Sort your finances once. Stop scrambling every April.

It’s 2pm on April 12. Your accountant just emailed asking for last year’s mileage log, three Stripe receipts, and the square footage of your home office. You don’t know where any of it is.

Most freelancers solve their bookkeeping problem too late. Once a year, around April, after half the receipts have already gone missing. The mileage isn’t logged. The Adobe charges look like personal subscriptions. You’re sorting a year of mixed transactions trying to remember what you bought in July.

The fix is a system. It isn’t complicated or expensive. Fifteen minutes a week, with your accounting software doing most of the work in the background while you stay focused on client work. This guide shows you what to track, how to organise it, when to update it, what changed under the One Big Beautiful Bill Act for 2026, and which tools take most of the work off your plate.

What disorganised records actually cost you

The cost of bad records is invisible until tax season. Then it gets very specific.

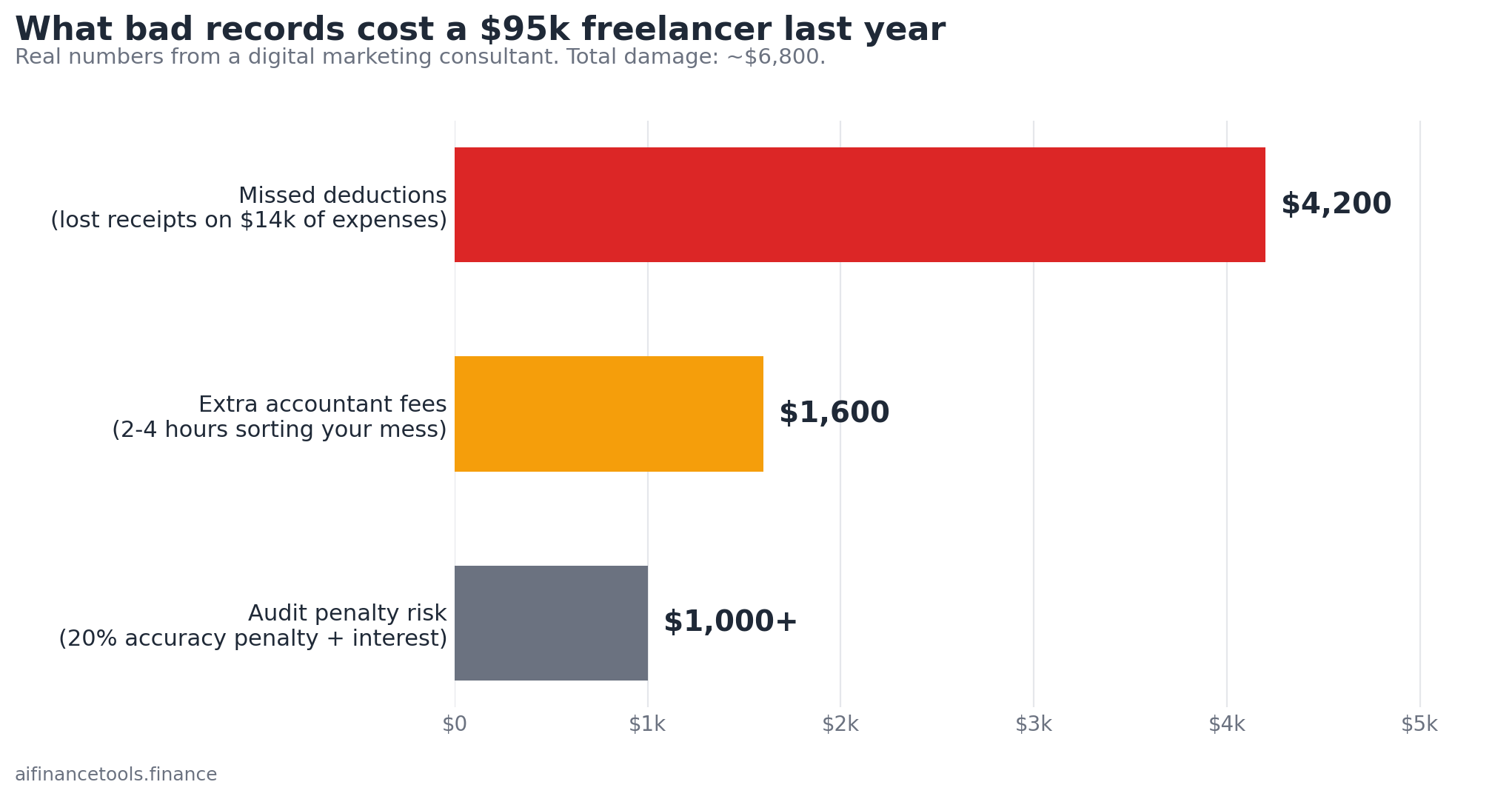

First cost: missed deductions. A freelance digital marketing consultant earning $95,000 paid an extra $4,200 in tax one year because she’d lost track of about $14,000 in legitimate business expenses. Software subscriptions. Contractor payments. A $1,400 conference she went to in February. Nothing dishonest, just nothing documented. Her marginal rate on that income was around 30% once you add federal income tax, self-employment tax, and state. Every dollar she couldn’t prove cost her about 30 cents.

Second cost: accountant fees. If you turn up in March with a folder of mixed receipts and 11 months of unreconciled transactions, your CPA will bill you to organise the mess before they file. CPA hourly rates for sole proprietor returns currently run $150 to $400. The difference between organised and disorganised records on a Schedule C return is usually two to four hours of billable time. That’s $300 to $1,600 a year, paid for nothing more than sorting work you could have done yourself in 10 minutes a week.

Third cost: audit exposure. Schedule C filers face higher audit rates than W-2 employees, particularly at higher income levels. Recent IRS Data Book figures show overall individual audit rates well below 1%, with Schedule C returns at the higher end of that range. The risk is not that an audit is likely. The risk is that if it happens, deductions you can’t document get disallowed. The burden of proof sits with you. You owe the additional tax, plus interest, plus potentially a 20% accuracy-related penalty under IRC Section 6662. Legitimate deductions become illegitimate the moment the paperwork isn’t there.

