California adds at least four bills generic tax guides skip: an $800 LLC tax, a front-loaded estimated schedule, a city registration most freelancers miss, and a deduction the state quietly takes back. Here is what each one of these California freelancer taxes costs you.

You formed an LLC last spring because a client said it looked more professional. You made $58,000, paid your federal taxes in April, and figured you had it handled. Then in October a letter from the California Franchise Tax Board showed up: $800 owed for the year, plus a penalty for paying it late. Nobody told you that bill existed.

California freelancer taxes have more moving parts than any other state’s, and California has more freelancers than anywhere else. You can learn the federal stuff once and reuse it anywhere, and our library of freelancer tax and finance guides covers that federal side. The California layer is where people get caught, because the traps are state-specific and most national guides never mention them.

This guide covers the bills that actually blindside California freelancers: the $800 franchise tax, the state income brackets, the estimated payment schedule that does not match the IRS, the city business taxes in San Francisco, Los Angeles, and Oakland, and the federal deduction California refuses to honor. Figures here are for the 2025 tax year (filed in 2026) and current 2026 rules. Tax law changes, so verify anything that affects a payment at ftb.ca.gov before you act.

The $800 that catches new California LLCs every year

File a Schedule C as a sole proprietor and you do not owe this. That matters, because the moment you form an LLC to look legitimate, you have signed up for an $800 minimum franchise tax every single year, whether you make money or not.

Every LLC, limited partnership, and corporation registered to do business in California owes the $800 annual tax. The Franchise Tax Board collects it even if your LLC earned nothing, sat dormant, or ran at a loss. The only way to stop it is to formally dissolve the entity with both the FTB and the Secretary of State.

Here is the part that trips people up. California used to waive the $800 for an LLC’s first year under Assembly Bill 85, but that waiver only applied to entities formed between January 1, 2021 and December 31, 2023. It expired. Any LLC formed in 2024 or later owes the full $800 from year one. Plenty of blog posts still claim the exemption is active. It is not, and the FTB’s own LLC page confirms it.

You pay the $800 with Form 3522 by the 15th day of the fourth month of your tax year, which is April 15 for a calendar-year LLC. Your LLC also files Form 568, the LLC Return of Income. Form a new LLC late in the year and you can get hit twice in quick succession: once shortly after formation, then again the following April. Corporations and S corporations still get a true first-year exemption. LLCs do not.

When the $800 turns into a lot more

Cross $250,000 in California gross receipts and the $800 stops being the whole story. California adds a separate LLC fee on top, based on total income, not profit. You estimate and pay it with Form 3536 by the 15th day of the sixth month (June 15 for calendar-year filers).

- $250,000 to $499,999: $900 fee, on top of the $800.

- $500,000 to $999,999: $2,500 fee.

- $1,000,000 to $4,999,999: $6,000 fee.

- $5,000,000 and up: $11,790 fee.

The fee runs on gross receipts, so a freelancer billing $300,000 a year but netting $120,000 still owes the $900 fee plus the $800 tax. That is $1,700 in state entity costs before a dollar of income tax. Most freelancers reading this earn under $250,000 and only face the flat $800, but the fee is worth knowing before a good year pushes you over the line.

Before you decide an LLC is worth it, read our breakdown of sole proprietorship versus LLC versus S-corp for freelancers. The table below shows what the LLC actually adds in California.

| California cost | Sole proprietor | Single-member LLC |

|---|---|---|

| Annual minimum franchise tax | $0 | $800 every year, even at a loss |

| First-year relief | Not applicable | None since AB 85 expired at the end of 2023 |

| LLC fee on income over $250,000 | Not applicable | $900 to $11,790 by gross receipts |

| State forms to file | Schedule CA (540) with your return | Form 568, Form 3522, plus Form 3536 if over $250,000 |

| Does the $800 reduce your income tax? | Not applicable | No, it sits on top of income tax |

