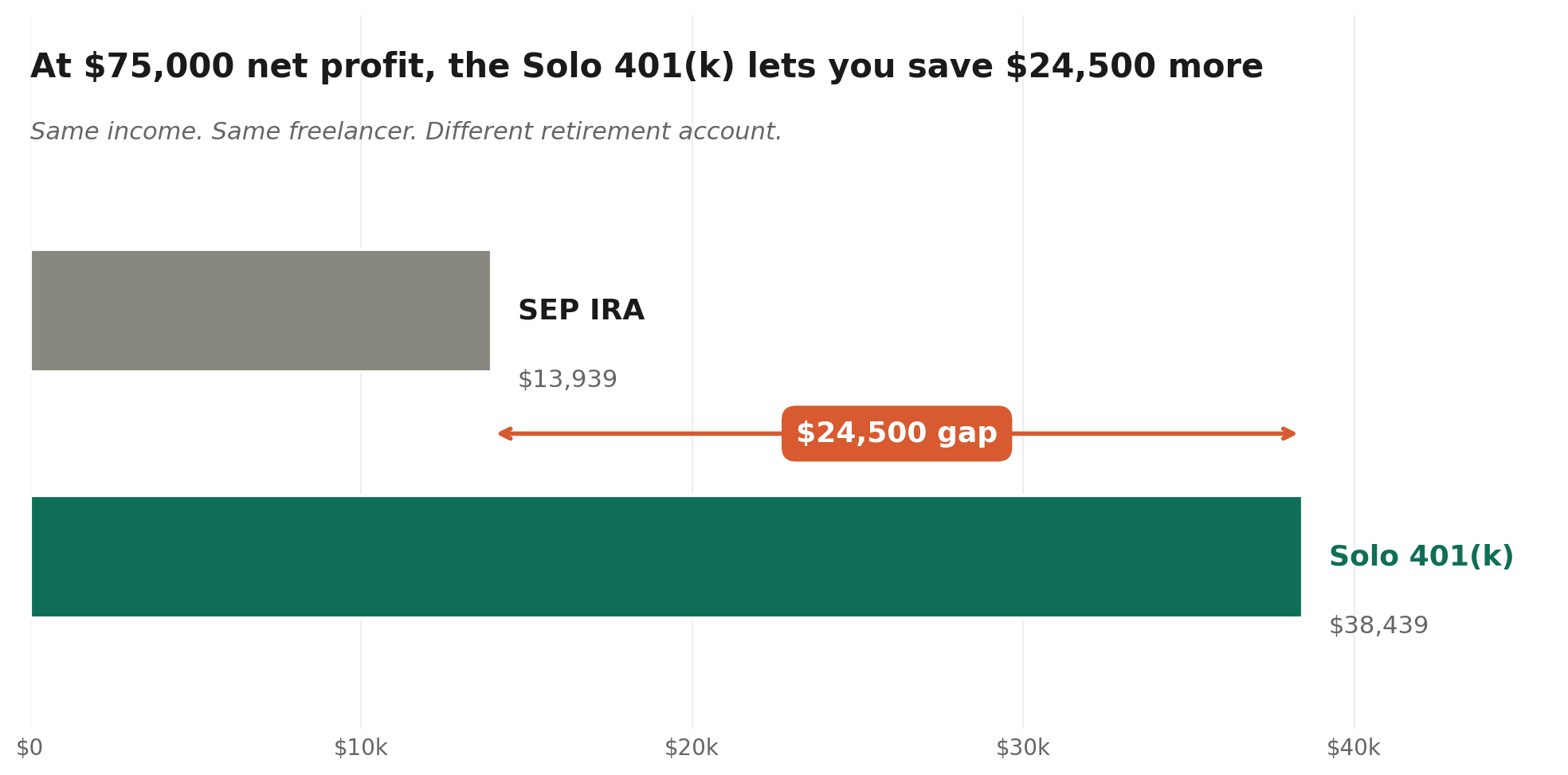

At $75,000 net profit, a Solo 401(k) lets you put away around $38,439 for 2026. A SEP IRA caps you at roughly $13,939 on the same income. Same person, same year, $24,500 gap. Here is when that gap matters and when it does not.

Solo 401k vs SEP IRA. Most freelancer retirement comparisons skip the part you actually need. They quote the headline $72,000 ceiling for both accounts and stop there. That ceiling is irrelevant for most freelancers reading this. You will never get near $72,000 on $80,000 of net profit. What matters is the contribution at your real income, and that is where these two accounts behave very differently.

This guide walks through the 2026 numbers, three worked examples at incomes a real freelancer might earn, the admin reality of running each plan, and a 5-minute decision framework. No theoretical scenarios about a six-figure W-2 plus side hustle. Just the math for a solo Schedule C filer trying to decide what to open before December 31.

The 2026 headline numbers

The IRS released the 2026 retirement plan limits in Notice 2025-67 on November 13, 2025. Here is what those limits look like for a self-employed person with no employees other than a spouse.

- Solo 401(k) employee deferral: $24,500 if you are under 50.

- Solo 401(k) catch-up (ages 50 to 59 and 64+): additional $8,000, for a $32,500 employee total.

- Solo 401(k) super catch-up (ages 60 to 63): additional $11,250 instead of $8,000, for a $35,750 employee total.

- Solo 401(k) combined limit: $72,000 total under 50, $80,000 with the regular catch-up, $83,250 with the super catch-up.

- SEP IRA contribution: up to 25% of compensation, capped at $72,000.

- Compensation cap for both plans: $360,000.

The matching $72,000 cap makes the two accounts look equivalent. They are not. The 25% for a SEP IRA is calculated differently when you are self-employed, and the Solo 401(k) adds an employee deferral on top of the employer side. At lower and middle freelancer incomes the Solo 401(k) wins by a wide margin. The next section shows the math.

How much can you actually contribute at your income?

The 25% figure you see quoted for both plans is the headline number. The IRS calculation for a sole proprietor is different. You start with net profit from Schedule C, subtract one half of self-employment tax, and apply the contribution rate to that adjusted figure. For the SEP IRA and the employer profit-sharing side of a Solo 401(k), the effective rate works out to around 20% of net profit. The IRS publishes the worksheet in Publication 560.

