Side income taxes with a full-time job catch people off guard for one reason: your day job withholds tax on your salary. That’s it. A $70,000 W-2 plus an $18,000 side gig can leave you owing about $5,500 in April that nobody pulled from a paycheck. Here’s the math, and three ways to stop it ambushing you.

It’s early April. You’ve just finished your return. You expected a small refund, the way you got one every year you were a W-2 employee. Instead the software says you owe $5,500, and you have no clue where it came from. Your employer withheld tax from every single paycheck. So what gives?

The side income gives. You did $18,000 of freelance design work on top of your salary, and not one cent of tax came out of any of it. That money shows up on a 1099-NEC (or a 1099-K if a platform like PayPal or Stripe paid you), and a 1099 has no withholding attached. Your W-2 covers your salary. It never touched the side gig.

Most side hustle tax content treats you like a full-time freelancer with no job, or pretends the job is the whole story. You’re neither. You’re one tax return with two income streams that feed into each other, and that overlap is where the money hides. This guide handles the W-2 plus 1099 math as one problem, because that’s exactly how the IRS sees it when you file. That is what makes side income taxes with a full-time job their own distinct problem.

Why your W-2 withholding does not cover side income taxes with a full-time job

Withholding pays one specific bill: the wages on that W-2. Your employer estimates the tax on your salary, takes it out across the year, and sends it to the IRS under your Social Security number. It works because your employer can see your salary coming.

Your freelance income is invisible to that system. No client withholds anything. The $18,000 lands in your account in full, and the whole tax bill is on you. That bill comes in two parts, and the first one blindsides almost everybody.

- Self-employment tax. This is the 15.3% that funds Social Security and Medicare (12.4% plus 2.9%), reported on Schedule SE. As a W-2 employee you paid half and your employer paid the other half. On your freelance profit you pay both halves yourself. It applies to 92.35% of your net profit, on top of income tax, and it starts at the very first dollar.

- Income tax. Your freelance profit stacks on top of your salary and gets taxed at your top marginal rate, not from zero. If your salary already puts you in the 22% federal bracket, your side income is taxed starting at 22%.