California freelancer taxes: income brackets for 2025

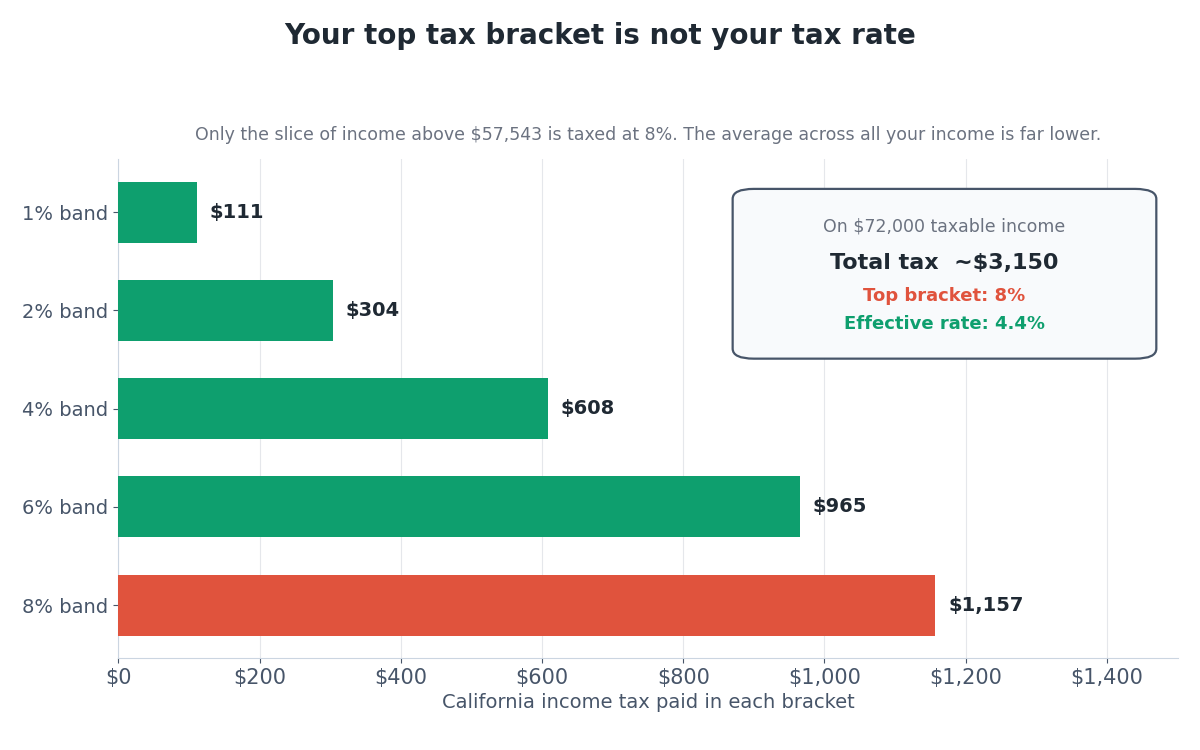

California taxes your net business profit as ordinary income on top of your federal bill. The state uses nine brackets running from 1% to 12.3%, with an extra 1% surcharge on income over $1 million that pushes the true top rate to 13.3%. Here are the 2025 brackets for single filers, used on returns filed in 2026.

| Rate | Single / married filing separately taxable income |

|---|---|

| 1% | $0 to $11,079 |

| 2% | $11,080 to $26,264 |

| 4% | $26,265 to $41,452 |

| 6% | $41,453 to $57,542 |

| 8% | $57,543 to $72,724 |

| 9.3% | $72,725 to $371,479 |

| 10.3% | $371,480 to $445,771 |

| 11.3% | $445,772 to $742,953 |

| 12.3% | $742,954 and up |

Married filing jointly brackets are exactly double the single figures, so California does not impose a marriage penalty in its rate structure. These are marginal rates, which means only the slice of income inside each band gets taxed at that rate.

A single freelancer with about $72,000 in California taxable income pays roughly $3,150 in state income tax, an effective rate near 4.4%, even though the top slice of that income sits in the 8% band. The marginal rate scares people more than the actual bill warrants. What does cost you is the standard deduction.