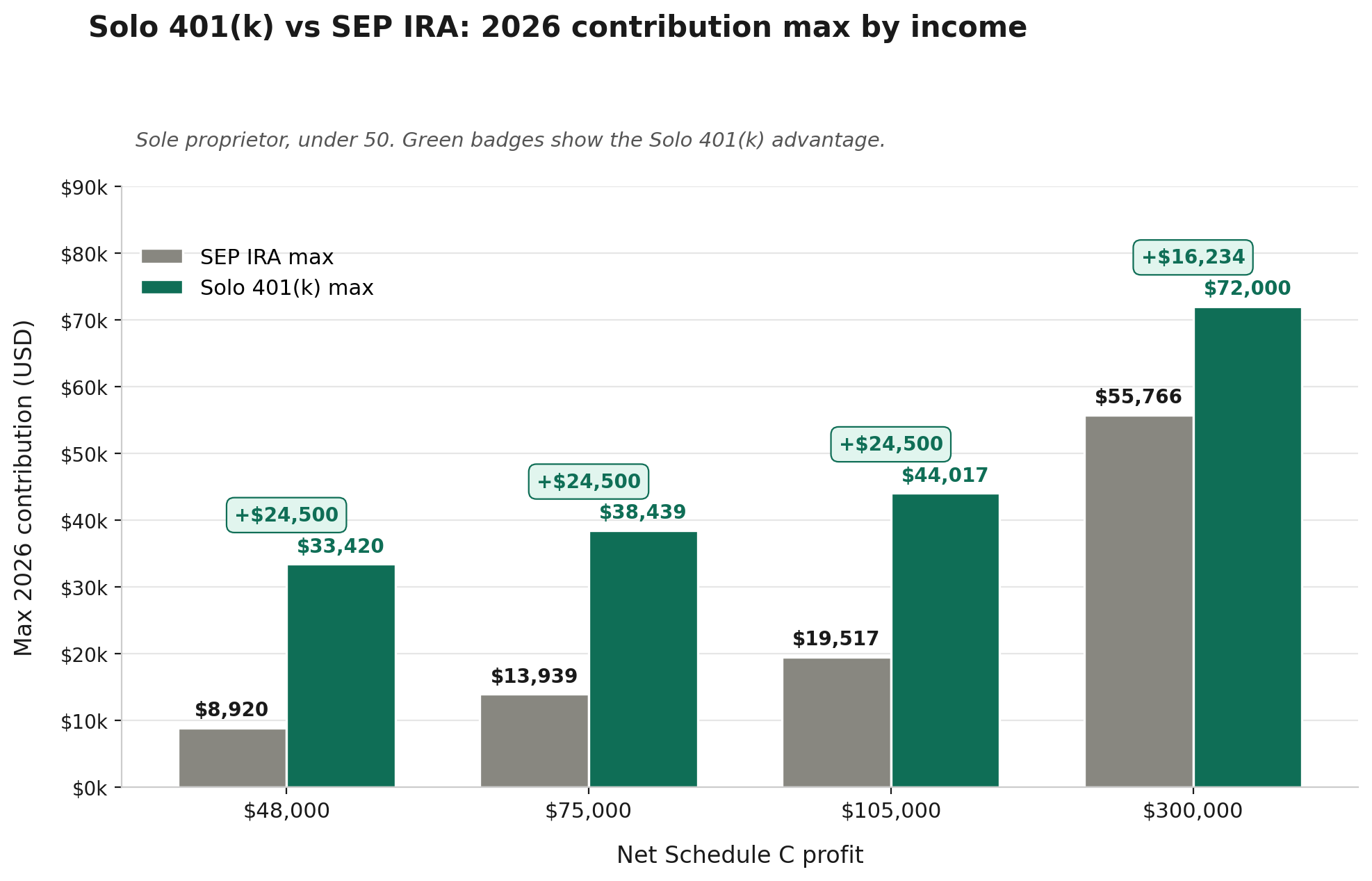

Here is what that looks like for three freelancer income levels. All examples assume a sole proprietor under 50, with the income figure being net profit on Schedule C before any retirement contribution.

The Solo 401(k) advantage sits at $24,500 across most of the freelancer income range. That is the employee deferral. The SEP IRA has no employee side. You get the employer percentage and nothing else, which at $75,000 of profit works out to about $13,939. The Solo 401(k) lets you add that $13,939 on top of the $24,500 employee deferral.

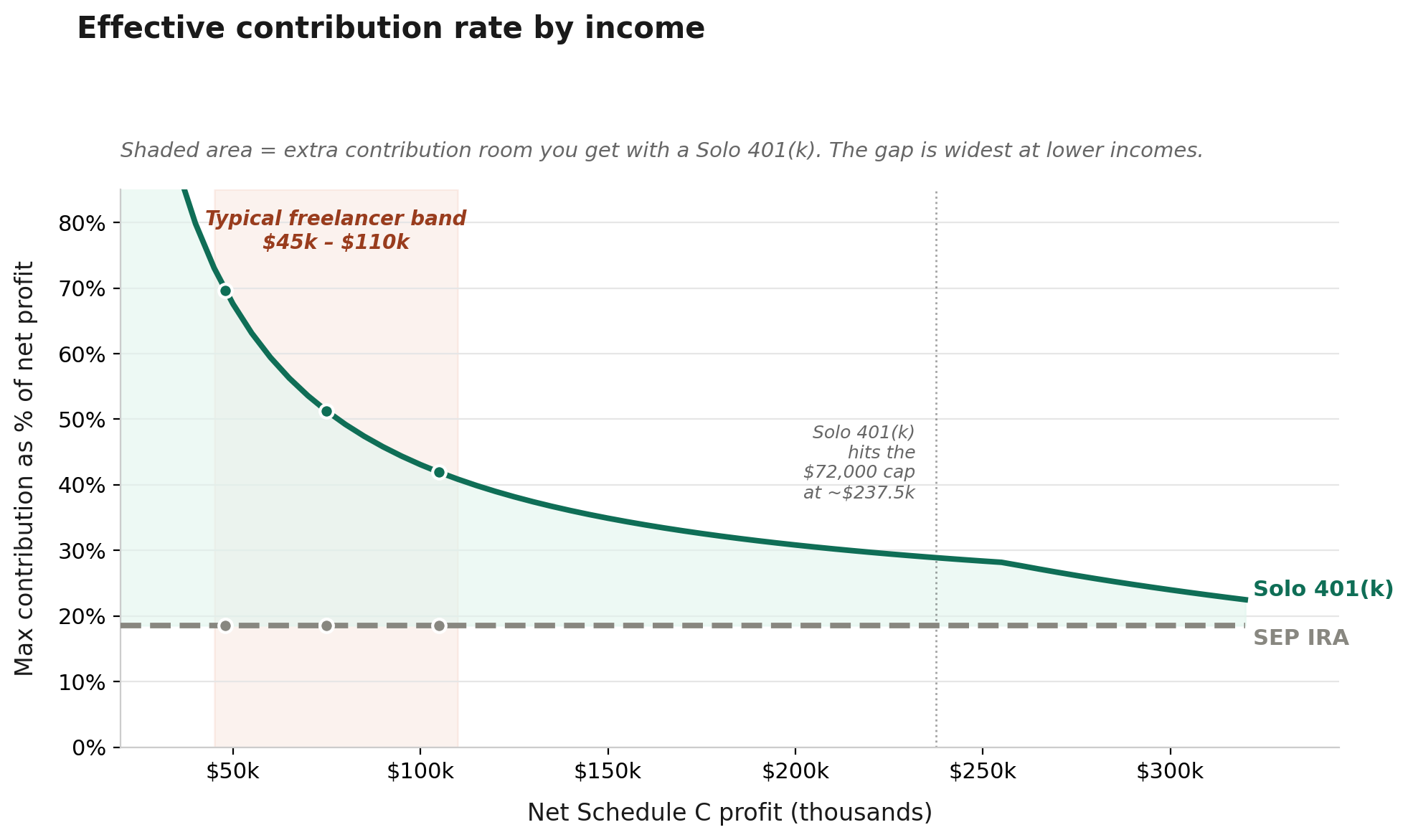

The two accounts only converge at high incomes. A SEP IRA hits the $72,000 cap at around $360,000 of compensation. A Solo 401(k) hits the same cap at roughly $237,500 of net profit. If you earn seven figures from your business with no employees, both accounts let you put away the same $72,000. If you earn $60,000, the Solo 401(k) lets you save five times more.