The $70k salary plus $18k side gig example, line by line

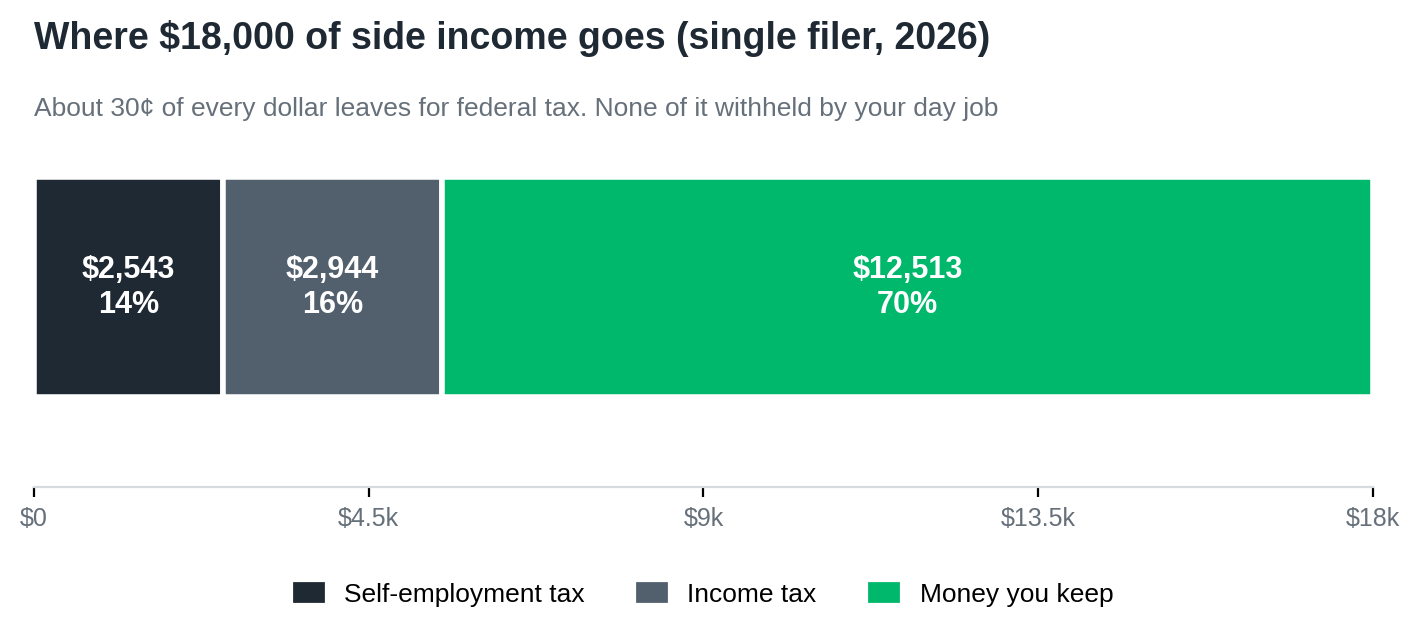

Take a freelance designer with a $70,000 W-2 job and $18,000 of net freelance profit after expenses, filing single for 2026. Here’s what the side income actually costs.

- Self-employment tax: $18,000 × 92.35% = $16,623, taxed at 15.3% = about $2,543. Half of that ($1,272) comes back as an income tax deduction.

- QBI deduction: the 20% qualified business income deduction (Section 199A, made permanent by the One Big Beautiful Bill Act in July 2025) knocks roughly $3,300 off the taxable amount.

- Income tax: after the half-SE and QBI deductions, about $13,400 gets taxed at the 22% marginal rate = roughly $2,944.

Total federal tax on the side income: about $5,500. That’s roughly 30 cents on every dollar you earned freelancing, and your salary withholding paid none of it. This is the gap. Everything below is about closing it before April. That gap is the heart of side income taxes with a full-time job.

Want the line-by-line on how profit gets calculated in the first place? The Schedule C walkthrough covers it with real numbers, and the deductions freelancers miss guide shows what brings that $18,000 of revenue down to taxable profit.

When does side income mean you have to pay quarterly taxes?

The trigger is simple. The IRS expects quarterly estimated payments if you’ll owe $1,000 or more when you file, after subtracting your withholding and credits. Owe less than $1,000 after withholding and you can skip the quarterlies and just pay at filing. This is the question at the center of side income taxes with a full-time job.

Here’s the part people miss. Your day-job withholding counts toward that test. If your employer withholds generously, your salary withholding alone might cover the safe harbor, and your side income rides along penalty-free even though no tax was withheld on it directly.

The safe harbor rule, and why it is your real deadline

You avoid an underpayment penalty if your total payments (withholding plus any estimates) hit one of these, per the IRS estimated tax rules:

- 90% of your current-year tax, or

- 100% of last year’s total tax (110% if your prior-year adjusted gross income was over $150,000, or $75,000 if married filing separately).

So the question isn’t “do I have side income.” It’s “will my W-2 withholding alone reach one of those numbers.” Pull last year’s Form 1040, find your total tax on line 24, and compare it to what your employer is on track to withhold this year. Your latest pay stub shows year-to-date federal withholding. If your projected withholding already clears 100% (or 110%) of last year’s total tax, you’re inside the safe harbor and you don’t need to make a single quarterly payment, no matter how much the side gig made.

If it falls short, the shortfall is what the side income created, and you have two ways to cover it. Quarterly payments are one. The other is usually better, and almost nobody with a day job uses it. Handling side income taxes with a full-time job comes down to this choice.

The quarterly deadlines, if you go that route, are April 15, June 15, September 15, and January 15. The quarterly estimated taxes guide walks through paying them through IRS Direct Pay.