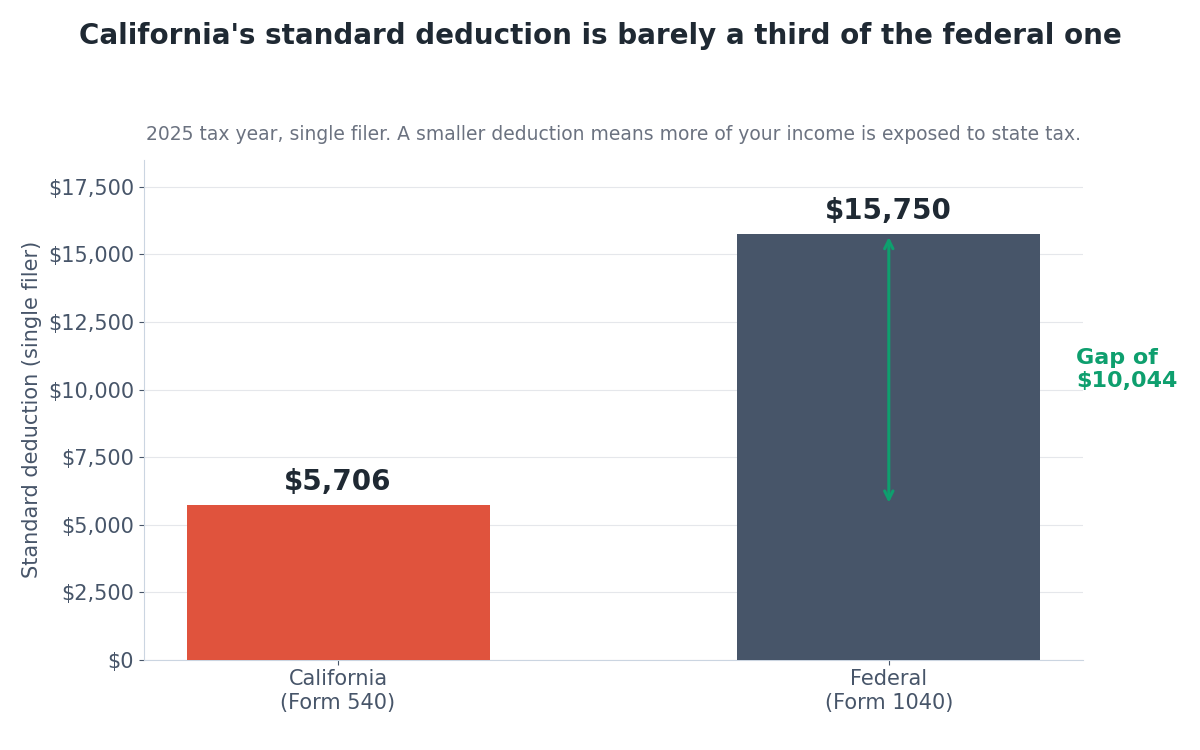

California’s 2025 standard deduction is $5,706 for single filers and $11,412 for married filing jointly. The federal standard deduction for 2025 is $15,750 for a single filer. That gap means more of your income is exposed to California tax than to federal tax, so your state taxable income comes out higher than the federal number you are used to looking at.

One thing California does not have: a separate state self-employment tax. The 15.3% self-employment tax (12.4% Social Security up to an annual wage cap of $176,100 in 2025, plus 2.9% Medicare with no cap) is federal only. To size the full picture, use our guide on how much freelancers should set aside for taxes.

