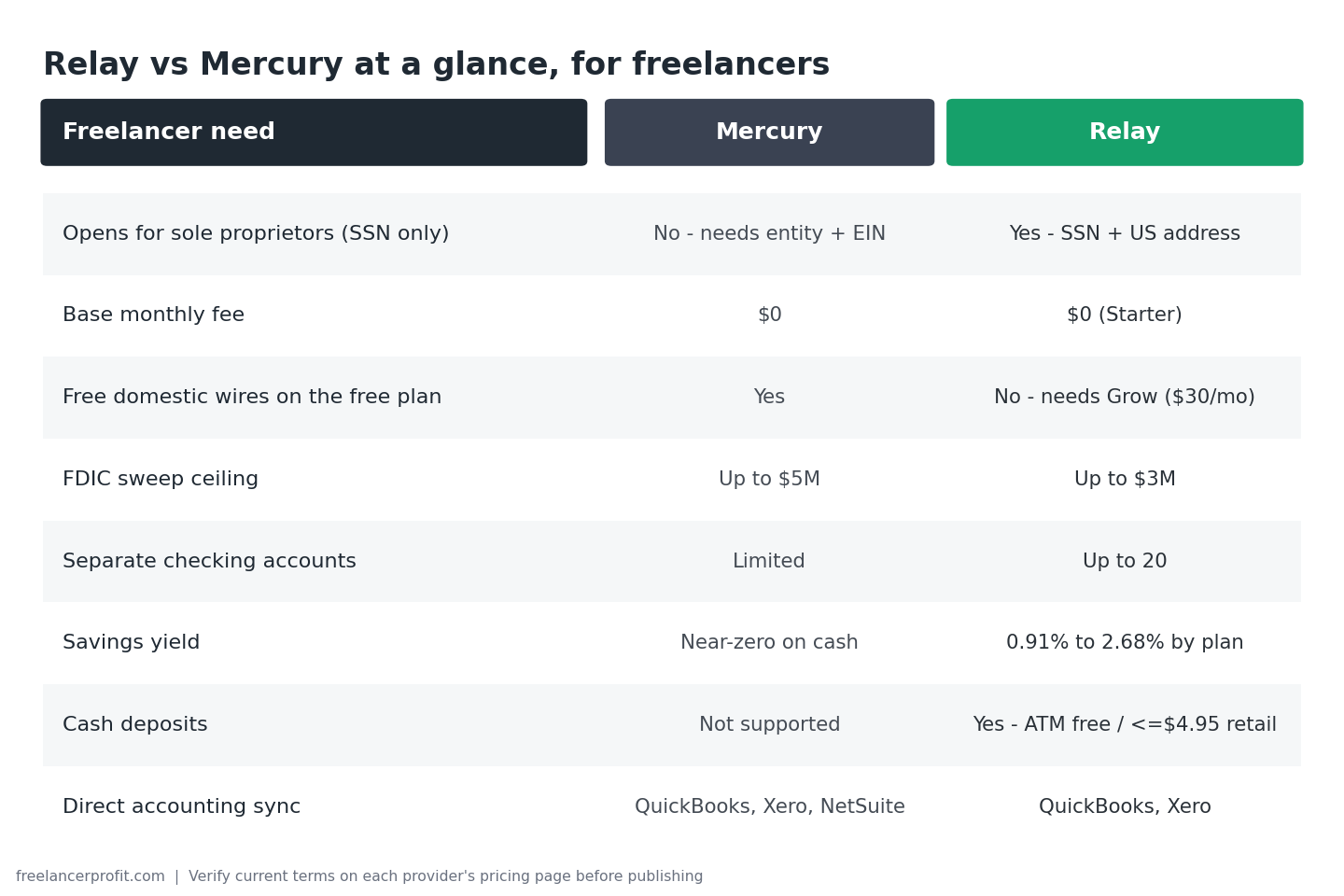

Mercury doesn’t open business accounts for sole proprietorships. Relay does. That one fact settles the question for a huge share of freelancers before any feature comparison even starts. Read that line twice. It catches people off guard.

If Mercury looks like your best fit, our full Mercury Bank review for freelancers breaks down exactly who it works for and who should skip it.