You can prevent all three with a system that takes less time than checking email.

Consistent Accounting Records: What You Actually Need to Keep

Before you build a system, you need to know what goes into it. Here’s every category of record a freelancer should hold.

Income records

Every dollar that comes into your business needs documentation. Copies of every invoice you sent, including the ones that went unpaid. Payment confirmations, whether they arrived by email, in your accounting software, or as a bank deposit. Any 1099-NEC forms you received. Bank statements showing direct deposits, ACH transfers, and check deposits.

Keep a copy of every invoice in your accounting software or a dedicated folder. If a client disputes a payment or the IRS questions your income, you need to show what you invoiced, when, and when it was paid.

Expense records

Every business expense needs a record showing the amount, date, vendor, and business purpose. Receipts for purchases. Business credit card and bank statements as backup for transactions where you’ve lost the original. A mileage log for business driving. Meal receipts with a note on the back showing who you met and what business you discussed.

You may have heard about a “$75 receipt rule.” Be careful with it. The $75 threshold in IRS Publication 463 applies specifically to travel, meals, gifts, and listed property under accountable plans for employees. For self-employed Schedule C filers, the IRS expects substantiation of every business expense regardless of amount. A bank or card statement showing the vendor, date, and amount can support smaller expenses. The safer rule is to keep a record for every expense you intend to deduct.

Tax records

Copies of every quarterly estimated tax payment, with date and amount. Your prior year tax returns, which you’ll use to calculate safe harbor payment amounts and prepare the current year’s return. Any correspondence from the IRS or your state tax agency. Documentation supporting major deductions: home office square footage and lease or mortgage statements, health insurance premium invoices, retirement account contribution confirmations, and SEP IRA or Solo 401(k) plan documents.

Business and contract records

Your contracts with clients, both for the business relationship and to document scope and payment terms. Business insurance policy documents. LLC formation documents and EIN paperwork if you’ve registered an entity. Loan agreements related to your business. W-9 forms from any subcontractors you’ve paid.

The records you need by deduction type

Each major Schedule C deduction has specific documentation the IRS expects. Generic advice to “keep your receipts” isn’t enough. Here’s what each deduction actually needs:

| Deduction | Records you need | Keep for |

|---|---|---|

| Home office | Square footage calculation showing the dedicated business area, mortgage or rent statements, utility bills, photos of the office space, Form 8829 calculation if using actual expense method | 7 years |

| Vehicle (mileage) | Contemporaneous mileage log with date, starting and ending odometer or trip miles, business purpose, and client or destination. The IRS standard mileage rate is 70 cents per mile for 2025 and 72.5 cents per mile for 2026 | 7 years |

| Business meals | Receipt plus names of attendees, business relationship, and what business was discussed. Meals are 50% deductible | 7 years |

| SEP IRA or Solo 401(k) | Contribution confirmations from your custodian, plan adoption documents, Form 5500-EZ if Solo 401(k) balance exceeds $250,000 | 7 years |

| Health insurance | Premium statements showing what you paid, Form 1095-A if you bought through the Marketplace, proof you had no access to a spouse’s employer plan | 7 years |

| Equipment over $2,500 | Receipt or invoice, depreciation schedule if you elect to depreciate, Section 179 election documentation if you expense it | Depreciation period plus 7 years |

| Subcontractors paid $2,000+ | W-9 collected before payment, copy of the 1099-NEC you sent them, payment records (the threshold rises to $2,000 for 2026 payments under OBBBA) | 7 years |

How long to keep everything

The IRS general rule is three years from the date you filed the return. Six years if you under-reported income by 25% or more. Seven years for losses related to worthless securities or bad debt. No limit if you filed a fraudulent return or didn’t file at all.

In practice, keeping everything for seven years is simpler than tracking which document falls into which category. State requirements can run longer. California’s Franchise Tax Board has up to four years to audit state returns, so California freelancers should plan for that minimum. Some states with multi-year statutes may push the practical retention period to eight years on certain documents.