The QBI deduction California refuses to honor

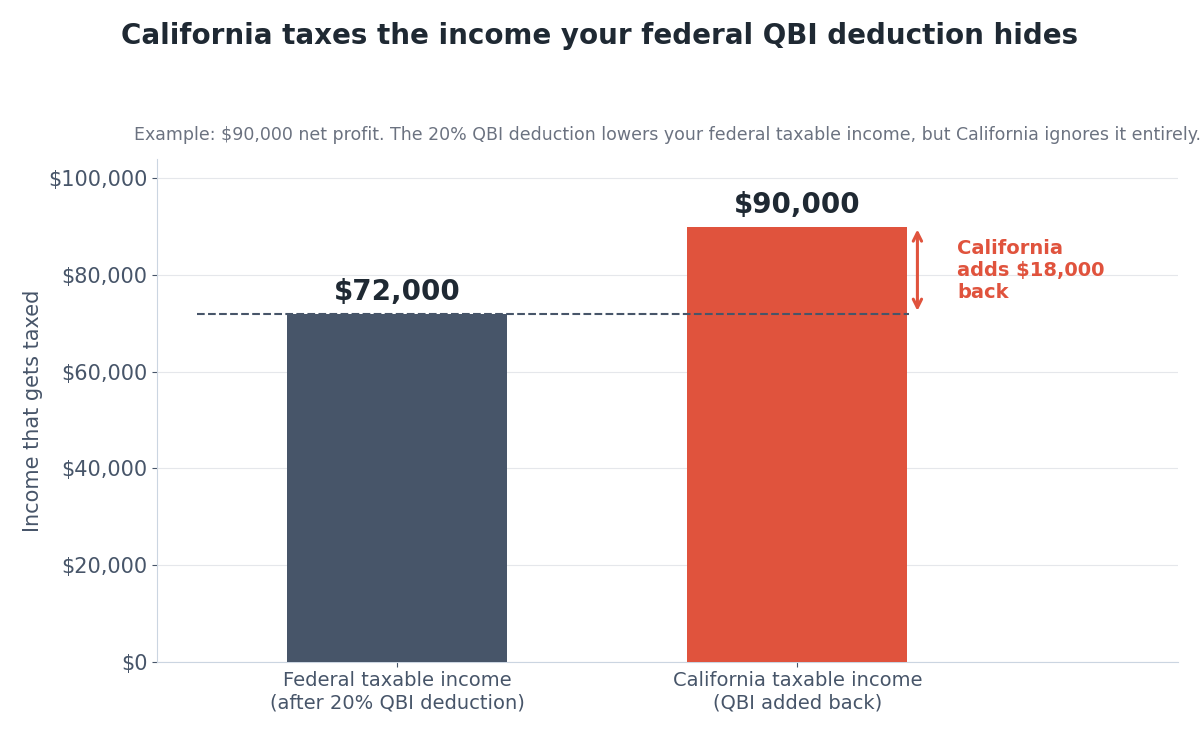

This is the trap almost no California freelancer sees coming, and it is one of the costliest California freelancer taxes surprises. The federal qualified business income deduction (Section 199A) lets eligible self-employed people deduct a chunk of their net profit. The One Big Beautiful Bill Act, signed July 4, 2025, made that deduction permanent at 20% of qualified business income.

California does not conform to Section 199A. It never has. The Franchise Tax Board confirms the state ignores the deduction entirely, and California’s conformity date sits at January 1, 2025, which means it does not pick up the One Big Beautiful Bill Act changes at all.

Here is what that means in dollars. Say you net $90,000 as a freelance developer. On your federal return the QBI deduction can shave roughly $18,000 off your taxable income. California adds every dollar of it back on Schedule CA (540), so the state taxes the full $90,000. This is one of the most common shocks on a first California return, because the federal deduction makes your bottom line look smaller than the state actually sees it.