Neither one is a chartered bank. Both are fintech platforms. Mercury holds your deposits at Choice Financial Group and Column N.A. Relay holds yours at Thread Bank. There are no branches. Both are built for people who get paid by ACH, wire, and card, not cash. Past that, they make very different bets, and they suit very different freelancers.

Can you even open each one as a freelancer?

Start here. It filters out half the decision. Mercury requires a registered US business entity: an LLC, an S-corp, a C-corp, or a partnership, plus an EIN and your formation documents. Operate as a sole proprietor or a DBA with no EIN, and Mercury’s application won’t approve you. That’s been Mercury’s policy for years, and it still holds in 2026.

Relay supports sole proprietors. Its own help docs say it opens accounts for sole proprietors with a valid SSN and a physical US address. No EIN. No LLC. You apply with your name, your SSN, and proof of where you operate. P.O. boxes and virtual mailbox addresses get rejected, so use a real one.

Take a freelance copywriter making $58,000 a year, working under her own name, no LLC. Mercury is closed to her unless she forms an entity first. Relay opens with her SSN. If she wants to weigh whether forming an LLC is worth it for other reasons, that’s a separate decision, covered in our guide on sole proprietorship vs LLC vs S-corp for freelancers, and the LLC formation services we rate if she decides to.

Already run an LLC or an S-corp? This filter doesn’t apply, and both banks are on the table. Read on. If you’re a sole proprietor and you don’t want to form an entity, you can skip the Mercury sections. Relay is your option of the two.

What each bank actually costs (without the marketing spin)

Both market themselves as free. At the base tier, both are: no monthly fee, no minimum balance. The costs hide in the things you do most. Wires. Savings yield. The upgrade someone talks you into.