What changed for 2025 and 2026 records under OBBBA

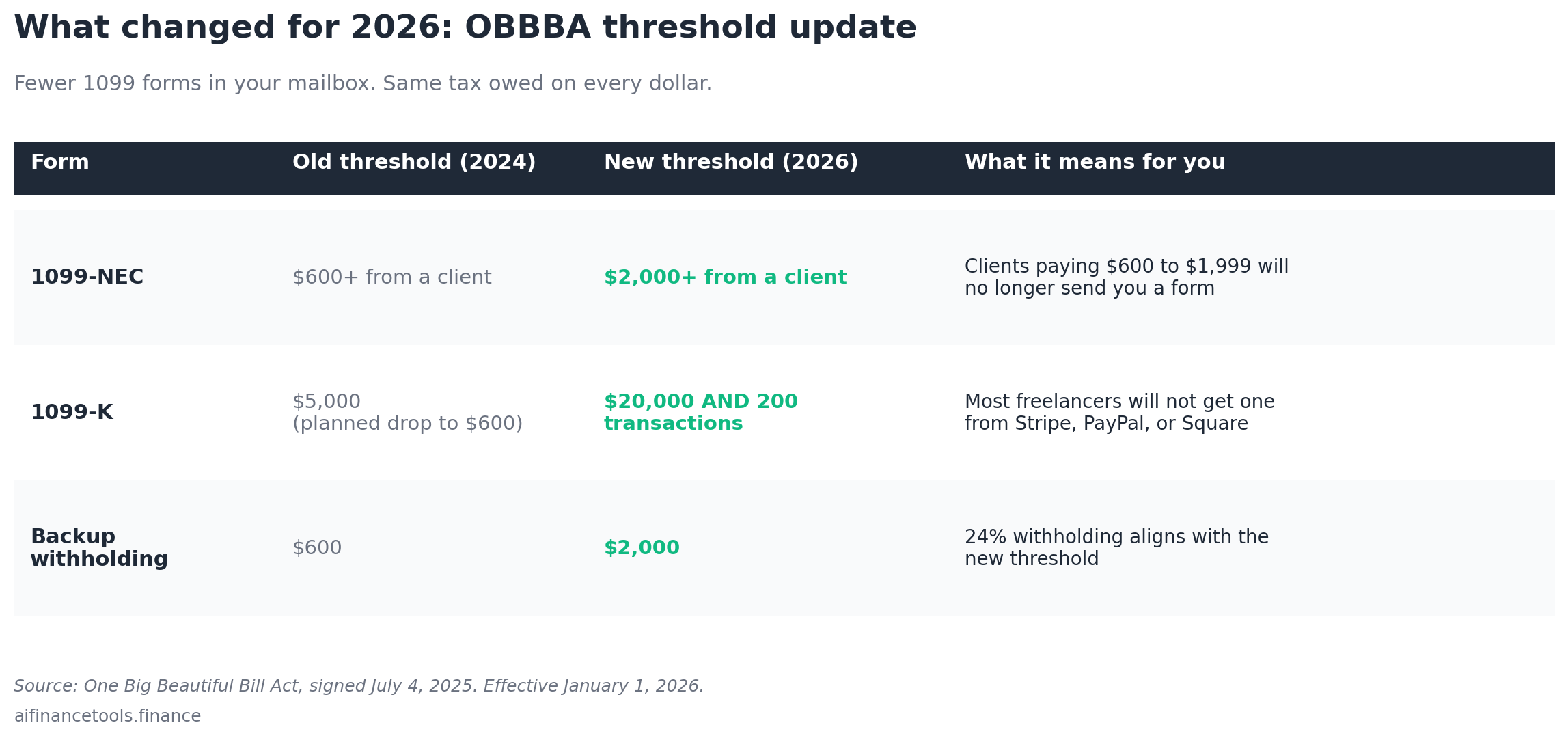

The One Big Beautiful Bill Act, signed July 4, 2025, changed three things that affect what records you need to keep yourself.

The 1099-NEC threshold rises from $600 to $2,000 starting January 1, 2026. Clients who paid you between $600 and $1,999 in 2026 will not be required to send you a 1099-NEC. You still owe tax on every dollar of that income. The IRS still expects you to report it. The change just means fewer paper trails arrive in your mailbox in January, and more responsibility falls on you to track payments yourself.

The 1099-K threshold reverted to $20,000 and 200 transactions. Under OBBBA, third-party payment platforms (Stripe, PayPal, Venmo for Business, Square, Etsy, Upwork) only issue a 1099-K if you exceed both $20,000 in payments and 200 transactions in the year. Both conditions must be met. The previously planned drops to $2,500 for 2025 and $600 for 2026 were eliminated. Most freelancers will not get a 1099-K under this rule.

Backup withholding aligns with the new $2,000 level. Clients only need to withhold 24% if a contractor fails to provide a valid W-9 and the payment exceeds the new threshold.

The practical takeaway: with fewer 1099s arriving, your bank deposits and your own invoicing records become the primary evidence of your income. If you weren’t tracking every payment yourself before, 2026 is the year to start. Our guide on avoiding tax liability shock walks through the income reconciliation process in more detail.

How to build your filing system

You have three options. The right one depends on how you work and what you’ll actually maintain.