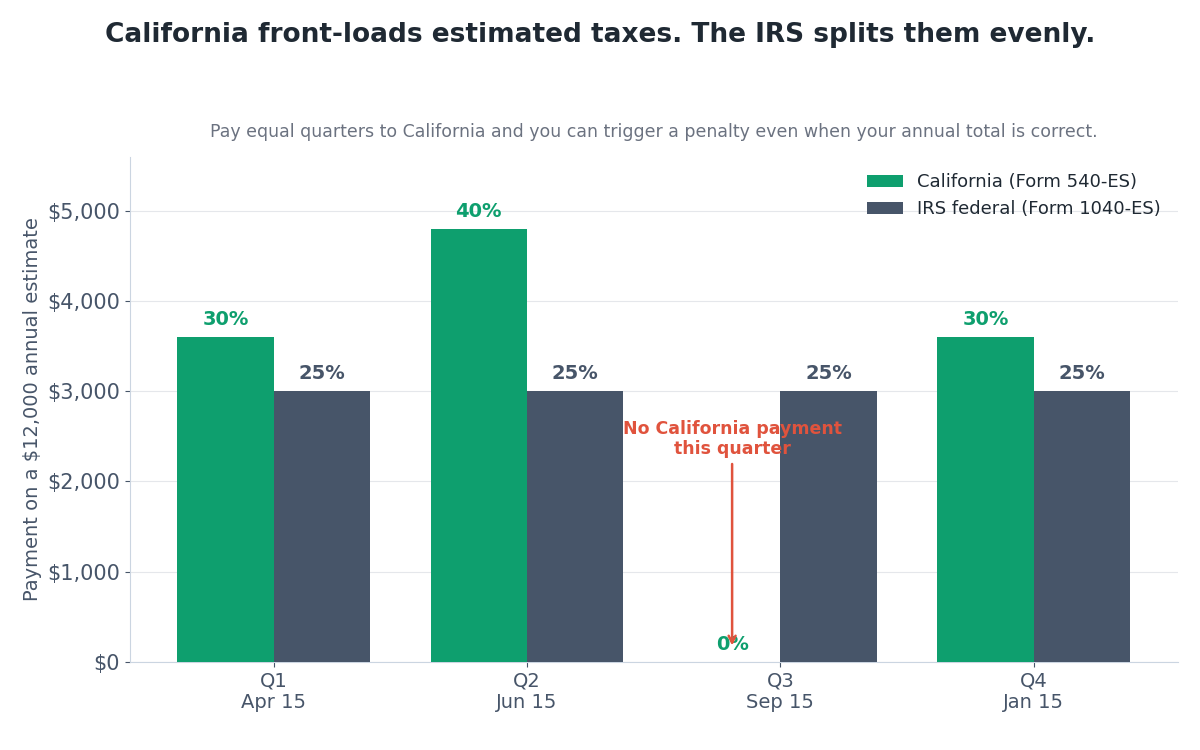

Why your California estimated payments aren’t four equal chunks

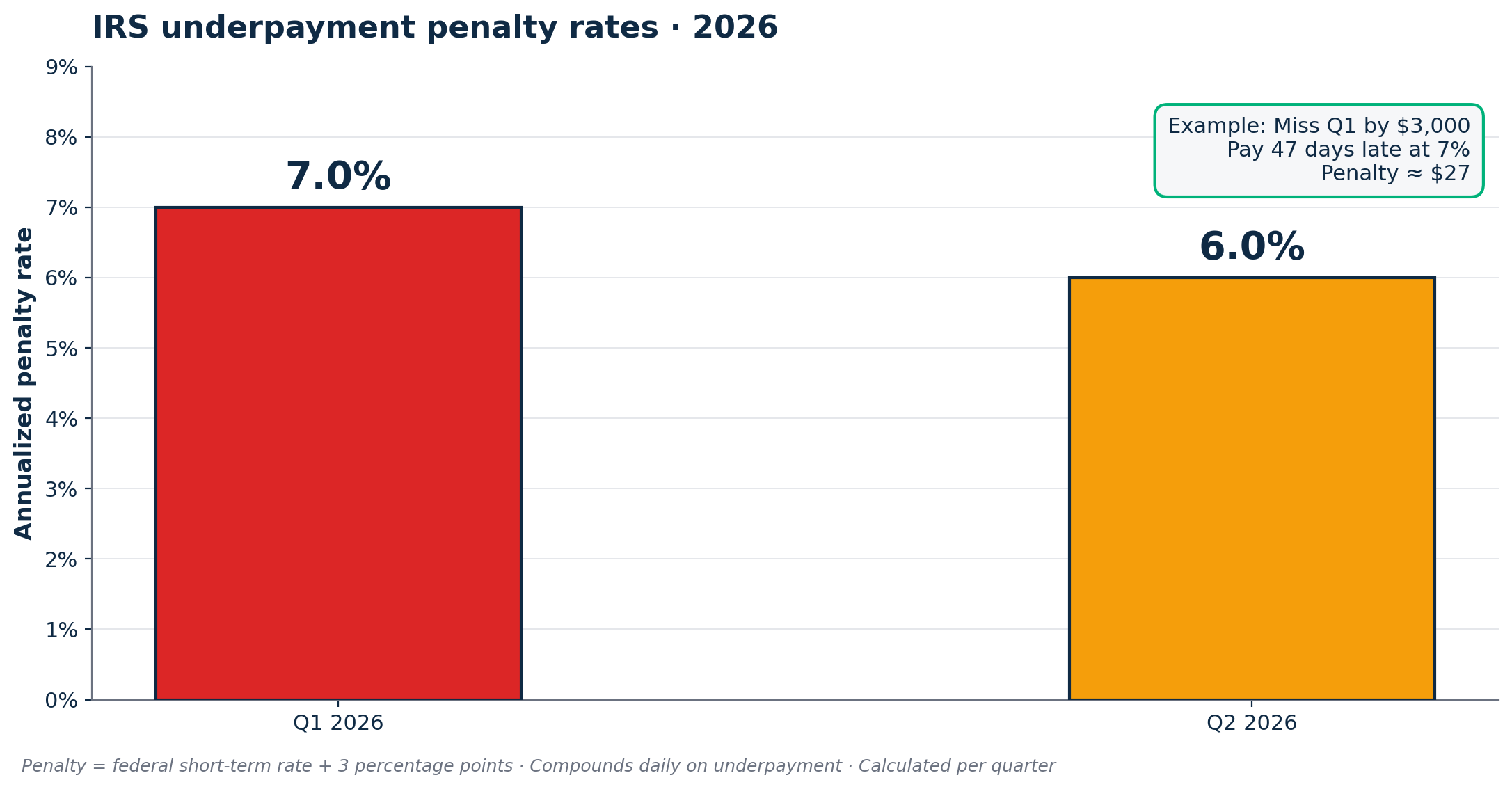

The IRS wants four roughly equal estimated payments, 25% each. California does not. The FTB requires a front-loaded schedule on Form 540-ES: 30% in the first quarter, 40% in the second, 0% in the third, and 30% in the fourth. Pay equal quarters the way you do federally and you can trigger a California underpayment penalty even if your annual total is exactly right, because the FTB checks each period separately.