How your day-job salary changes your self-employment tax

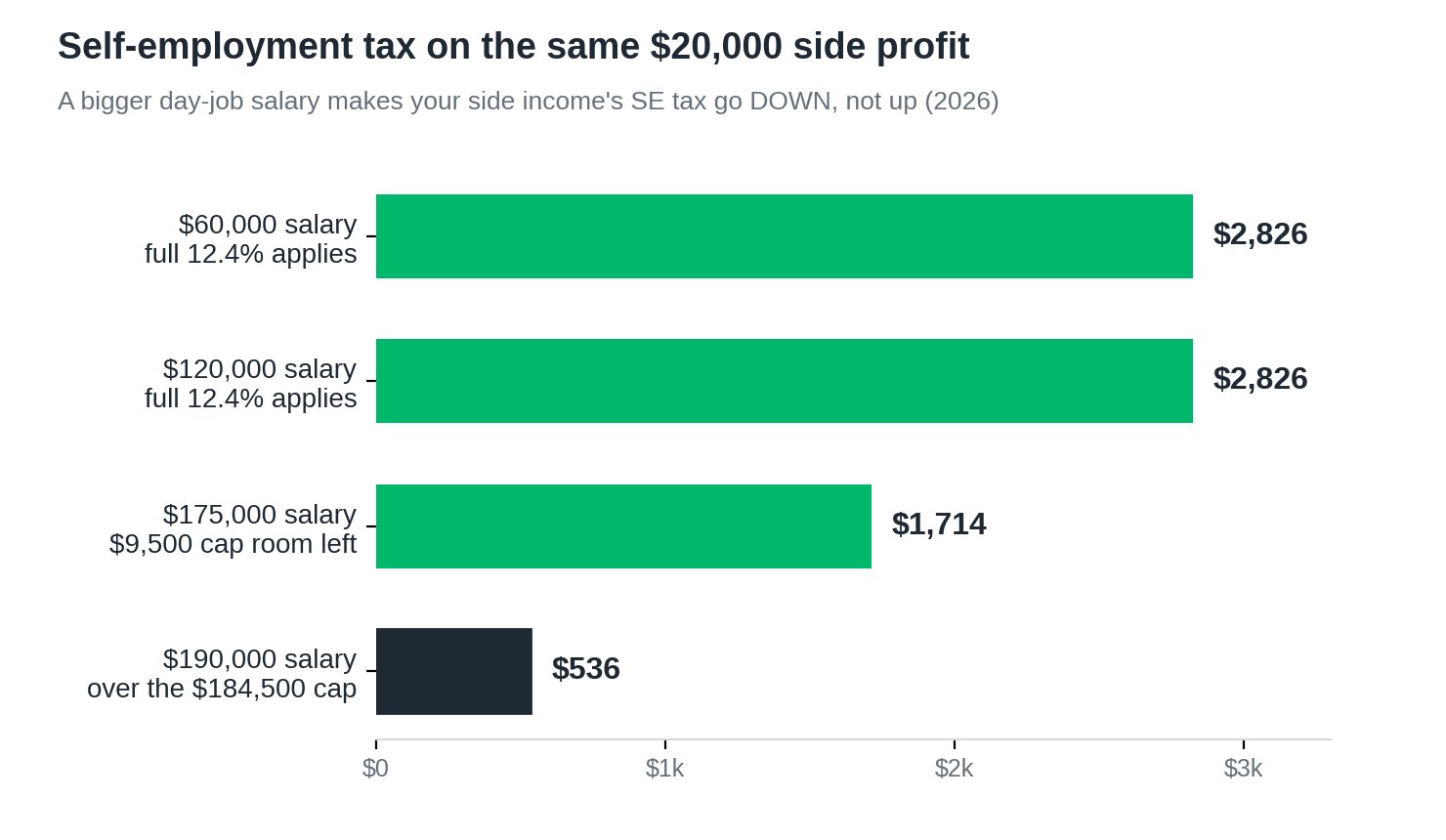

This is the part no side hustle article shows you, and it can swing your bill by thousands. The 12.4% Social Security half of self-employment tax only applies up to the annual wage base, which is $184,500 for 2026 ($176,100 in 2025). Your W-2 wages count toward that cap first. It is the detail that makes side income taxes with a full-time job different from full-time freelancing.

On Schedule SE you subtract your W-2 Social Security wages from the wage base before applying the 12.4%. The higher your salary, the less room is left, and the more of your side income escapes the Social Security portion entirely. Once your salary alone hits $184,500, your freelance profit owes only the 2.9% Medicare portion. So a bigger day-job salary makes your side income’s self-employment tax go down.

What $20,000 of side profit costs in SE tax, by day-job salary (2026)

| Day-job salary | SE tax on $20,000 of side profit (2026) |

|---|---|

| $60,000 | ~$2,826 |

| $190,000 | ~$536 |

Read the bottom two rows again. A freelancer with a $190,000 salary pays about $536 in self-employment tax on the same $20,000 that costs a $60,000 earner $2,826. The income tax on that side profit is higher for the high earner, because they’re in a higher bracket. The self-employment tax runs the opposite way. You need both halves to see your real number.