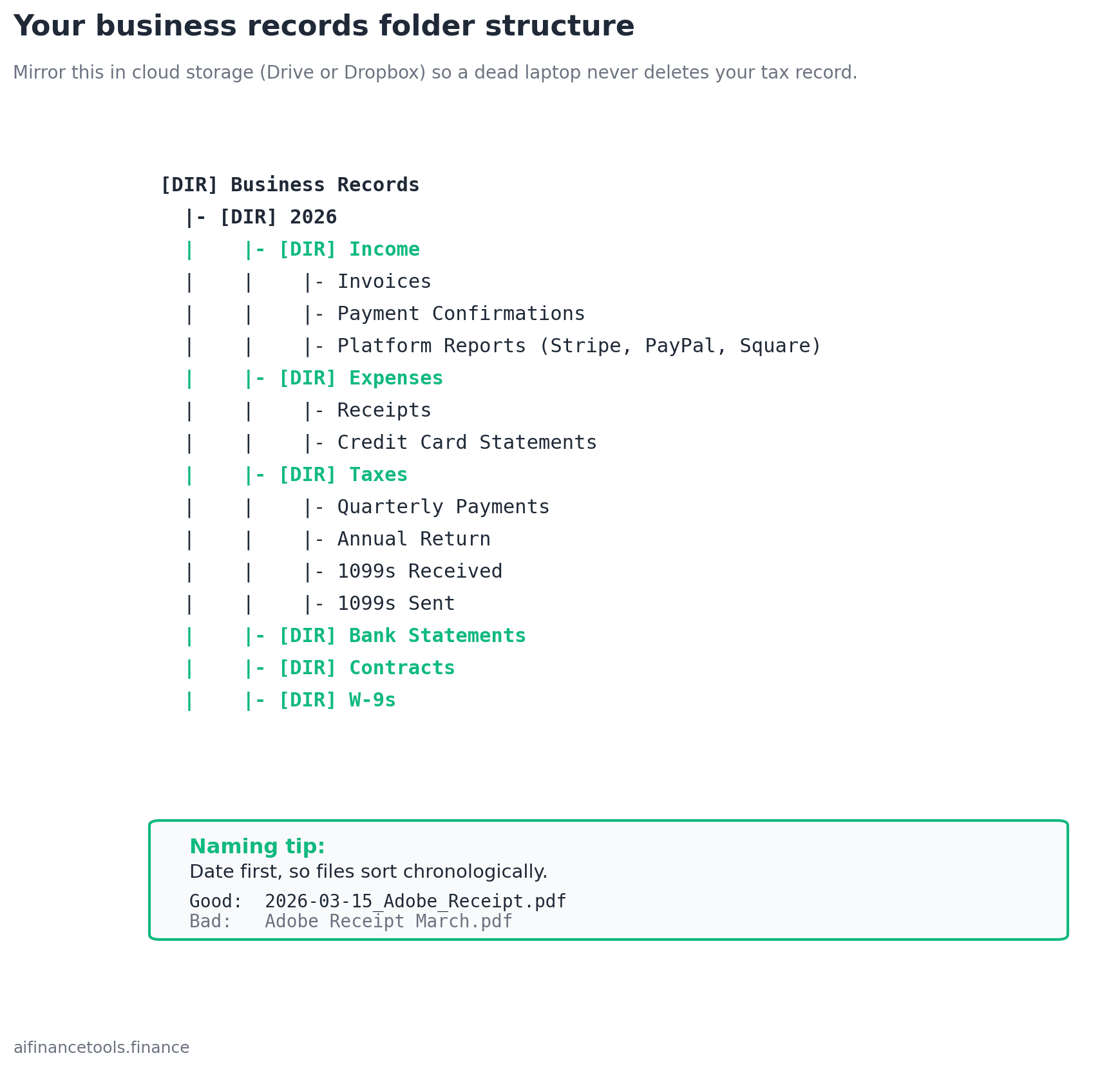

Option 1: Digital folder system

Build a folder hierarchy on your computer and mirror it in cloud storage like Google Drive or Dropbox. The cloud copy is not optional. Hard drives fail. Computers get stolen. A receipt photo that lives only on your phone disappears the moment the phone does.

A workable structure:

Name files with the date first so they sort chronologically: 2026-03-15_Adobe_Receipt.pdf rather than Adobe Receipt March.pdf. The two seconds of typing pays back the next time you need to find something.

The catch with a manual folder system is that it only works if you stay on top of it. Files saved in the wrong place. Receipts that never get scanned. Statements never downloaded. These gaps cause problems. If you’re going this route, attach the folder maintenance to a fixed weekly time slot.

Option 2: Physical filing system

Some freelancers prefer paper. If you do, use a two-drawer filing cabinet with labelled hanging folders organised by year and category. The same categories apply: income, expenses, taxes, bank statements, contracts.

The problem is receipts. Physical receipts fade. They tear. They go through the wash. Even if you prefer paper for larger documents, scan or photograph receipts and save the digital copy. The paper version becomes the backup, not the primary record.

Option 3: Accounting software (the option that removes most of the work)

Connect your business bank account and business credit card to accounting software. Transactions import automatically. The software categorises them by vendor and transaction type. You review and correct once a month in about 15 minutes.

The financial records stored in accounting software are also far more useful than a folder of PDFs. You can run a profit and loss statement in 30 seconds. You can see every transaction from a specific vendor across the year. You can generate the expense summary your accountant needs without assembling it yourself.

For most freelancers earning over about $40,000 in self-employment income, accounting software pays for itself in saved time and accountant fees within the first year. The exact tools and pricing are in the accounting software comparison guide.

Records when you’re paid through Stripe, PayPal, Venmo, and Square

Each platform handles year-end reporting differently. With the 1099-K threshold reverted to $20,000 and 200 transactions, most freelancers won’t get a form from these platforms. You still need your own records of every payment. Pull the right report from each.

Stripe

Dashboard > Reports > Balance summary or Payments report. Set the date range to January 1 through December 31. Export as CSV. Stripe charges 2.9% plus 30 cents per transaction in the US, deducted from each payment before deposit. Report the gross amount on Schedule C Line 1, then deduct the fees on Line 27a (other expenses) or wherever your accountant categorises payment processing costs. The fees are fully deductible.

PayPal

Activity > Statements > Annual statement. Distinguish between Goods & Services payments (business income) and Friends & Family payments (which the IRS treats as personal transfers). If a client tries to pay you via Friends & Family to dodge the 2.9% fee, decline. It creates messy records and can land both of you in tax trouble. PayPal also issues separate reports for refunds and chargebacks. Pull these so your reported income reflects net amounts correctly.

Venmo

Personal Venmo accounts don’t issue 1099-Ks regardless of volume. Venmo for Business does, subject to the $20,000 / 200-transaction threshold. If clients pay you via personal Venmo, you’re entirely on your own for record-keeping. Push them to a Venmo for Business account or move them to Stripe. Pull your transaction history from the Venmo app under Statements.

Square

Reports > Sales > Sales summary. Set custom date range January 1 to December 31. Export as CSV or PDF. Square charges 2.6% plus 10 cents for in-person card payments, 2.9% plus 30 cents for online. Same Schedule C treatment as Stripe.

The reconciliation step nobody mentions

Once a year, sum the gross amounts from every platform plus direct bank deposits. That number should equal your reported gross receipts on Schedule C Line 1. If it doesn’t, you’ve either missed payments or double-counted. Fix the discrepancy before filing. The IRS computer matches what platforms reported against what you reported, and mismatches generate automated CP2000 notices.

Your Maintenance Schedule for Consistent Accounting Records

Clean records don’t require large blocks of time. They require small, regular habits done on a fixed schedule.

Weekly: 15 to 20 minutes

Once a week, open your accounting software or your bank account and do four things. Review any new transactions that imported and confirm they’re in the right category. Attach any receipts you collected during the week to their matching transactions. Check your mileage log and make sure any business driving from the past week is recorded. Scan or photograph any paper receipts before they get lost or fade.

Doing this weekly instead of monthly cuts the time per session a lot, because you’re working with a few transactions at a time rather than sorting through 60 or 80 at once. It also means errors get caught within days rather than discovered months later.

Monthly: 30 to 45 minutes

At the end of each month, do a full bank reconciliation. Compare the transactions in your accounting software against your actual bank statement to confirm they match. Catching discrepancies monthly prevents mistakes from compounding and ensures financial reports reflect true cash positions.

Check for any transactions that are miscategorised or missing. Review the month’s expenses for anything sitting in a catch-all category. Check accounts receivable: are there invoices that should have been paid that are now overdue? Send the follow-up now rather than three months from now. Our invoicing software guide covers automated payment reminders if you’re sending follow-ups manually.

Pull a profit and loss statement for the month. You don’t need to analyse it deeply. Seeing your income and expenses summarised gives you a real picture of how the month went. That picture helps you decide whether to take on a new project, whether a software subscription is still worth keeping, and whether you’re on track for the year.