Mercury’s pricing

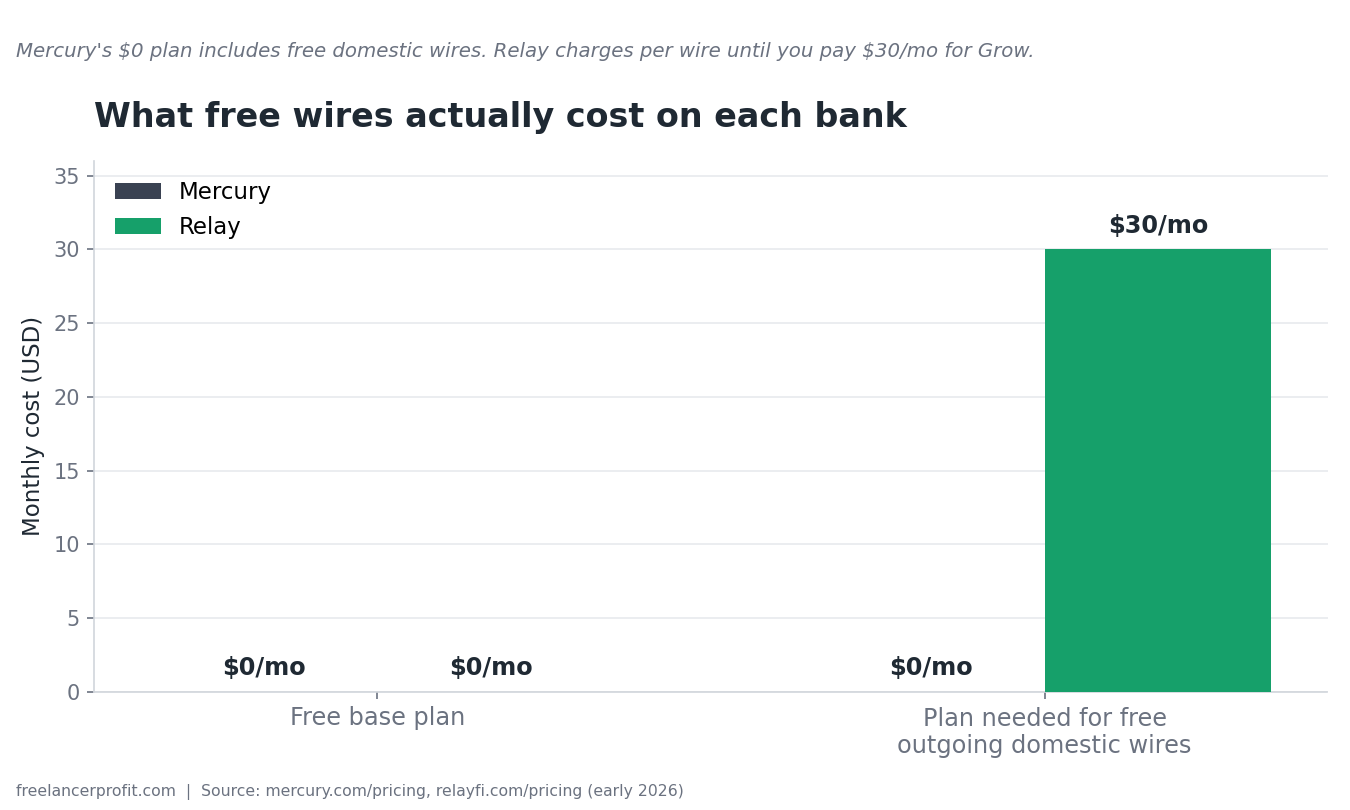

Mercury’s base plan is $0 a month. It covers free domestic wires, free outgoing USD international wires, free ACH, free checks, virtual and physical debit cards, and the IO credit card with 1.5% cash back. Non-USD international wires carry about a 1% currency conversion fee, and card purchases in foreign currencies add up to 3%. Mercury Plus is $35 a month and adds recurring and branded invoicing. Mercury Pro is $350 a month and adds a dedicated relationship manager plus richer NetSuite automation, which almost no solo freelancer needs.