Three worked examples at real freelancer incomes

A freelance copywriter making $48,000 (under 50)

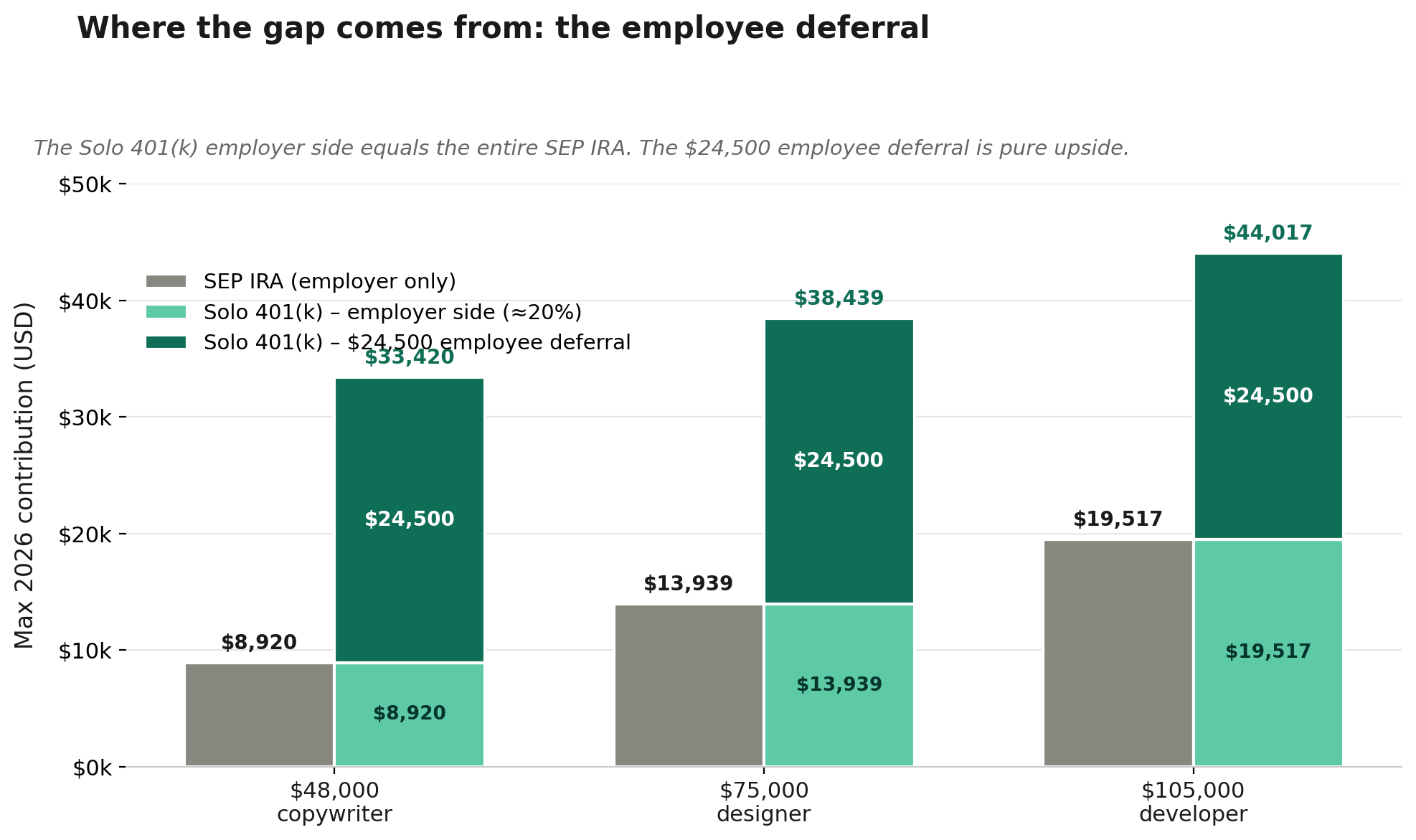

Net profit of $48,000 gives you roughly $44,608 of adjusted earnings after the SE tax adjustment. A SEP IRA contribution at the maximum is about $8,920, which works out to 20% of adjusted earnings. With a Solo 401(k), you get the same $8,920 as your employer profit-sharing contribution. On top of that, you get a full $24,500 employee deferral. Total: $33,420.

At $48,000, the Solo 401(k) is the only account that lets you save anything close to a meaningful percentage of your gross. A SEP IRA limits you to about 18.6% of gross. A Solo 401(k) gives you the option to save 70% of your net if you want to. Most freelancers earning $48,000 cannot defer $33,420. The option still matters. In a strong month or a windfall quarter, you have somewhere to put the money.