One catch if you have two W-2 jobs, or switched jobs mid-year: each employer caps Social Security withholding independently, so you can over-pay. You claim the excess back as a credit on Form 1040, line 11 of Schedule 3. The IRS won’t chase you for it. You have to ask.

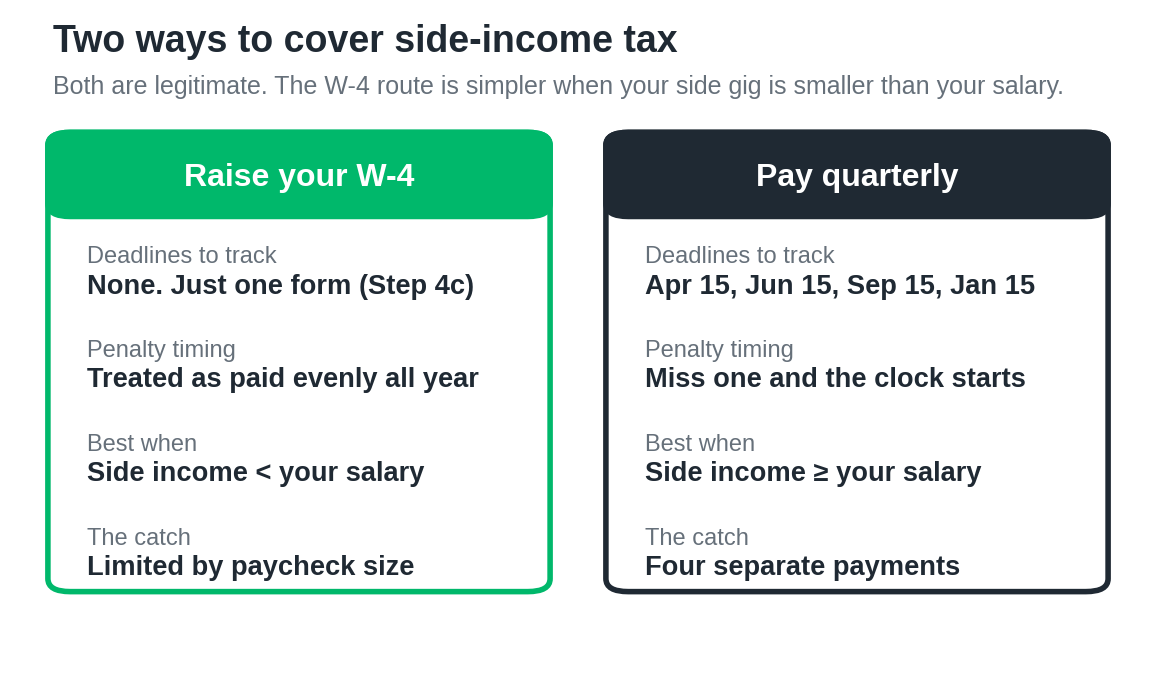

Adjust your W-4 instead of paying quarterly

Here’s the move almost nobody with a day job uses. You can cover your entire side-income tax bill through your W-2 withholding and skip quarterly payments completely. The IRS treats withholding as if it were paid evenly across the whole year, no matter when it actually left your paycheck. This is the Form 2210 default rule, and it’s the thing that makes this work.

Quarterly payments are dated. Miss the timing on one and the penalty clock starts for that quarter, even if you catch up later. Withholding has no such problem. Money withheld in December counts the same as money withheld in March. You could earn a lump of freelance income in November, bump your December paychecks to cover the tax, and the IRS treats it as though you paid steadily since January.

How to size the extra withholding

You do it on Form W-4, Step 4(c), the line labeled “Extra withholding.” Whatever dollar amount you put there gets taken from every paycheck on top of your normal withholding. The steps:

- Estimate the federal tax on your side income (use the 30% rule of thumb below if you’re in the 22% bracket, then refine).

- Divide that figure by the number of paychecks left in the year.

- Put that per-paycheck amount in Step 4(c) and hand the new W-4 to your employer’s payroll team.

- Recheck in January and reset the figure for the new year.

For the designer owing about $5,500 on side income, with 24 paychecks left, that’s roughly $230 per paycheck into Step 4(c). No IRS portal, no four deadlines, no separate payments to remember, no penalty timing to sweat. One form. If you’d rather not do the arithmetic yourself, the IRS Tax Withholding Estimator at irs.gov runs the per-paycheck number for you.