Quarterly: one to two hours

Your quarterly session has two tasks. First, review your estimated quarterly tax payment. Pull your income and expenses for the quarter, calculate what you owe, and make the payment by the due date. April 15, June 15, September 15, and January 15 are the four deadlines. Missing them costs you a penalty calculated on the amount underpaid.

Second, review your records for completeness. Are all receipts accounted for? Is your mileage log current? Are your client contracts on file? A quarterly pass through your records is easier to manage than an annual one and catches anything that slipped through the weekly and monthly habits.

Annually: two to four hours

Your annual session prepares everything your accountant needs to file your return. If you’ve maintained your records through the year, this session is largely a review rather than a rebuild. Confirm your income total matches your bank deposits and platform reports. Confirm your expense categories are complete and correctly classified. Confirm you have documentation for every major deduction.

Export the reports your accountant requests: profit and loss, expense summary by category, mileage log total. If you’re using accounting software, most of these are available in two clicks. If your records are complete, this session shouldn’t feel stressful.

Bank reconciliation: the step most freelancers skip

Bank reconciliation sounds technical. The idea is simple. You’re comparing two records of the same transactions: what your accounting software says happened, and what your bank statement says happened. When they match, your records are accurate. When they don’t, something needs investigation. A clean reconciliation is the audit trail your records depend on.

Most modern accounting tools handle the matching automatically. You review what imported, confirm the categories, and mark transactions as reconciled.

Without reconciliation, errors stack up silently. A transaction gets recorded twice. A payment lands in the wrong category. A bank fee you didn’t notice gets missed as a deductible expense. Small errors over twelve months distort your profit picture by enough to matter. A freelancer making decisions based on inaccurate numbers is making those decisions blind.

Reconciliation also catches fraud and unauthorised charges early. If a vendor charges you incorrectly or an unauthorised transaction appears on your card, you see it in the current month rather than six months later, when disputing it becomes much harder.

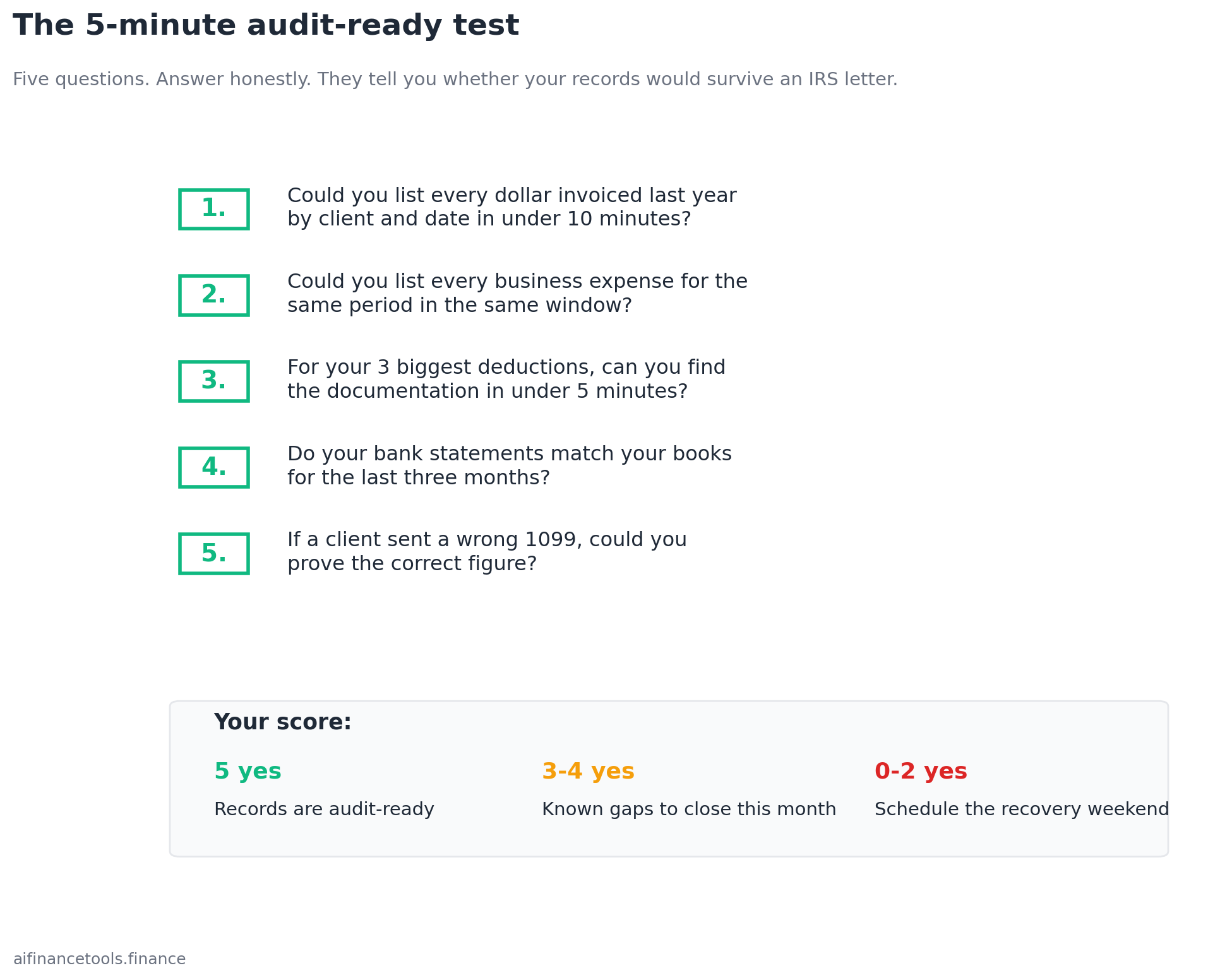

The 5-minute audit-ready test

Five questions. Answer each honestly in five minutes. They tell you whether your records would survive an IRS letter without panic.

- Could you produce a list of every dollar you invoiced last year, by client and date, in under 10 minutes? If yes, your income records are intact. If no, your accounts receivable tracking has gaps.

- Could you produce a list of every business expense for the same period in the same window? If no, you’re either missing transactions or sitting on a “miscellaneous” pile too thick to sort.