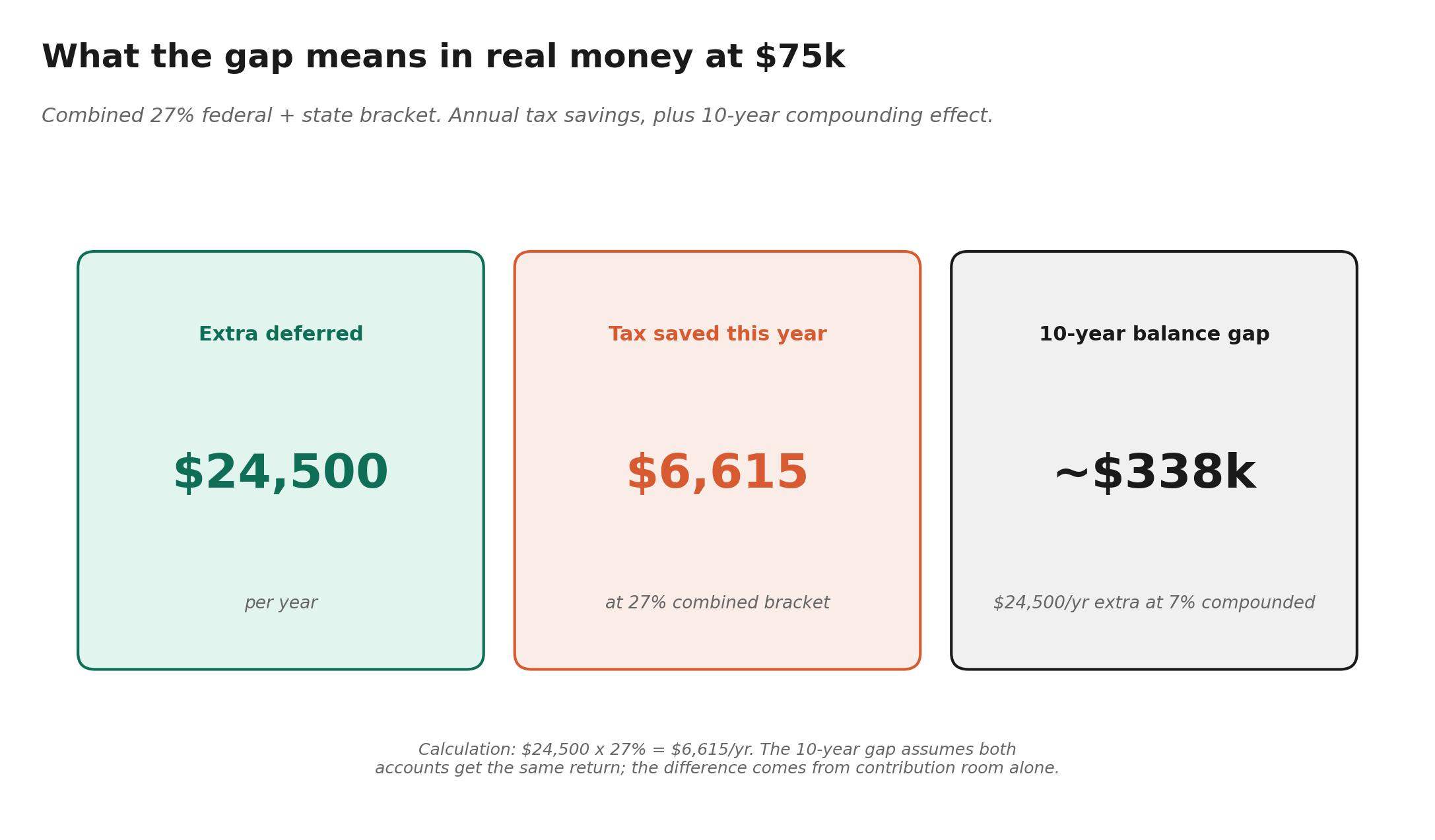

Solo 401k vs SEP IRA at $75,000: the designer example

This is the income that breaks the “they’re basically the same” framing you see on most blog posts. Your adjusted earnings come to about $69,697. The SEP IRA maxes out at roughly $13,939. The Solo 401(k) maxes out at roughly $38,439 ($13,939 employer plus $24,500 employee). Same income. $24,500 difference.

If you sit in the 22% federal bracket and a 5% state bracket, that extra $24,500 of deferral is worth about $6,615 in current-year tax savings. Run that play for ten years and the gap stops being theoretical. The difference between a $400,000 retirement account and an $800,000 one at modest market returns starts to compound before you factor in what you do with the tax savings each April.

A freelance developer making $105,000 (under 50)

Net profit of $105,000 produces adjusted earnings of about $97,585. The SEP IRA contribution maxes out at $19,517. With a Solo 401(k), you get that same $19,517 as your employer contribution plus $24,500 as the employee deferral. Total: $44,017.

At this income level, the Solo 401(k) lets you defer more than 41% of net profit. The SEP IRA caps you at about 18.6%. If you want to defer aggressively in a strong year because next year looks lean, the Solo 401(k) is the only account that gives you that flexibility. A SEP IRA forces you to spend money you would rather save.

If you want the math at your exact income, our 2026 tax setaside calculator walks through the same SE tax adjustment used in the retirement contribution worksheets.

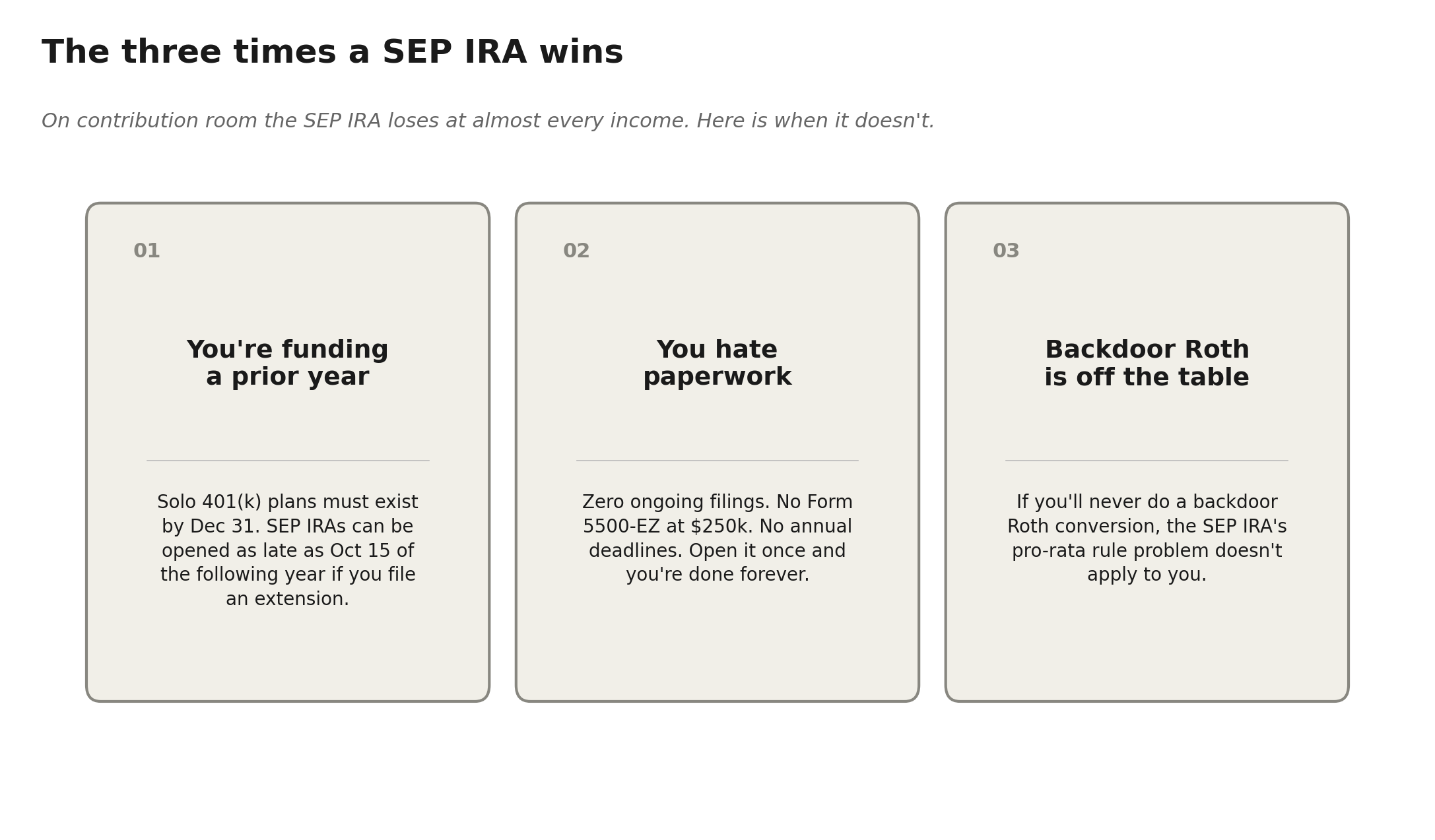

When does the SEP IRA actually win?