This breaks in one situation: when your side income is large compared to your salary. There’s only so much your employer can withhold from a $50,000 salary, and if your freelance profit is $80,000, you can’t squeeze enough out of the paycheck to cover it. At that point you need quarterly payments, or a mix of both. For most people earning $45,000 to $110,000 with a side gig under their salary, the W-4 route covers the whole thing.

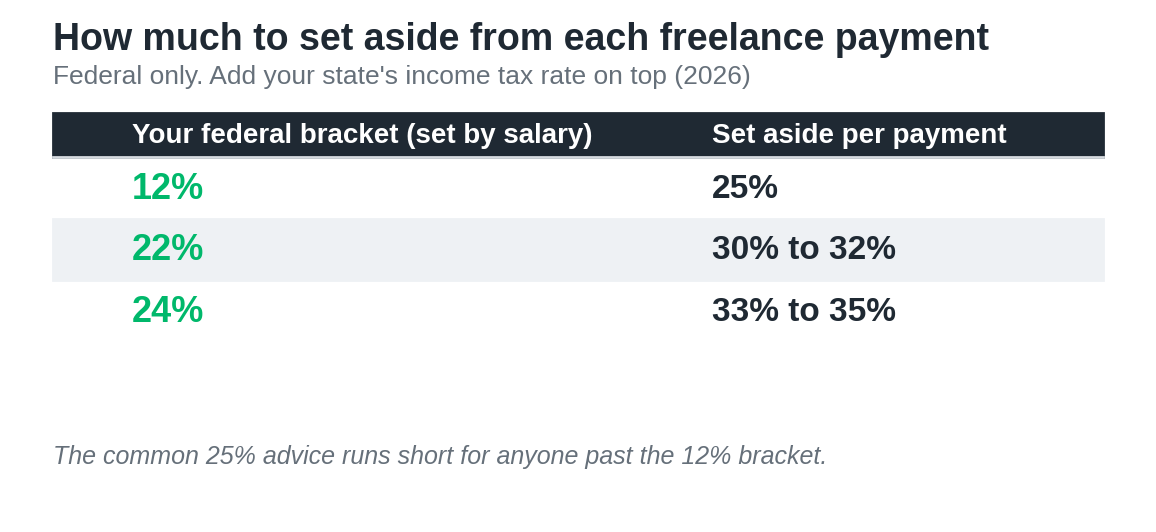

How much should you set aside when you cannot predict the side income?

Feast and famine makes a flat dollar plan useless. You don’t know if the side gig will bring in $4,000 or $25,000 this year. So set aside a percentage of each freelance payment instead, the moment it lands, and the unpredictability stops mattering.

The right percentage depends on the federal bracket your salary already put you in, because your side income stacks on top of it. These figures assume your salary is under the $184,500 Social Security cap, which covers nearly everyone in the $45,000 to $110,000 range.

| Federal bracket your salary already put you in | Set aside for federal tax (per freelance payment) |

|---|---|

| 12% bracket | ~25% |

| 22% bracket | 30%–32% |

| 24% bracket | 33%–35% |

Open a separate savings account and move the percentage over every time a client pays you. The freelancers on r/freelance who never get caught short all say the same thing: the money has to leave the spending account immediately, or it gets spent. The set-aside guide goes deeper on picking your number, and tracking expenses properly lowers it by shrinking your taxable profit.

The 25% figure most blogs quote is a full-time-freelancer number, and even there it runs light. With a salary already filling your lower brackets, 25% will leave you short in April if you’re in the 22% bracket. Run the percentage against your bracket, not against some round number you read somewhere. The rest of our freelancer tax and money guides cover the situations this one skips, from full-time freelancing to retirement accounts.

Should you set up an S-corp for side income?

Short answer for almost everyone reading this: not yet, and the W-2 job is the reason. The S-corp pitch is that you save the 15.3% self-employment tax on the profit you take as distributions rather than salary. With a day job, much of that saving is already gone before you start. For side income taxes with a full-time job, the S-corp math rarely pays off.

Look back at the SE tax table. The big chunk of self-employment tax is the 12.4% Social Security portion, and your salary is already eating into the $184,500 cap. If your salary is $150,000, you have $34,500 of Social Security room left, and an S-corp can only save you the 12.4% on whatever side profit fits inside it. If your salary is over $184,500, your side income owes no Social Security tax at all, so the S-corp saves you nothing on that front. You’re left chasing the 2.9% Medicare portion, which rarely justifies the overhead.