Relay’s pricing

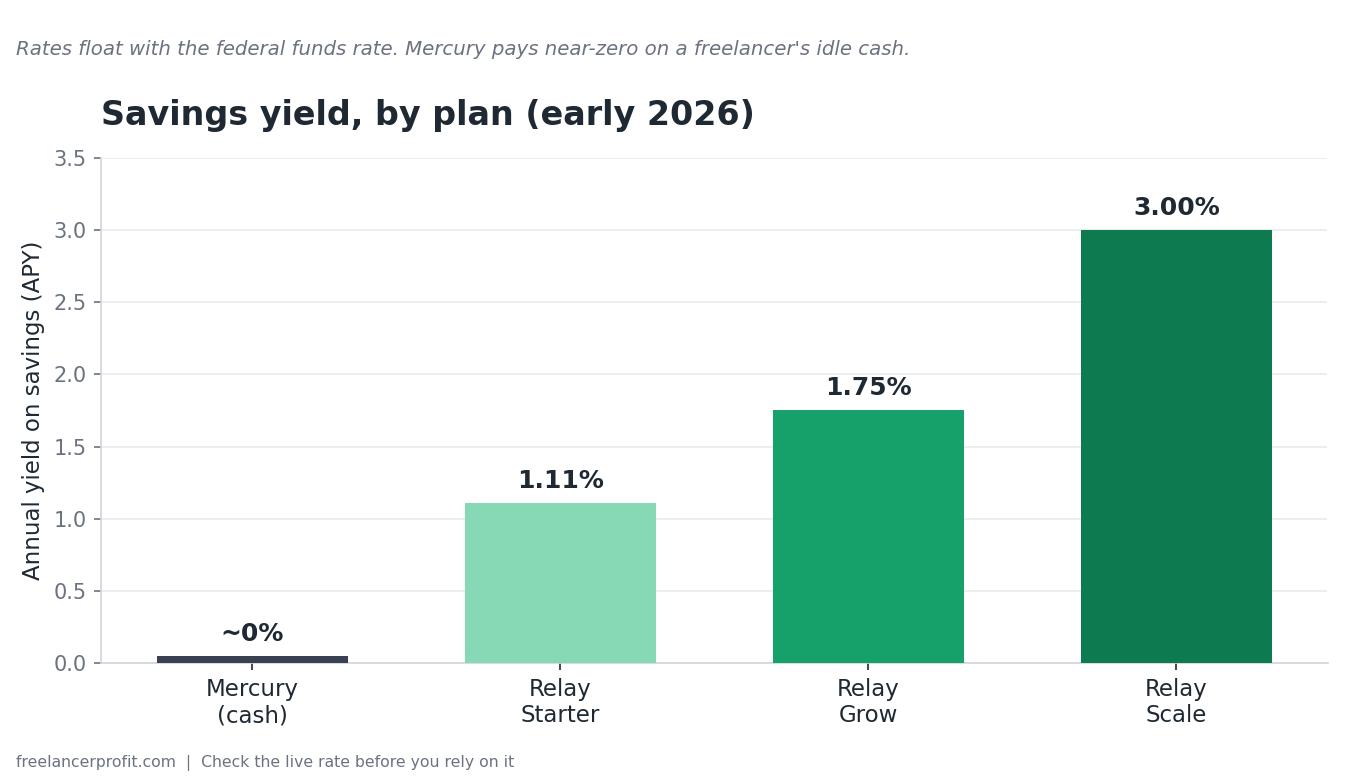

Relay Starter is $0 a month, with up to 20 checking accounts and 2 savings accounts. Here’s the catch most reviews skip: on the free Starter plan, outgoing domestic wires aren’t free. You need the Grow plan at $30 a month for free outgoing domestic wires, same-day ACH, and automated bill pay. Scale runs $90 a month for larger teams. Savings yield tracks your plan: roughly 1.11% on Starter, 1.75% on Grow, and 3.00% on Scale as of early 2026. Rates float with the federal funds rate, so check the live number before you bank on it.

This flips the usual story. People assume Relay is the free one and Mercury is the one that costs money. For a freelancer who sends wires, Mercury’s free plan can be the cheaper of the two, because Mercury gives you free wires at $0 while Relay charges for outgoing wires until you’re paying $30 a month. Never send wires? The point is moot. Pay an overseas contractor by wire every month? It matters.

| Freelancer need | Mercury | Relay |

|---|---|---|

| Opens for sole proprietors (SSN only) | No. Requires registered entity + EIN | Yes. SSN + physical US address |

| Monthly fee (base plan) | $0 | $0 (Starter) |

| Free outgoing domestic wires on the free plan | Yes | No. Needs Grow ($30/mo) |

| Free outgoing USD international wires | Yes | Limited, plan-dependent |

| FDIC coverage (pass-through sweep) | Up to $5M | Up to $3M |

| Separate checking accounts for budgeting | Limited | Up to 20 |

| Savings yield | Near-zero on cash; Treasury ~4% APY ($250k min) | 1.11% to 3.00% by plan |

| Cash deposits | Not supported | Allpoint+ ATM free; Green Dot up to $4.95 |

| Direct accounting sync | QuickBooks Online, Xero, NetSuite | QuickBooks Online, Xero |

| FreshBooks / Wave | Bank feed or CSV only | Via Yodlee feed only |

| Partner bank | Choice Financial Group, Column N.A. | Thread Bank |

If you want this account compared against the wider field, our roundup of the best business bank accounts for freelancers puts both alongside Novo, Found, Bluevine, and Lili. We score every entry against the same checklist, explained on our methodology page and applied across all our freelance finance tool reviews.

FDIC coverage: which one protects more of your money?

Standard FDIC insurance covers $250,000 per depositor, per bank. Both Mercury and Relay stretch that with a sweep network that spreads your deposit across multiple partner banks, so more of it stays insured. Mercury’s sweep covers up to $5 million through Choice Financial Group, Column N.A., and their network banks. Relay’s covers up to $3 million through Thread Bank and the IntraFi network.

For most freelancers earning $45,000 to $110,000, neither ceiling is the thing that decides it. You’re not likely to park $3 million in a checking account. The number starts to matter if you keep a big tax reserve, a buffer for a slow stretch, and an emergency fund all in one place, or if a large project payment lands and sits for a quarter. In that case, Mercury’s higher ceiling is a real edge, even if you rarely trigger it.