The SEP IRA loses on contribution room at almost every income level. It still wins on three specific things.

You want to set it up after the tax year ends

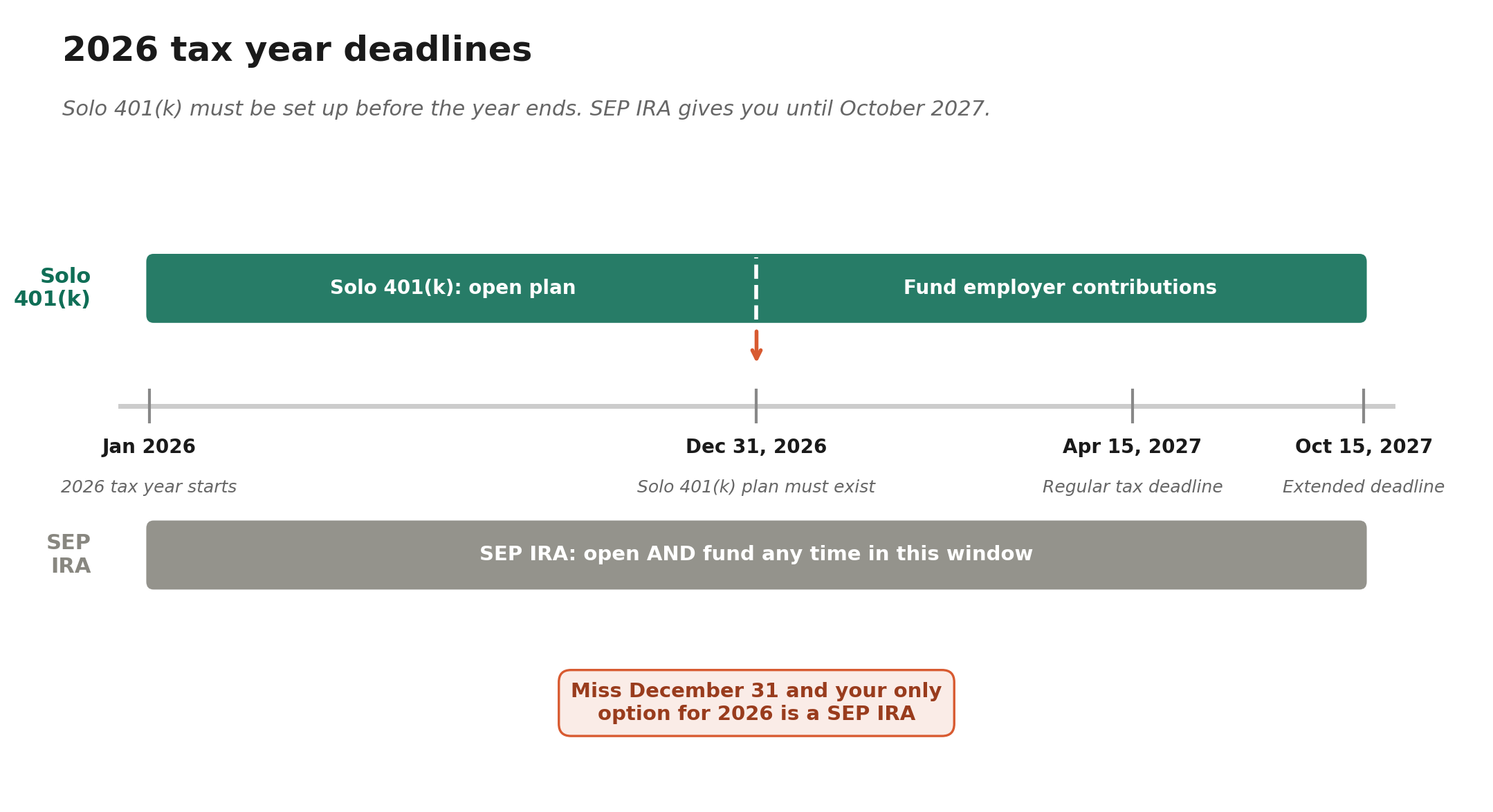

A Solo 401(k) must be established by December 31 of the tax year you want to contribute for. Miss December 31 and you have no plan. You can fund employer contributions after year-end, but the plan itself has to exist by midnight on December 31.

A SEP IRA can be opened and funded as late as your tax filing deadline including extensions. For the 2026 tax year, that means October 15, 2027 if you file an extension. This matters for freelancers who close their books in March and realize they had a better year than they thought. The SEP IRA is the only account that lets you fix this retroactively. One freelancer on Reddit’s r/tax described opening a SEP in April for the prior year specifically because they did not know how much they had made until their books were finally closed.

You hate paperwork more than you love optimization

A SEP IRA requires IRS Form 5305-SEP, which you keep in your records but do not file. There is no annual return. There is no ongoing compliance. You open the account at Fidelity, Schwab, or Vanguard in about 20 minutes and you are done.

A Solo 401(k) requires you to file Form 5500-EZ every year once plan assets cross $250,000. The form itself is short. About one page of basic plan information. The problem is that it is one more deadline (July 31 for most filers), one more thing to forget, and one more potential late-filing penalty if you ignore it. SECURE 2.0 raised the late filing penalty to $250 per day, capped at $150,000 per return, per IRS Form 5500 guidance.

You plan to do a backdoor Roth IRA every year

This is a specific tax planning point that catches a lot of high-earning freelancers. The backdoor Roth IRA strategy works by contributing to a non-deductible traditional IRA and converting it to a Roth. The conversion is tax-free only if you have no other pre-tax IRA balances. The IRS pro-rata rule treats all your traditional IRAs as one pool.

A SEP IRA is a traditional IRA. Its balance gets pulled into the pro-rata calculation. If you have $80,000 in a SEP IRA and you try a $7,500 backdoor Roth conversion, most of the conversion gets taxed. A Solo 401(k) sits outside the IRA pool and does not interfere. If you want both a big employer-side retirement plan and an annual backdoor Roth, the Solo 401(k) is the only clean option.

What about Roth contributions?