You owe California estimated payments once you expect to owe more than $500 in state tax after withholding, a lower trigger than the federal $1,000 threshold. If you also hold a W-2 job, the tax withheld from that paycheck reduces what you still owe California, so a smaller side income can stay under the $500 line; our guide on freelancing while employed full-time shows how to run that math. The due dates match the federal calendar (April 15, June 15, September 15, and January 15), but the third payment is zero. Here is the schedule on a $12,000 annual estimate.

| Payment | Due date | Percent of annual estimate | On a $12,000 estimate |

|---|---|---|---|

| 1st | April 15, 2026 | 30% | $3,600 |

| 2nd | June 15, 2026 | 40% | $4,800 |

| 3rd | September 15, 2026 | 0% | $0 |

| 4th | January 15, 2027 | 30% | $3,600 |

The empty third quarter throws people. You are not done for the year, you just have no California payment due that quarter, while your federal payment is still owed in September. If your prior-year California adjusted gross income topped $150,000, you have to pay 110% of last year’s tax to stay inside the safe harbor instead of 100%.

Run your federal numbers alongside this using our walkthrough on filing quarterly estimated taxes as a freelancer, then split the California portion into the 30/40/0/30 pattern so you are not penalized for a payment that arrived in the wrong quarter.

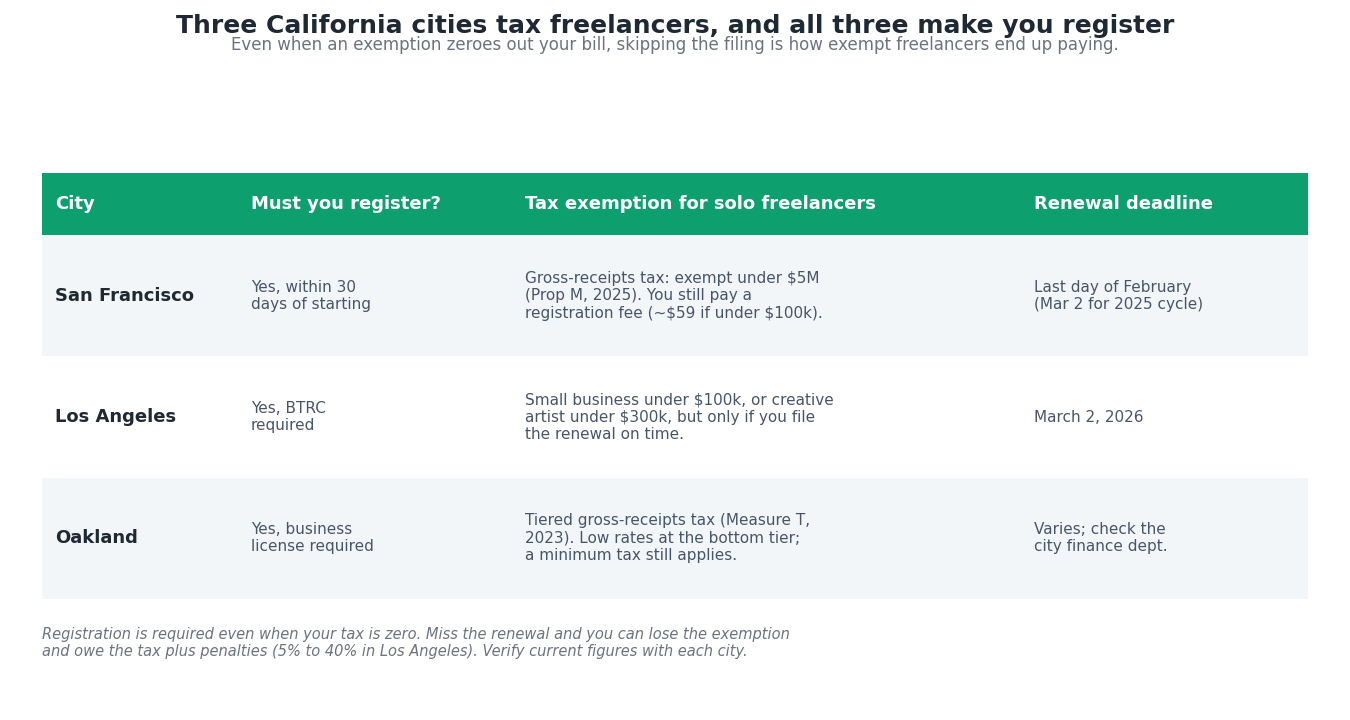

Local business taxes most California freelancers never hear about

California cities run their own business taxes, separate from anything the FTB collects. Three matter most for freelancers: San Francisco, Los Angeles, and Oakland. In all three, the registration requirement applies even when you owe no tax, and missing the filing is how exempt freelancers end up paying anyway.

San Francisco: register even when you owe nothing

San Francisco voters passed Proposition M in November 2024, and it took effect January 1, 2025. It raised the small business exemption for the gross receipts tax from $2.25 million to $5 million. Keep your San Francisco gross receipts under $5 million, which covers essentially every solo freelancer, and you no longer file a gross receipts tax return.