One more thing worth knowing. Mercury filed for its own national bank charter with the OCC in December 2025. Until that goes through, the partner-bank structure above is what applies. Relay’s partner, Thread Bank, received an FDIC enforcement action in 2024, worth knowing even though your deposits stay FDIC-insured through the sweep. Pass-through insurance also depends on conditions being met, so treat the headline number as a ceiling, not a promise on every dollar.

Account organization and the Profit First method

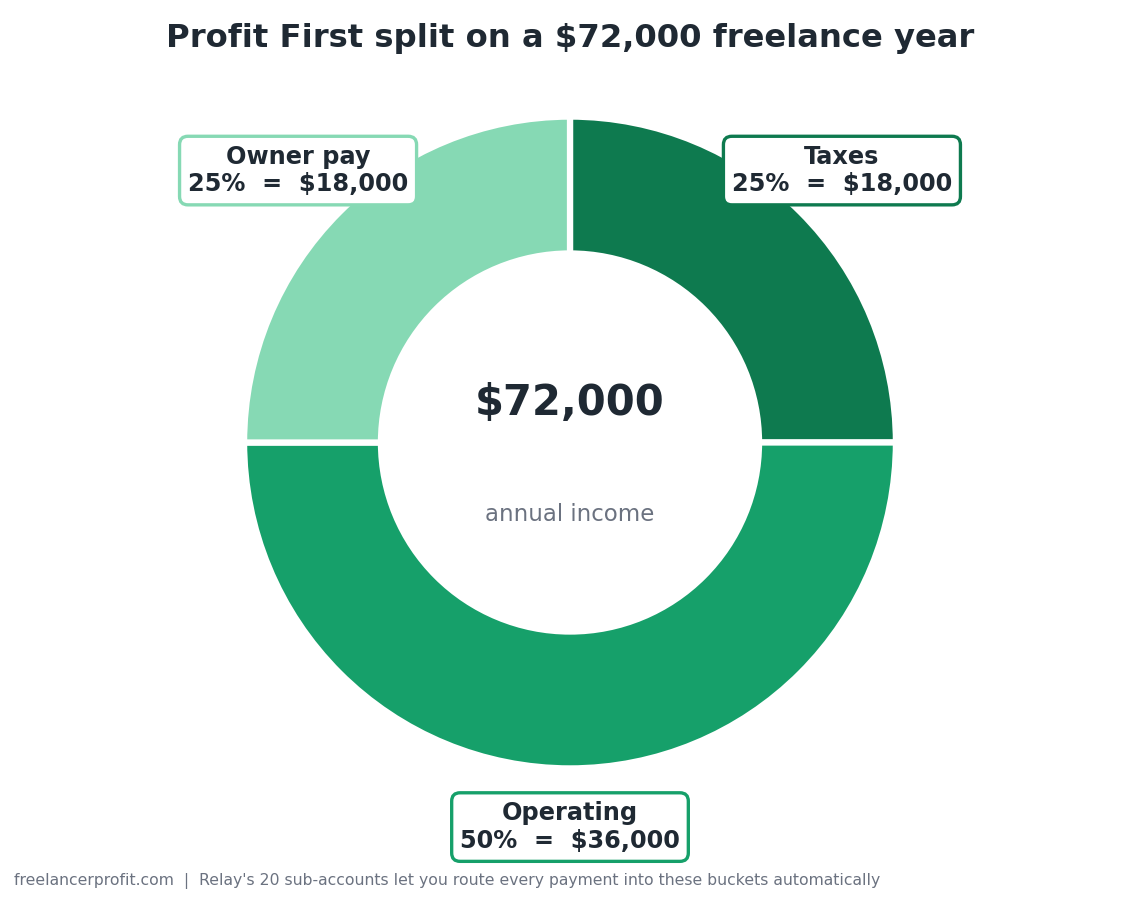

This is where Relay pulls ahead. You can open up to 20 separate checking accounts under one login, each with its own account and routing number. Freelancers use this to run envelope budgeting without a single spreadsheet. One account for taxes, one for operating expenses, one for owner pay, one for profit. Money lands where it belongs instead of in one undifferentiated pile.

A freelance designer making $72,000 can route every client payment so 25% drops into a tax account, 50% into operating, and the rest into owner pay, then leave the tax bucket untouched until quarterly time. That does more to prevent a year-end cash shock than any app reminder ever will. It pairs directly with the math in our guide on how much to set aside for taxes and the schedule in filing quarterly estimated taxes.