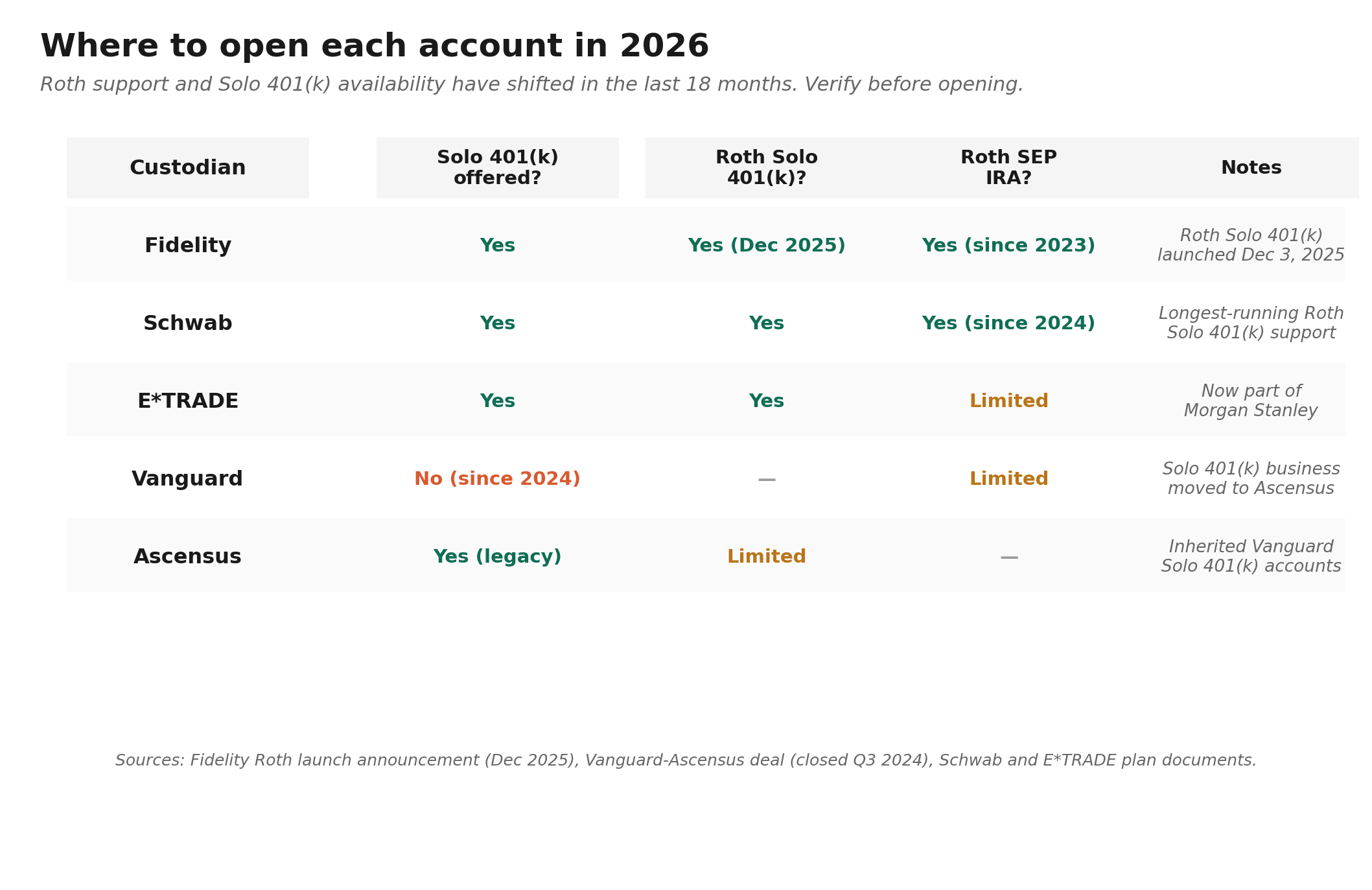

Before SECURE 2.0, SEP IRAs were pre-tax only. The 2022 legislation opened the door to Roth SEP IRAs. Custodian adoption has been slow and uneven. Fidelity launched a Roth SEP option in 2023. Schwab added Roth SEP support in 2024. Vanguard’s direct Roth SEP support remains limited as of early 2026. If Roth treatment matters to you, confirm with your provider before you assume it is available.

Solo 401(k) Roth deferrals have been around longer at Schwab and E*TRADE. Fidelity was the laggard. They only launched a Roth Self-Employed 401(k) on December 3, 2025. If you opened a Fidelity Solo 401(k) before that date, you only had pre-tax contributions available. Vanguard’s individual 401(k), Multi-SEP, and SIMPLE IRA business was sold to Ascensus in a deal announced April 16, 2024 and closed in the third quarter of 2024, so Vanguard no longer offers a direct Solo 401(k) at all. Vanguard does still offer a one-person SEP IRA. SECURE 2.0 also opened the door to Roth employer contributions, though provider support varies.

One nuance for 2026: the SECURE 2.0 mandatory Roth catch-up rule for high earners references W-2 wages, not self-employment income. If you are a sole proprietor with no W-2 wages, you are not the target of this rule. If you operate as an S-corp and pay yourself W-2 wages above $150,000 in 2025, your 2026 catch-up contributions to your Solo 401(k) must be Roth.

The common mistake: opening both and then doing nothing

You can technically have both a SEP IRA and a Solo 401(k) for the same business, but the combined limit is still $72,000. There is no stacking benefit. A long-running thread on Bogleheads from 2024 documented several freelancers who opened a SEP IRA at Vanguard in their first year of freelancing, then opened a Solo 401(k) at Fidelity a year later, then could not figure out how to roll the SEP into the Solo 401(k) without triggering tax issues.

Pick one. If you opened a SEP IRA in your first year and your income has grown past $50,000 of net profit, you can roll the SEP into a Solo 401(k) directly without tax consequences as long as your Solo 401(k) provider accepts incoming rollovers. Fidelity and Schwab both do. If your Solo 401(k) is now sitting at Ascensus because it transitioned from Vanguard in 2024, the rollover process is more painful. Several Ascensus customers have reported on r/personalfinance that the firm requires liquidation rather than in-kind transfers when you move out.