And the overhead is real. An S-corp means running payroll for yourself with a “reasonable salary,” filing a separate Form 1120-S return, paying for payroll software or a service ($500 to $1,500 a year is common), and state filing fees. Those costs are fixed whether your side profit is $20,000 or $200,000. For a side gig clearing $20,000, they eat the entire benefit.

There’s a QBI cost too. Money you pay yourself as S-corp salary isn’t qualified business income, so it shrinks the 20% QBI deduction you’d otherwise get on the full profit as a sole proprietor. For a side hustler, that often cancels what little SE tax saving was left.

The honest threshold: the S-corp election starts to make sense when your side profit is large (commonly cited around $80,000 and up of net profit) and your salary still leaves meaningful Social Security room. Below that, with a W-2 job, it’s paperwork that costs you money. The entity comparison runs the full break-even, and our methodology explains how we test these claims.

The mistake that produces the April surprise

The recurring theme across r/tax and r/freelance threads on side income is one belief, stated a dozen different ways: “I have a job that withholds tax, so I figured I was covered.” You were covered on your salary. The side income was always a separate bill with no payments going against it. The broader version of this trap, and how to defuse it across a full freelance year, sits in the guide on how to avoid a tax liability shock. Almost everyone who gets burned by side income taxes with a full-time job believed exactly this.

The second version of the mistake is trusting last year’s refund. You got a refund every year as a pure W-2 employee, so a refund feels normal. The first year you add side income, that refund can flip to a four-figure bill while nothing about your salary changed. A refund last year tells you nothing about this year once a 1099 enters the picture.

The third is forgetting state tax. The numbers above are federal. If you’re in California, Illinois, or another state with income tax, your side income owes state tax too, and your state has its own estimated payment rules. Florida and Texas freelancers skip this. Most others don’t. The state-by-state guide has your rate.