- For your three biggest deductions, could you find the documentation in under five minutes? Home office square footage, mileage log, equipment receipts. If any are missing, you’re at risk if those deductions get questioned.

- Do your bank statements match what’s in your books for the last three months? If they don’t reconcile, you don’t have an accurate picture of your business.

- If a client sent you a duplicate 1099 or one with the wrong amount, could you prove the correct figure? If you can’t reconcile platform reports against bank deposits and invoices, you can’t dispute incorrect 1099s.

Score yourself. Five yes answers means your records are audit-ready. Three or four yes answers means you have known gaps to close. Two or fewer means schedule a recovery weekend (next section).

What an audit actually looks like

The word “audit” provokes more fear than the reality usually warrants. The IRS uses computer screening through its Discriminant Function System (DIF) to compare your tax return against statistical norms for similar returns. Selection for an audit doesn’t always mean you’ve done something wrong.

Most audits for self-employed individuals are correspondence audits. The IRS mails you a letter (typically a CP2000 notice or an examination letter such as Letter 566 or 525) asking for documentation on one or two specific deductions. You gather the records and mail them back, usually within 30 days. If the records are there, the deduction stands. The whole process takes a few weeks.

Common audit triggers for Schedule C filers include unusually high expense ratios compared to income, claiming 100% business use of a vehicle without owning a second car for personal use, home office deductions that look disproportionate to income, large meal deductions, and consistent net losses across multiple years. None of these triggers automatically create a problem. They mean the IRS may want to see the records. If the records exist and are accurate, the audit closes cleanly.

The practical implication: keep your records in a state where you could respond to a 30-day notice by the end of next week. That’s the standard consistent record-keeping achieves.

The recovery weekend: cleaning up six months of mess

If your records are six months behind, you don’t need a full year to fix them. You need a weekend.

Saturday: build the income and expense backbone

Pull every bank statement and credit card statement from January 1 through last month. If you have a business account and a personal account both being used for business expenses, pull both. Open a free trial of accounting software (FreshBooks or Xero offer 30 days). Connect both accounts and let transactions import.

Categorise everything. The software will guess at categories based on vendor names. You confirm or correct. Most freelancers can categorise six months of transactions in three to four hours. Anything that doesn’t have an obvious category, leave as “Uncategorised” and come back to it. Better to be honest about what you don’t know than to mis-categorise.

Pull every income deposit, including direct bank transfers, ACH, Stripe payouts, and any check deposits. Match each to an invoice if you have one. If you don’t, write down what work the payment was for while you can still remember.

Sunday: receipts, mileage, and quarterly catch-up

Sunday morning, gather receipts from every source you can think of. Email folders. Photos on your phone. The shoebox or drawer. Vendor accounts where you can re-download (Adobe, Apple, Google, AWS, your software subscriptions all keep digital records). Attach the important ones (over $75, or for vehicle, home office, or meals) to the matching transactions in your accounting software.

Reconstruct your mileage log if you have one to rebuild. Use your calendar to identify business trips. Pull Google Maps trip history if you’ve enabled it. Estimate conservatively for trips you can document with calendar entries even without exact mileage.

Calculate your year-to-date Q1 and Q2 estimated tax based on the now-cleaner numbers. If you’ve underpaid, make a catch-up payment with Form 1040-ES through the IRS Direct Pay system. The penalty is calculated quarter by quarter, so paying late is still better than paying nothing.

Two days. Six months of records cleaned up. The remaining six months become a weekly habit so you never have to do this again.