You still have to register your business within 30 days of starting and renew it every year, and you still pay the annual business registration fee. That fee is based on your San Francisco gross receipts. For the 2026-27 registration year it is $55 plus a $4 state fee if your gross receipts are $100,000 or less, and $95 plus $4 from $100,000 to $250,000. New businesses can apply for San Francisco’s First Year Free program, which waives the initial registration fee. The unified renewal deadline for the 2025 cycle was March 2, 2026 (the last day of February, which fell on a weekend). Being exempt from the tax does not mean skipping the form. File on time or you lose your standing and pick up penalties.

Los Angeles: the exemption you lose by not filing

Anyone doing business in the City of Los Angeles must hold a Business Tax Registration Certificate, including self-employed people working from home. Los Angeles taxes gross receipts, not profit, so the tax is calculated on revenue regardless of whether you made money.

Two exemptions usually zero out a freelancer’s bill. The small business exemption applies when your worldwide gross receipts are $100,000 or less. The creative artist exemption applies to qualifying creative work (writers, illustrators, designers, photographers, and similar) up to $300,000 in receipts from those activities. Both require you to file the annual renewal on time. The 2026 renewal deadline is March 2, 2026.

Here is the trap. The exemption is not automatic. Miss the renewal deadline and Los Angeles treats you as delinquent, strips the exemption, and bills you the tax that would otherwise have been zero, plus penalties that climb from 5% to 40% as the year goes on. A freelance copywriter earning $70,000 who forgets the renewal can owe city tax and penalties on revenue that should have cost nothing.

Oakland: a tiered tax since 2023

Oakland requires a business license for anyone operating in the city and taxes gross receipts under a tiered structure created by Measure T, effective January 1, 2023. Business and professional service rates are low at the bottom tier, in the range of $0.50 to a few dollars per $1,000 of gross receipts depending on category, and a minimum tax applies. A separate measure proposing a one-year tax holiday for businesses under $1 million in receipts has been floated for 2027 but is not yet law, so do not plan around it.

Smaller California cities run similar registration rules. If you work from home anywhere in the state, check your city’s finance department for a business license requirement before you assume you owe nothing.

AB5 and why your clients still treat you like a risk

Assembly Bill 5 took effect January 1, 2020 and is still law. It made the ABC test the default for deciding whether a worker is an independent contractor or an employee, and it presumes you are an employee unless the hiring business can prove otherwise. AB 2257, signed in September 2020, added exemptions that cover most knowledge-work freelancers: writers, editors, copy editors, translators, photographers, videographers, illustrators, fine artists, graphic designers, and marketers, among others.

The piece that affects your money is the business-to-business exemption under Labor Code section 2776. It lets one genuine business contract with another outside the ABC test, but only if twelve conditions are met. You need a separate business location, any required business license, the freedom to set your own rates and hours, and the ability to contract with other clients.

This is why some California clients ask you to form an entity or show a city business license before they will pay you as a contractor. They are protecting themselves from misclassification liability. Holding an LLC and a city registration helps satisfy those conditions, which is one of the few arguments for the $800 cost beyond liability protection. When a client does pay you this way, expect a 1099-NEC at tax time; our step-by-step guide on handling a 1099-NEC covers what to do when one lands.

California deductions and moves worth claiming

Most federal business deductions flow through to your California return, but a few behave differently, and that difference can move your bill by hundreds or thousands of dollars.

- Home office. California follows the federal rules here. If you qualify, claim it on both returns. See our home office deduction guide for the method comparison.

- Ordinary business expenses. Software, equipment, mileage, and supplies reduce both your federal and California profit. Keep them clean with a system from our expense tracking guide.

- Half of self-employment tax. This federal adjustment flows to California too, lowering your state taxable income.

- Large equipment write-offs. California caps Section 179 expensing at $25,000 and does not follow federal bonus depreciation. A big camera or computer you fully wrote off federally may have to be depreciated over years on your California return. If your work leans visual, our deductions guide for freelance designers flags the gear write-offs worth tracking.

- Pass-through entity elective tax. If you have elected S-corp or partnership treatment, California’s PTE elective tax can recover some of the federal state-and-local-tax deduction you lost. A plain sole proprietor cannot use it.

California also runs its own credits, including the California Earned Income Tax Credit and a small renter’s credit ($60 single, $120 joint, subject to income limits). Most freelancers earning $45,000 or more phase out of the bigger ones, but check eligibility when you file Form 540.

For the full list of write-offs that apply on the federal side, work through our tax deductions freelancers miss and the line-by-line Schedule C walkthrough. Both feed directly into the numbers California then taxes.