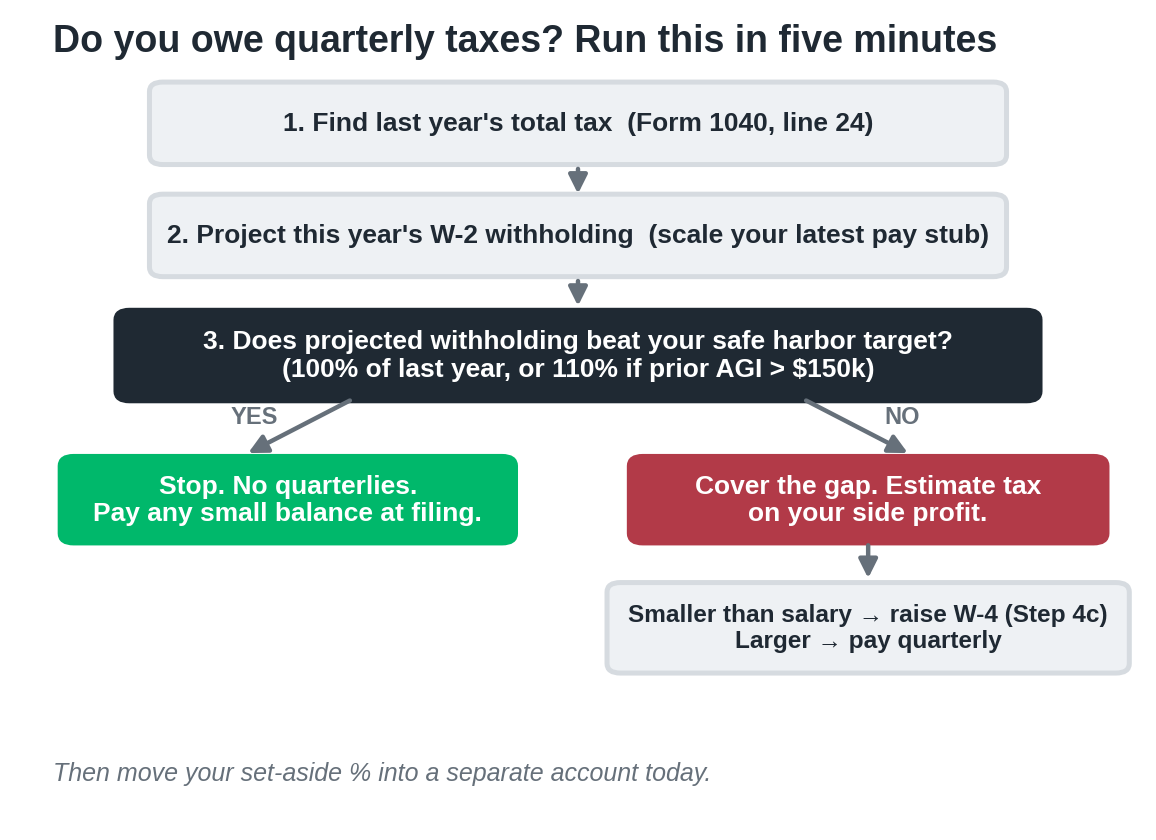

Run this in five minutes

You can settle whether you owe quarterlies, and pick your fix, before your coffee goes cold.

- Find last year’s total tax. Form 1040, line 24. Note whether your prior-year AGI was over $150,000 (if so, your target is 110% of that figure, otherwise 100%).

- Project this year’s withholding. Take year-to-date federal withholding from your latest pay stub and scale it to a full year.

- Compare. If projected withholding already beats your safe harbor target, stop. You owe no quarterlies this year. Pay any small balance at filing.

- If it falls short, estimate tax on your side profit (set-aside table above) and decide: bump Step 4(c) on your W-4 to cover it through payroll, or make quarterly payments. If your side profit is smaller than your salary, the W-4 route is simpler.

- Move your set-aside percentage into a separate account today, so the cash is there when the bill comes.

Frequently Asked Questions

Do I have to pay quarterly taxes if I have a full-time job and freelance on the side?

Only if your withholding won’t cover you. The test is whether you’ll owe $1,000 or more at filing after withholding and credits. Your W-2 withholding counts toward the safe harbor, so if it already reaches 100% of last year’s total tax (110% if your prior-year AGI was over $150,000), you can skip quarterlies entirely. If it falls short, you cover the gap with estimated payments or by raising your W-4 withholding. That is the short version of side income taxes with a full-time job.

Can I just increase my W-4 withholding instead of making estimated payments?

Yes, and it’s usually simpler. The IRS treats withholding as paid evenly across the year no matter when it was taken, so you dodge the quarterly timing penalties. Use Step 4(c) on Form W-4 to add a flat extra dollar amount per paycheck. The limit is practical: you can only withhold so much from your salary, so this works best when your side income is smaller than your wages.

How much should I set aside for taxes on freelance income if I also have a salary?

Base it on the federal bracket your salary already put you in, because side income stacks on top. In the 22% bracket, set aside 30% to 32% of each freelance payment for federal tax. In the 24% bracket, set aside 33% to 35%. Add your state’s income tax rate on top. The common 25% advice runs short for anyone past the 12% bracket.

Why do I owe self-employment tax when my job already takes out Social Security?

Your job withholds Social Security and Medicare on your salary only. Your freelance profit is separate income with no employer, so you owe both the employee and employer halves on it: 15.3% total, reported on Schedule SE. The one piece of good news is that your W-2 wages count toward the annual Social Security cap ($184,500 for 2026), which can reduce or remove the 12.4% Social Security portion on your side income if your salary is high.

Does my freelance income push my whole salary into a higher tax bracket?

No. Brackets are marginal, so only the income that lands in a higher band is taxed at the higher rate. Your salary keeps its existing treatment, and the side income is taxed starting at whatever bracket your salary ended in. If your salary leaves you in the 22% bracket, your first dollars of side profit are taxed at 22%, not the whole return.

Should I form an LLC or S-corp for a side hustle while employed?

An LLC gives you liability separation but changes nothing about your taxes by default; a single-member LLC is still taxed as a sole proprietor. An S-corp election can cut self-employment tax, but with a W-2 job the saving shrinks, because your salary already fills part of the Social Security wage base. For most side gigs under about $80,000 of net profit, the S-corp’s payroll and filing costs outweigh the benefit. Wait until the profit is large and steady.

What happens if I missed a quarterly estimated payment?