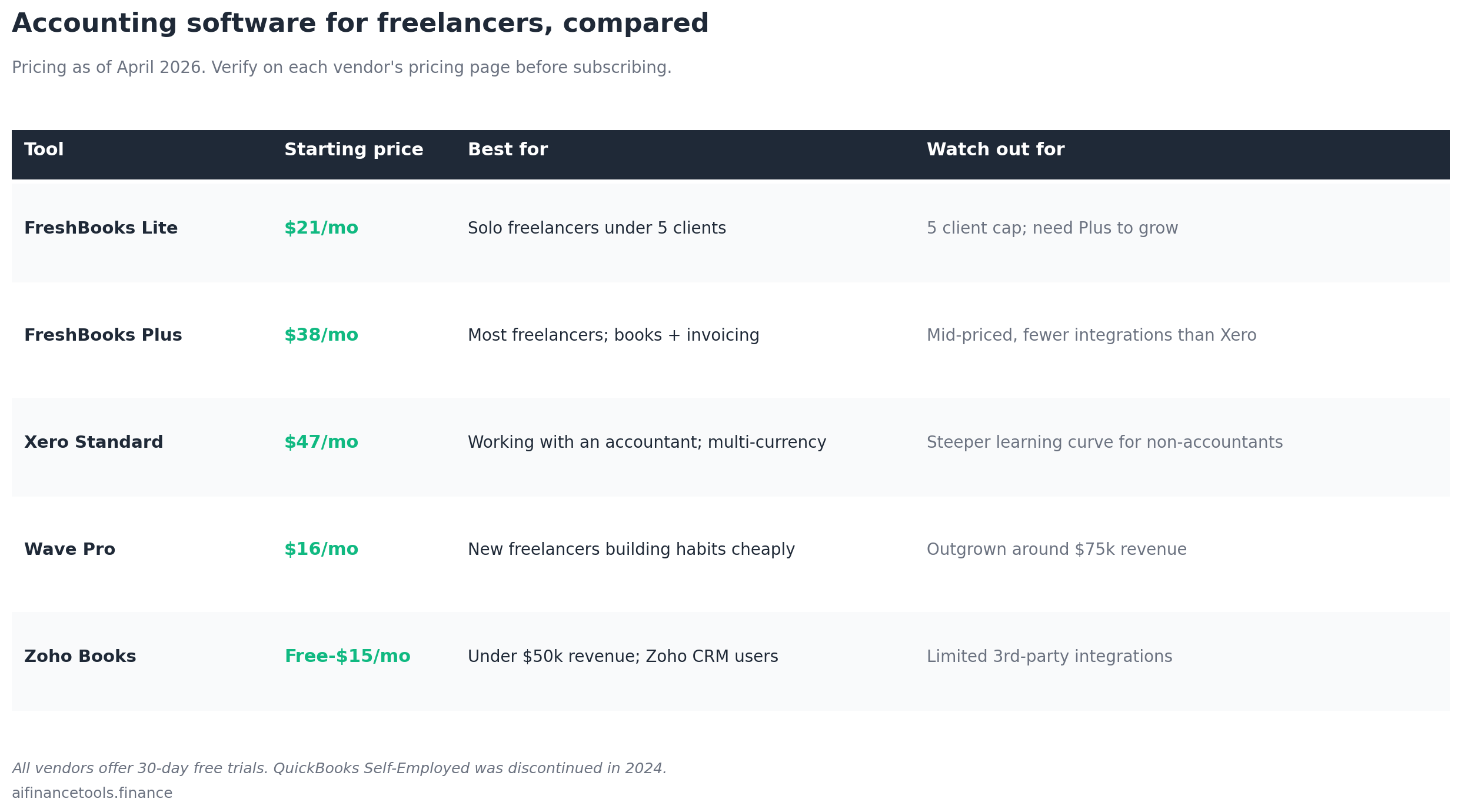

The Tools That Build Consistent Accounting Records for You

The right accounting software doesn’t just store records. It builds them as you go, reducing weekly maintenance to a quick review rather than manual data entry. Pricing below is current as of April 2026. Verify on each vendor’s pricing page before subscribing.

A note on QuickBooks for freelancers

If you’ve been searching for QuickBooks Self-Employed, that product is gone. Intuit launched QuickBooks Solopreneur in February 2024 and stopped offering QuickBooks Self-Employed to new customers. Existing QBSE users have been migrated or given the option to switch. Solopreneur kept the tax-focused features (estimated quarterly tax estimates, mileage tracking, basic expense categorisation) but is more limited than QuickBooks Online. If you’re starting fresh in 2026, the alternatives below are generally stronger options for freelancers under $150,000 in revenue. If you were a QBSE user, check whether Solopreneur still meets your needs or whether a migration to FreshBooks or Xero would serve you better.

FreshBooks

Best for: Freelancers who want invoicing, expense tracking, and record-keeping in one tool without a steep learning curve.

FreshBooks connects to your business bank account and imports transactions automatically. It categorises expenses by vendor and lets you attach receipt photos directly to each transaction so the documentation lives next to the number it supports. Invoices store automatically the moment you create them. The expense report view shows every category with totals at a glance, which is the report you hand your accountant.

Common complaints from G2 and Capterra reviewers: the Lite tier ($21/month) caps you at 5 billable clients, which most active freelancers outgrow within a year. The Plus tier ($38/month) raises that cap and adds double-entry accounting. Customer support is generally well-reviewed compared to Intuit’s products.

Pricing as of April 2026: Lite around $21/month, Plus around $38/month. Verify on freshbooks.com/pricing.

Xero

Best for: Freelancers who work with an accountant or bookkeeper, need professional-grade reporting, or invoice international clients in multiple currencies.

Xero offers unlimited users on every plan, strong bank reconciliation tools, and good project tracking. The dashboard provides clear financial overviews without overwhelming detail. Multi-currency support is the standout feature for freelancers with clients in the UK, EU, or Australia. It handles exchange rate conversions automatically for invoicing and reporting.

The unlimited users matter most if you have an accountant. They log in directly to pull the reports they need rather than asking you to export and email files. That alone is worth one to two billable hours saved at tax time.

Pricing as of April 2026: Starter around $20/month (limited invoices), Standard around $47/month (most freelancers need this plan). Verify on xero.com/us/pricing.

Wave

Best for: New freelancers who want to build record-keeping habits without a monthly software fee.

Wave’s core invoicing and manual expense tracking is free. Bank transaction import (the feature that does most of the work) moved to the Pro plan in 2024, currently around $16/month. Receipt scanning works through the mobile app. For straightforward record-keeping without complex reporting needs, Wave Pro covers the basics at a lower cost than FreshBooks or Xero.

The trade-off: Wave is owned by H&R Block and the product roadmap has prioritised integration with their tax filing service. Some advanced features available in FreshBooks and Xero (project tracking, time tracking, robust accounts receivable aging) are limited or missing. As your income grows past about $75,000, you’ll likely outgrow Wave.

Zoho Books

Best for: Freelancers who want strong features at a lower price point, or those already using other Zoho products.

Zoho Books is free for businesses earning under $50,000 in annual revenue. Paid plans start around $15/month. The expense tracking and bank reconciliation are detailed, receipt scanning works well, and the integration with Zoho CRM works smoothly if you already use it for client management. Outside Zoho’s other products, third-party integrations are more limited than Xero or FreshBooks offer.

Four Habits That Keep Your Accounting Records Consistent

The tools help. The tools only work when the habits are in place. These four practices, done consistently, separate freelancers who sail through tax season from those who dread it.

1. Photograph receipts the moment you get them

Every accounting tool lets you snap a photo with your phone and attach it to a transaction. Do this in the parking lot, at the coffee shop table, or the moment you sit back down at your desk. Paper receipts fade. Digital photos stored in your accounting software are retrievable years later. The 30-second window between the purchase and moving on with your day is when the business purpose is clearest in your memory. The IRS calls these contemporaneous records, and they carry more weight in an audit than reconstructed records do.

2. Use one dedicated card for all business purchases

Every business expense goes on your business card. No exceptions. Your statement becomes a near-complete record of expenses, sorted by date and vendor automatically. Cash purchases are the exceptions, and those are the ones that need deliberate documentation. Mixing personal and business on one card is the single biggest cause of messy records and the most common reason CPAs run up billable hours during tax season. Our guide on tracking business expenses as a freelancer covers how to set this up.

3. Never use “miscellaneous” as a category

Vague categories like “miscellaneous” stand out to an IRS auditor. If you can’t categorise something clearly, the answer is to think harder about the business purpose, not to file it under a catch-all. Specific, consistent categories that mirror the lines on Schedule C make your records readable and defensible.