Mercury runs the opposite way: fewer accounts, more automation. You get a checking and savings setup, automated transfer rules, and approval workflows built for teams and startups. You can build some structure, but you won’t get Relay’s 20-account layout. If labelled buckets are the reason you’re switching banks, Relay wins this section outright. If you’d rather set a percentage rule and forget it, Mercury suits you fine. Either way, keeping those buckets clean is what makes tracking business expenses bearable come tax time.

How do they connect to QuickBooks, FreshBooks, and Wave?

Both banks favour the same two tools for direct syncing. Mercury has native integrations with QuickBooks Online, Xero, and NetSuite, with a bank feed that syncs several times a day. Relay syncs natively with QuickBooks Online and Xero. Keep your books in either of those and both banks reconcile cleanly. The difference here is small.

The gap shows up with FreshBooks or Wave, which plenty of freelancers run. Neither bank has a true native sync for those. Relay connects to FreshBooks through Yodlee, an aggregated read-only feed rather than a deep integration, and to other money apps through Plaid. Mercury connects FreshBooks through standard bank feeds or CSV export. Wave gets no direct link from either bank, so you’re pulling transactions through aggregation or importing a CSV.

Be honest about your stack before you choose. Committed to FreshBooks or Wave? Don’t expect the slick auto-categorisation QuickBooks users get with these banks. Our roundups of the best accounting software for freelancers and best invoicing software for freelancers walk through which tool pairs with which bank.

The complaints freelancers actually report

Both banks have a recurring complaint, and they’re not the same complaint. Knowing them up front is worth more than any feature list.

- Relay: account holds and verification friction. Trustpilot and Reddit threads describe accounts getting flagged by Thread Bank’s fraud detection and frozen for days while support sorts it out. Relay launched an Account Protection Team in 2026 to deal with this, and plenty of holds clear quickly, but the pattern still shows up in recent reviews.

- Mercury: account closures and offboarding. In 2024, TechCrunch reported Mercury closing or restricting accounts tied to founders in certain countries, including earlier rounds that hit Nigerian and other startups. Application rejections are common too, and Mercury rarely spells out the reason.

Neither pattern is a dealbreaker, and neither is unique to these two. Account freezes and surprise closures come with fintech banking, versus a traditional bank with a branch you can walk into. The defence is the same for both: don’t keep your only account here. Keep a backup elsewhere so a hold never leaves you unable to make rent. We cover that backup habit in the guide on managing cash flow as a freelancer.

The mistake most freelancers make choosing between them

The common mistake, repeated across forum threads, is treating “free” as identical between the two. It isn’t. Relay’s free Starter plan charges for outgoing domestic wires. Mercury’s free plan doesn’t. So a freelancer who pays a subcontractor by wire twice a month can spend more on Relay’s free tier than on Mercury’s, or end up paying $30 a month for Grow to make those wires free. Picture a freelance developer running an LLC, earning $95,000, who wires an overseas collaborator every month. On Mercury that costs nothing. On Relay Starter it costs per wire, which nudges them toward the $30 Grow plan.

The second mistake is choosing on FDIC numbers you’ll never reach while ignoring the eligibility rule that blocks you before you start. If you’re a sole proprietor, Mercury’s $5 million ceiling means nothing, because you can’t open the account. Sort eligibility and your real transaction habits first. The headline coverage figure comes last.