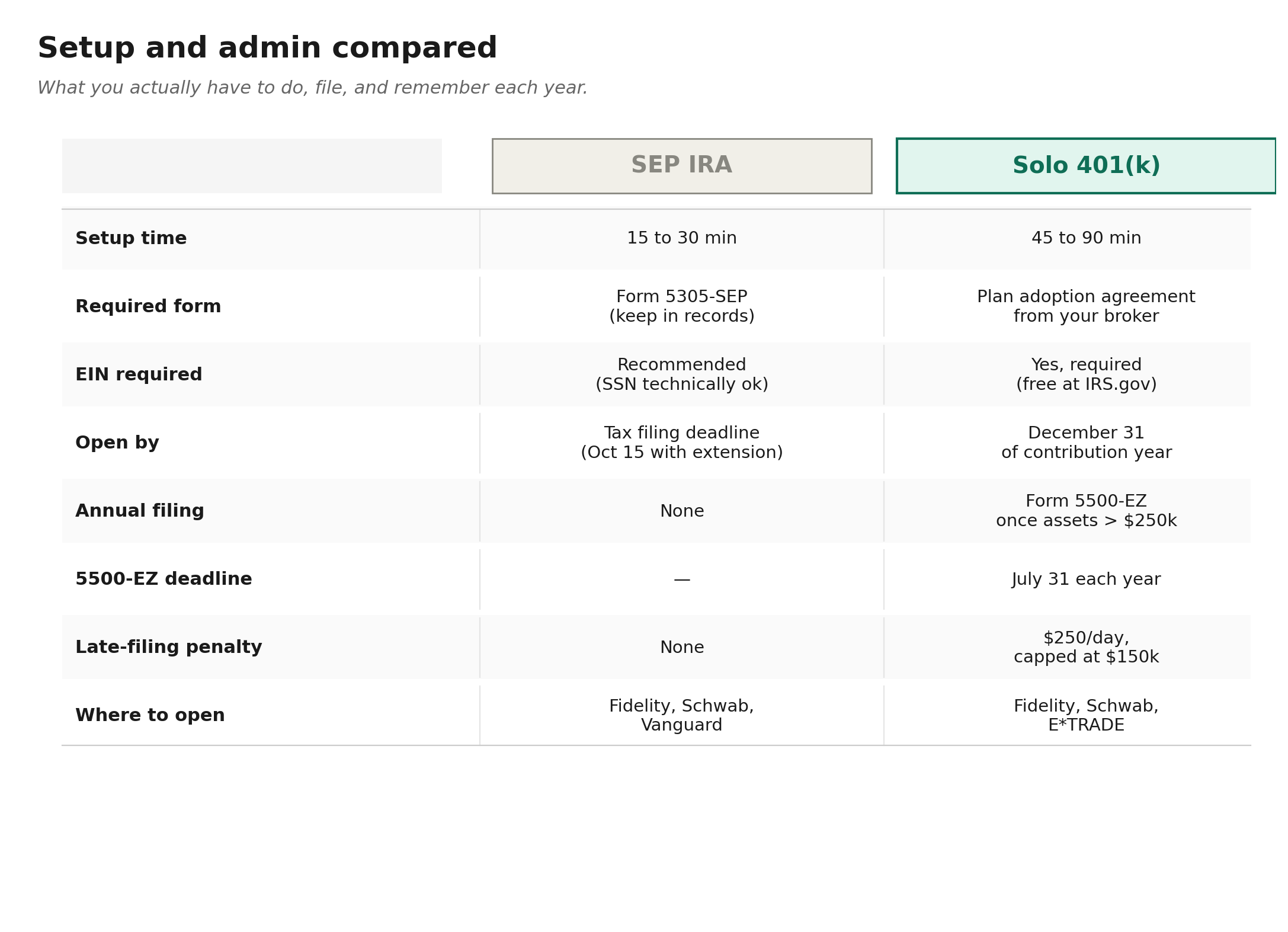

Setup and admin compared

| SEP IRA | Solo 401(k) | |

|---|---|---|

| Setup time | 15–30 minutes | 45–90 minutes |

| Required form at setup | Form 5305-SEP (keep in your records, do not file) | Plan adoption agreement from the brokerage |

| Deadline to open | As late as your tax filing deadline incl. extensions (Oct 15, 2027 for tax year 2026) | Must be established by Dec 31 of the tax year; employer contributions can be funded up to the filing deadline |

| Ongoing annual filing | None | Form 5500-EZ once plan assets exceed $250,000 (due July 31); final 5500-EZ when you close the plan |

| EIN required | No (SSN technically allowed, though most custodians ask for an EIN) | Yes — required |

SEP IRA setup

Open the account online at Fidelity, Schwab, or Vanguard. You will need your EIN, though sole proprietors can technically use a Social Security Number for a SEP IRA. The custodian provides Form 5305-SEP, which you sign and keep. Setup takes 15 to 30 minutes. No ongoing filings. No annual return. The custodian handles tax reporting (Form 5498) automatically.

Solo 401(k) setup

You need an EIN. The IRS issues these for free at irs.gov/EIN. You then open the plan with a major brokerage. Fidelity, Schwab, and E*TRADE all offer no-fee prototype Solo 401(k) plans. Vanguard’s individual 401(k) business moved to Ascensus in 2024 and Vanguard no longer offers a direct Solo 401(k). The brokerage provides the plan adoption agreement. Setup takes 45 to 90 minutes, longer if you also want Roth or after-tax options that are not included in the default plan document.

| Provider | Direct Solo 401(k)? | Roth Solo 401(k)? | Note |

|---|---|---|---|

| Fidelity | Yes | Yes — Roth Self-Employed 401(k) launched Dec 3, 2025 | Pre-tax only if you opened before that date. No-fee prototype plan. |

| Schwab | Yes | Yes (available longer) | Accepts incoming SEP rollovers. No-fee plan. |

| E*TRADE | Yes | Yes (available longer) | No-fee prototype plan. |

| Vanguard | No | — | No longer offers a direct Solo 401(k); business moved to Ascensus in 2024. Still offers a one-person SEP IRA. |

| Ascensus | Yes (former Vanguard plans) | Varies | Holds Solo 401(k) plans that transitioned from Vanguard in 2024; reported to require liquidation rather than in-kind transfers to move out. |

Once plan assets exceed $250,000, you must file Form 5500-EZ by July 31 each year. When you close the plan, you file a final 5500-EZ regardless of asset level. The form takes about an hour the first time. After that, it takes 15 minutes a year.