4. Reconcile every month without exception

Monthly reconciliation is what keeps records reliable. Quarterly reconciliation lets errors compound before you catch them. Regular bank statement reviews also improve your cash flow forecasting, which our cash flow guide covers in detail. Set a recurring 45-minute calendar block on the last working day of each month and treat it as non-negotiable as a client deadline.

When your records tell you something useful

Good records do more than satisfy the IRS. They give you data that improves how you run your business.

A web designer reviewing her March P&L noticed she’d spent $340 on Adobe Creative Cloud, $89 on Figma, and $59 on Webflow. Three tools doing overlapping work for her workflow. She cancelled Webflow and saved $708 a year. That decision was only possible because her records were clean enough to surface the line items in 30 seconds.

An accurate profit and loss statement tells you your real margin. You can see which months are consistently strong and which are slow, which lets you plan cash reserves rather than reacting to shortfalls. You can see whether a specific client relationship is profitable after accounting for all the software, subcontractors, or travel it required.

When you apply for a business loan, a line of credit, or want to lease office space, your financial records are what lenders and landlords review. Organised books show a credible, professionally run operation. Disorganised records (or no records) create doubt that’s hard to overcome no matter how well your business is actually performing.

Get your free record keeping checklist

I’ve put together a Record Keeping Checklist that covers every document category, how long to keep each type, the records-by-deduction-type table from this article in printable form, and a monthly maintenance calendar you can stick on your wall. Most freelancers find at least two or three records they weren’t keeping when they go through it the first time.

Frequently Asked Questions

How long should I keep tax records and financial documents?

Three years from the date you filed the return covers most situations. Six years covers the IRS window for auditing substantial under-reporting (more than 25% of gross income). Seven years covers nearly everything, including most audit scenarios involving losses or bad debt. Some states require longer (California has a 4-year window for state returns). In practice, keeping everything for seven years is simpler than tracking each document by retention period.

Does the IRS accept photos of receipts?

Yes. The IRS accepts digital copies of receipts under Revenue Procedure 97-22, provided your storage system maintains accurate, complete, legible copies that can be retrieved on request. The advantage of digital is that photos don’t fade, can’t be lost in a move, and are searchable. Attach receipt photos to their matching transactions in your accounting software so the documentation lives with the number it supports. For a few documents like signed contracts and business insurance policies, keeping both physical and digital copies is reasonable.

What if I’m missing a receipt for a legitimate expense?

For most expenses, a bank or card statement showing the vendor, date, and amount provides supporting evidence, though it doesn’t fully replace a receipt. The Cohan rule (from a 1930 court case) lets the IRS allow reasonable estimates for expenses where you can prove the activity occurred but don’t have exact documentation. The Cohan rule does not apply to travel, meals, gifts, or vehicle expenses, which require strict substantiation under IRC Section 274(d). For those categories, missing documentation usually means the deduction is lost. The fix is preventive: photograph receipts the moment you get them.

How do I handle records when clients pay through five different platforms?

Pull a year-end report from each platform (Stripe, PayPal, Square, Venmo for Business, plus your bank for direct deposits). Sum the gross amounts. That total should match the gross receipts on Schedule C Line 1. If accounting software is connected to your bank, most of this matches automatically. The reconciliation step is comparing platform reports against bank deposits to catch any payments that arrived but didn’t make it into your books.

Should I use a spreadsheet or accounting software?

Accounting software for anything beyond the simplest freelance setup. A spreadsheet requires manual data entry for every transaction, which you’ll skip when you’re busy and catch up on inconsistently. Software imports transactions from your bank automatically, reduces data entry errors, generates reports your accountant can use directly, and stores receipts attached to transactions. The monthly cost is usually recovered in accountant fee savings within the first year.

When should I hire a bookkeeper instead of doing this myself?

Most freelancers can handle their own bookkeeping with accounting software through about $150,000 in revenue. Consider hiring a part-time bookkeeper if you’re spending more than four hours a month on financial admin, your income justifies the cost, or you have complex transactions (multiple states, international clients, subcontractors). A part-time bookkeeper usually charges $200 to $500 per month and handles weekly maintenance, monthly reconciliation, and reporting. If record-keeping is consistently taking time away from billable work, the math usually favours outsourcing.

What’s the biggest mistake freelancers make with their records?

Waiting until tax season to organise everything. By January, you’ve lost receipts, forgotten the business purpose of transactions, and face a multi-day project that a weekly 15-minute habit would have eliminated. The second-biggest mistake is mixing personal and business finances in one account, which makes every tax season harder than it needs to be and increases audit risk if questioned.

Did the OBBBA change my record-keeping requirements for 2026?

It changed who sends you 1099s, not what you need to track. Starting January 1, 2026, the 1099-NEC threshold rises from $600 to $2,000, so clients who paid you between $600 and $1,999 will no longer be required to send a form. The 1099-K threshold from payment platforms reverted to $20,000 and 200 transactions, so most freelancers won’t get a form from Stripe, PayPal, or Square. You still owe tax on every dollar regardless of whether a form arrives. With fewer forms in the mail, your own bank deposit records and platform reports become the primary evidence of income.

Start here

If you don’t have a dedicated business bank account, open one this week. That single decision makes every other record-keeping habit dramatically easier.

After that, pick one accounting tool and connect your bank account. The first month, spend 20 minutes reviewing what imported. Correct any miscategorised transactions. Attach receipts. Run a profit and loss statement to see what your month actually looked like. Do that every month, and tax season stops being stressful.

For the broader system, the expense tracking guide and the freelancer tax deductions guide on this site cover the rest of the workflow from capturing expenses to claiming them. The accounting software comparison goes deeper on the tool choice, and the cash flow guide covers how to use clean records to plan around freelance income swings.

This guide reflects IRS recordkeeping guidelines and OBBBA Act provisions current as of April 2026. Tax law changes regularly. Always verify retention requirements, 1099 thresholds, and documentation standards with a qualified tax professional for your specific situation. This guide is for informational purposes and does not constitute tax or legal advice.

About the author

Gareth is an entrepreneur based in Dubai and the founder of Freelancer Profit. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official IRS documentation, and expert sources.