A five-minute decision framework

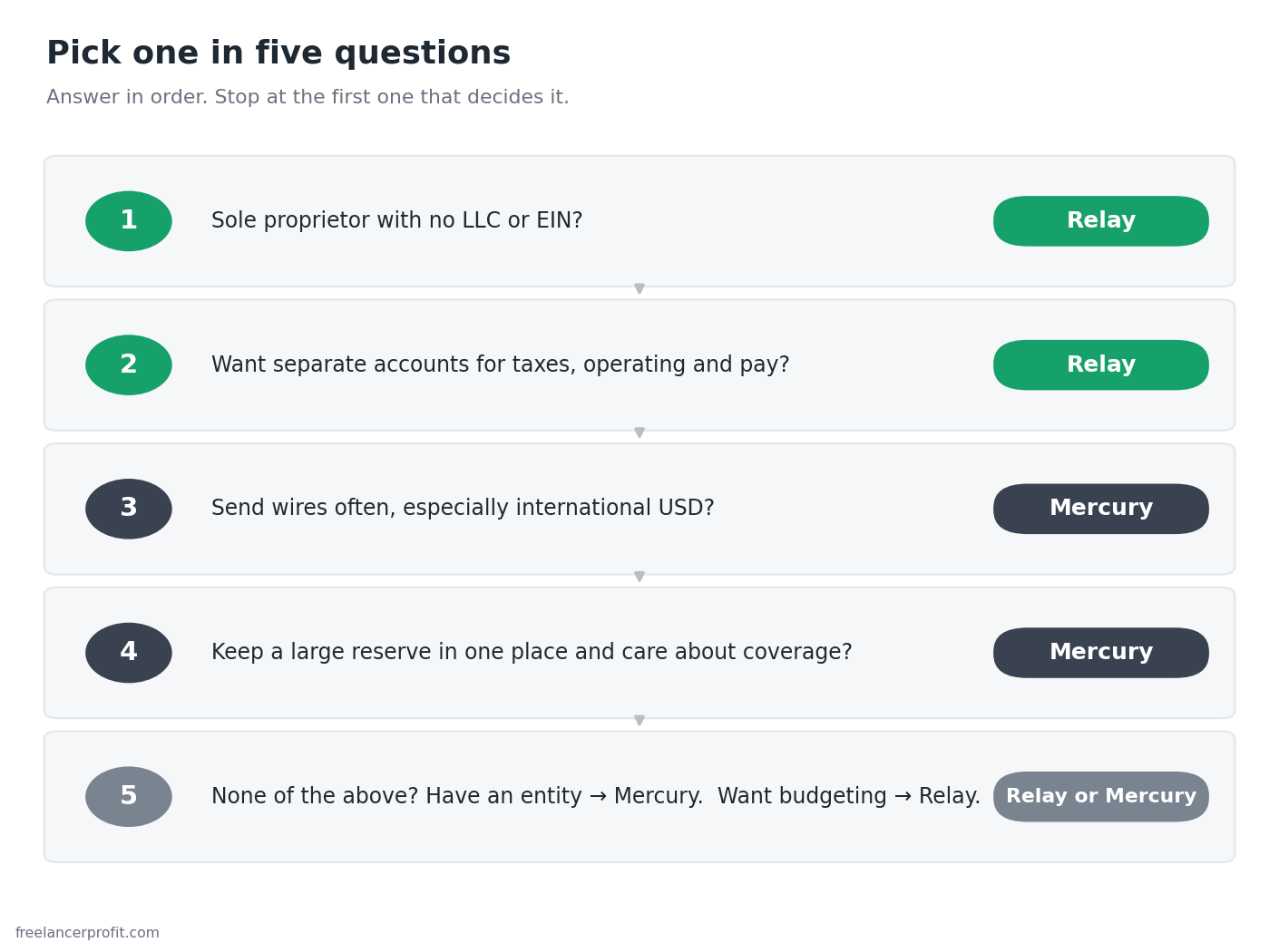

The Relay vs Mercury choice comes down to a handful of questions. Answer these in order. Stop at the first one that decides it for you.

- Are you a sole proprietor with no LLC or EIN? Pick Relay. Mercury will not open your account. Done.

- Do you want separate accounts for taxes, operating, and pay? Pick Relay. The 20-account structure is the whole point.

- Do you send wires often, especially international USD? Pick Mercury. Free wires on the $0 plan beat Relay’s wire fees.

- Do you keep a large reserve in one place and care about coverage? Lean Mercury for the $5M sweep ceiling.

- None of the above strongly applies? If you have an entity, default to Mercury for the cleaner free tier. If you want budgeting structure, default to Relay.