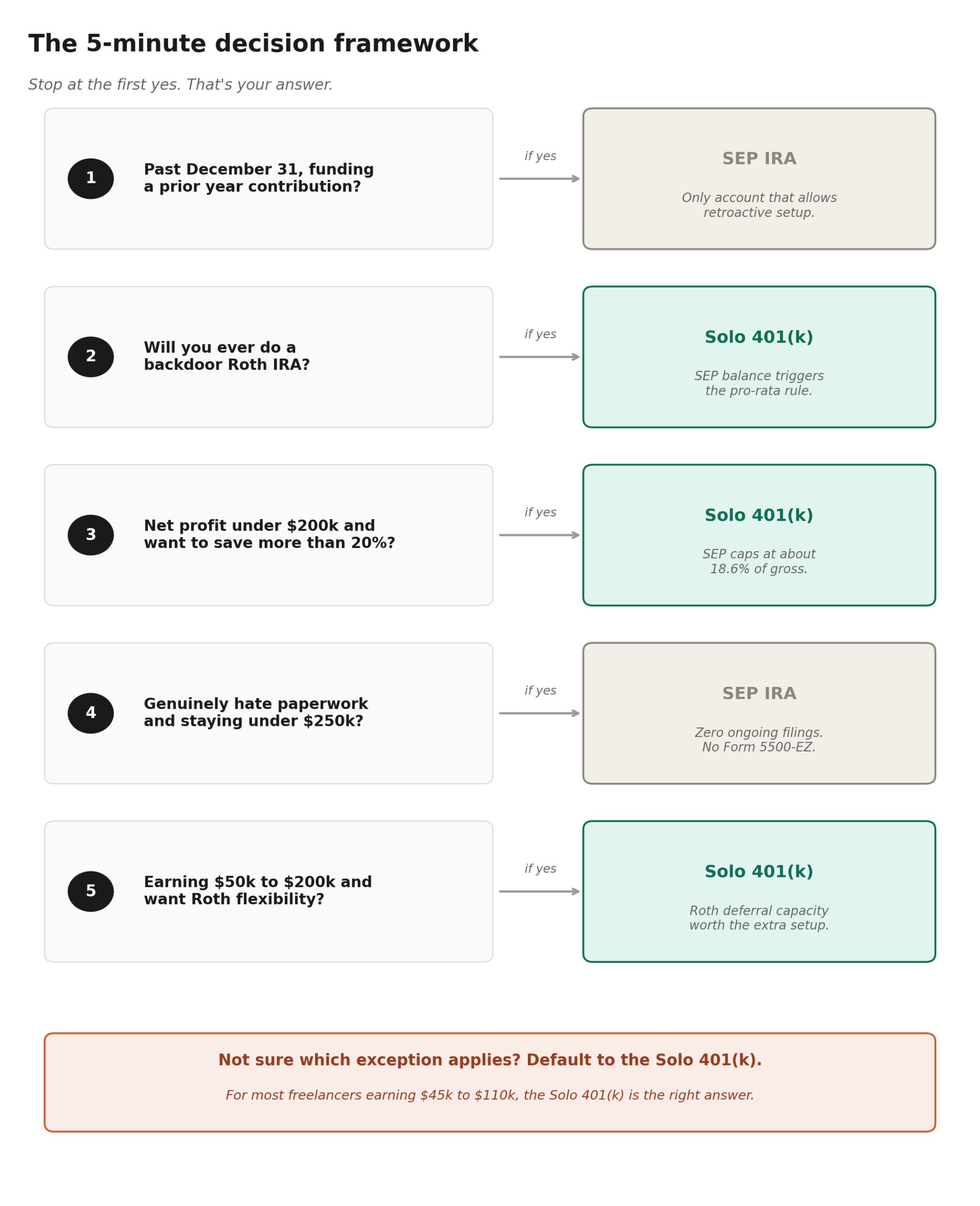

A 5-minute decision framework

Run through these five questions in order. The first “yes” gives you your answer.

For most freelancers in the $45,000 to $110,000 income band, the answer is the Solo 401(k). The exceptions are real but narrow. If you are not sure which exception applies to you, default to the Solo 401(k).

What about an S-corp election?

Electing S-corp status changes the math for both plans because contributions are calculated off W-2 wages, not net profit. The 25% employer contribution becomes a true 25% (no SE tax adjustment), and the employee deferral comes off your W-2 paycheck. A reasonable salary of $60,000 with $40,000 of distributions changes what each account can hold. Whether to elect S-corp status is its own decision and depends on how much you make and what state you live in. We walk through the math in our S-corp vs LLC vs sole prop comparison.

The 2026 Freelancer Retirement Worksheet

If you want the exact contribution numbers for your income, the worksheet takes your Schedule C net profit and walks through the SE tax adjustment, the 20% effective employer rate, and the $24,500 employee deferral side-by-side. You get a clean PDF you can hand to your CPA or use to size your contributions before year-end. Free, no upsell, no spam.

Frequently Asked Questions

Can I have both a Solo 401(k) and a SEP IRA?

Technically yes, but the combined contribution limit across both accounts is still $72,000 for 2026, so there is no advantage to running both. If you opened a SEP IRA in an earlier year and want to switch, you can roll the SEP balance into a Solo 401(k) at a custodian that accepts rollovers (Fidelity and Schwab both do). This avoids the pro-rata rule problem that a SEP IRA creates for backdoor Roth conversions.

What is the deadline to open a Solo 401(k) for 2026?

December 31, 2026. The plan must be established by midnight on the last day of the tax year you want to contribute for. You can fund employer contributions up to your tax filing deadline including extensions (October 15, 2027 if you extend), but the plan document itself must exist by December 31. Miss that deadline and your only option for 2026 is a SEP IRA, which you can open as late as your filing deadline.

Do I need an EIN to open either account?

You need an EIN for a Solo 401(k). It is non-negotiable. Sole proprietors can technically open a SEP IRA with a Social Security Number, though most custodians now ask for an EIN anyway. EINs are free at IRS.gov and take about 10 minutes online. There is no reason not to have one if you are running a business.

Can I contribute as both employee and employer to a Solo 401(k) on the same income?

Yes, and that is the whole point of the plan. The $24,500 employee deferral is separate from the employer profit-sharing contribution, which is up to 25% of your adjusted net earnings (effectively about 20% of net Schedule C profit for sole proprietors). At $75,000 of net profit you can contribute around $24,500 as the employee and around $13,939 as the employer, for a total of $38,439.

Is a Solo 401(k) worth the paperwork if I only have $20,000 to contribute?

Most of the time, yes. The only ongoing paperwork is Form 5500-EZ, which is required when plan assets exceed $250,000. If your balance is $20,000, you have zero filing requirements at the federal level. Setup is a one-time 45 to 90 minutes. The Roth flexibility, the higher contribution ceiling, and the absence of pro-rata rule problems outweigh the minor extra setup time in most cases.

Can I switch from a SEP IRA to a Solo 401(k) mid-year?

You can open a Solo 401(k) at any point before December 31. If you have already made SEP IRA contributions for 2026, those count toward the combined $72,000 limit. The cleanest move is to stop SEP contributions, open the Solo 401(k), make this year’s contributions to it, and then roll the old SEP balance into the Solo 401(k) at year-end or the following year. Confirm with your Solo 401(k) custodian that they accept incoming SEP rollovers before you start.

Does a SEP IRA reduce my self-employment tax?

No. SEP IRA and Solo 401(k) contributions reduce your federal and state income tax, but not the 15.3% self-employment tax. SE tax is calculated on net earnings before retirement contributions. This is true for both accounts. If lowering SE tax is your goal, the only reliable lever is an S-corp election that lets you take part of your income as distributions rather than wages.

What happens to my Solo 401(k) if I hire an employee?

The “solo” in Solo 401(k) is literal. If you hire a non-spouse W-2 employee who works more than 1,000 hours in a year, your plan no longer qualifies. SECURE 2.0 introduced an exclusion for long-term part-time employees who work under 500 hours over two consecutive years, which helps. If you cross the threshold, you either upgrade to a full 401(k) plan with the associated compliance, or you terminate the Solo 401(k). Plan ahead if you are thinking about hiring.

For more on structuring your business before you hire, see our Sole Proprietorship vs LLC vs S-Corp guide and our breakdown of freelancer-friendly business bank accounts.

One thing to do this week

Pull your year-to-date net profit from your bookkeeping. If you are tracking toward $50,000 or more in 2026 and you do not have a retirement plan yet, open a Solo 401(k) at Fidelity, Schwab, or E*TRADE in the next seven days. Setup is under 90 minutes. The contribution deadline for employee deferrals at most custodians requires you to make a salary deferral election by December 31, which means waiting until late December leaves you with a thin window. Open it now and you have eight months to fund it.

Tax laws change. The IRS releases new contribution limits each November for the following year. The numbers above are accurate as of May 2026 based on IRS Notice 2025-67. Verify current limits at IRS.gov before making contributions. This article is informational only and is not tax or legal advice. For decisions involving your specific situation, consult a CPA or enrolled agent.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.