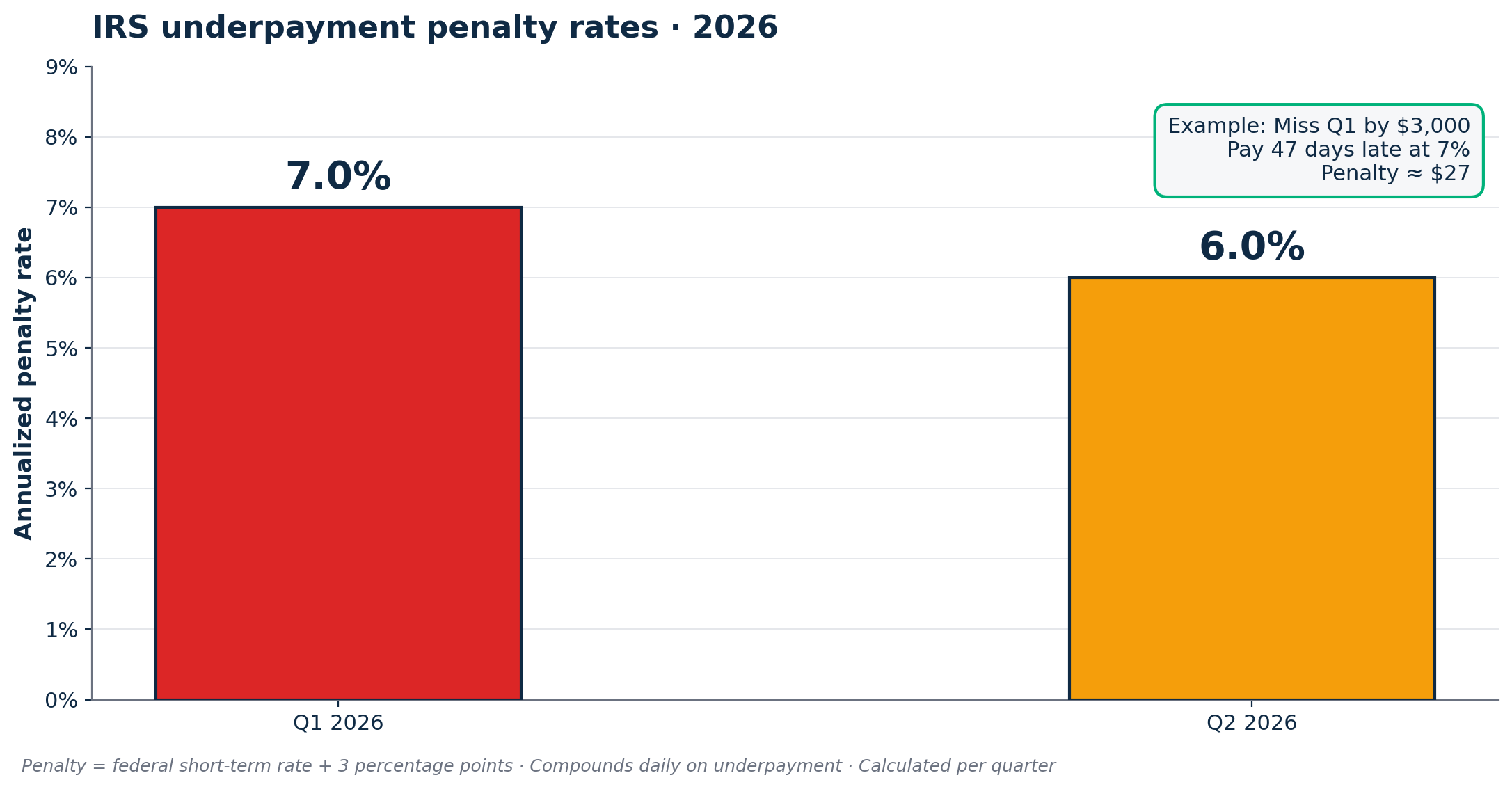

You owe an underpayment penalty calculated as interest on the shortfall, charged per quarter until you catch up. The IRS dropped the individual underpayment rate to 6% for the second quarter of 2026, down from 7% earlier in the year, and it resets every quarter. You can shrink or erase the penalty for earlier quarters by raising your W-4 withholding for the rest of the year, since withholding is treated as paid evenly. Form 2210 calculates the final figure.

Tax laws change and the figures here reflect 2025 and 2026 rules, including the One Big Beautiful Bill Act signed July 4, 2025. Verify current numbers at IRS.gov and confirm your own situation with a CPA. This is informational and not tax or legal advice.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.