Relay vs Mercury: the verdict on who should pick which

Pick Relay if you’re a sole proprietor without an entity, or you want to run envelope budgeting with separate accounts for tax, operating, and owner pay, or you sometimes deposit cash. In the Relay vs Mercury matchup, it’s the better fit for the largest single group of freelancers: the ones filing a Schedule C under their own name.

Pick Mercury if you already run an LLC or S-corp, you send wires regularly and want them free without a monthly fee, you want the higher FDIC sweep ceiling, or you lean technical and value the API and automation. It rewards the freelancer who has already formalised the business.

One concrete step this week: open whichever one matches your answer in the framework, then open a second account at a different institution as your backup. A frozen account stings a lot less when it isn’t your only one. Not sure your books can keep up with a new account? Set the habit first with our guide to consistent accounting records.

Free: the freelancer bank-fit checklist

A one-page checklist that runs your situation through the same eligibility, fee, and FDIC questions in this guide, plus the documents you need to open either account on the first try. It also lists the four account buckets to set up if you go with Relay’s structure. Drop your email and it lands in your inbox.

Frequently Asked Questions

Can I open Mercury as a sole proprietor?

No. Mercury doesn’t open business accounts for sole proprietorships. You need a registered US entity, like an LLC, S-corp, C-corp, or partnership, along with an EIN and your formation documents. Operating under your own name with just an SSN means you’d have to form an entity first. Relay is the alternative of the two, since it opens accounts for sole proprietors with a valid SSN and a physical US address.

Is Relay or Mercury better for the Profit First method?

Relay. You can open up to 20 separate checking accounts under one login, each with its own account and routing number, which is exactly what Profit First and envelope budgeting need. Set up accounts for tax, operating expenses, owner pay, and profit, then split each client payment across them. Mercury is built around fewer accounts and automated transfer rules, so it can approximate the system without matching the labelled-bucket structure.

Which one has higher FDIC insurance?

Mercury. Its sweep network provides FDIC coverage up to $5 million through Choice Financial Group, Column N.A., and partner banks. Relay’s sweep, through Thread Bank and the IntraFi network, covers up to $3 million. Both run well past the standard $250,000 per-bank limit. For most freelancers, neither ceiling decides it, since you’re unlikely to hold balances near either figure. Pass-through coverage depends on conditions being met, so treat the number as a ceiling.

Are Relay and Mercury free?

Both have a $0 monthly base plan with no minimum balance. The difference is usage. Mercury’s free plan includes free domestic and USD international wires. Relay’s free Starter plan charges for outgoing domestic wires; free ones require the Grow plan at $30 a month. Send wires often and Mercury’s free tier can cost less than Relay’s. Rarely wire money and both are effectively free.

Do they sync with QuickBooks, FreshBooks, or Wave?

Both sync natively with QuickBooks Online and Xero, and Mercury also syncs with NetSuite. Neither has a deep native integration with FreshBooks or Wave. Relay connects FreshBooks through the Yodlee aggregation feed, and Mercury connects it through standard bank feeds or CSV export. Wave has no direct link from either bank, so you import transactions by aggregation or CSV. If clean accounting sync matters most, QuickBooks Online or Xero gives the smoothest result with either bank.

Can I deposit cash with Relay or Mercury?

Relay allows cash deposits. You can add cash free at Allpoint+ ATMs, or at Green Dot network retailers for a fee of up to $4.95. Mercury doesn’t support cash deposits at all. If any part of your freelance income shows up as physical cash, Relay handles it and Mercury doesn’t, which may push you toward Relay or toward keeping a traditional bank account on the side.

Are my deposits safe if Relay or Mercury fails?

Neither is a chartered bank. Your money sits at their FDIC-insured partner banks, so federal deposit insurance applies through those institutions, subject to the sweep program conditions. Mercury filed for its own national bank charter in December 2025, and that’s still in process. Relay’s partner, Thread Bank, received an FDIC enforcement action in 2024. The practical safeguard for either is the same: keep a backup account at a second institution so an account hold or closure never leaves you stuck.

Tax and banking rules change, and the eligibility, pricing, FDIC, and integration details above can shift without notice. Verify current terms on the providers’ own pages and confirm anything tax-related at IRS.gov. This article is informational only and is not tax, legal, or financial advice. For your specific situation, consult a CPA.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.