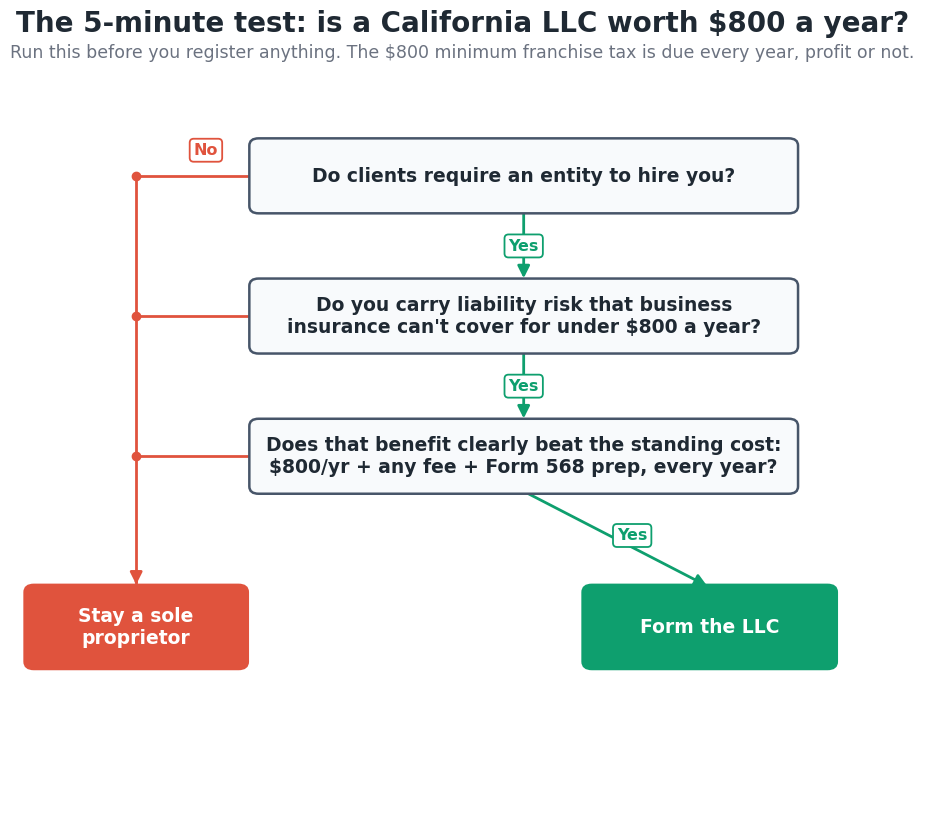

The 5-minute test: is a California LLC worth $800 a year?

Run this before you register anything. It takes five minutes and saves you the most expensive avoidable bill in this guide.

- Do clients require an entity to hire you, or are they fine paying a sole proprietor? If they are fine, the case for an LLC weakens fast.

- Do you carry real liability risk, such as work that could cause a client financial loss? If not, business insurance may cover you for less than $800 a year.

- Will you clear roughly $250,000 in gross receipts soon? If yes, factor in the LLC fee on top of the $800.

- Add it up: $800 minimum tax, plus any fee, plus Form 568 prep, every year, regardless of profit. That is your standing cost.

- If the benefits in steps 1 and 2 clearly beat that standing cost, form the LLC. If they do not, stay a sole proprietor and revisit next year.

If you do decide to form one, compare providers in our review of the best LLC formation services for freelancers so you are not overpaying on setup. We explain how we test these in our methodology.

Your California freelancer tax deadline checklist

Here is every California deadline that costs money if you miss it, pulled together in one place. Dates are for the 2025 tax year filed in 2026; the city figures shift yearly, so confirm them with each city before you rely on them.

| Deadline | Date | What it covers | Who it applies to |

|---|---|---|---|

| 1st estimated payment (30%) | April 15, 2026 | California front-loads at 30/40/0/30, not four equal quarters | Anyone expecting to owe more than $500 after withholding |

| $800 minimum franchise tax (Form 3522) | April 15, 2026 | The flat $800 every LLC owes, even at a loss | LLCs, LPs, and corporations only |

| 2nd estimated payment (40%) | June 15, 2026 | The largest of the four California installments | Freelancers paying estimates |

| LLC fee (Form 3536) | June 15, 2026 | $900 to $11,790 once gross receipts top $250,000 | LLCs over $250,000 in gross receipts |

| 3rd estimated payment (0%) | September 15, 2026 | No California payment due, but your federal one still is | Freelancers paying estimates |

| 4th estimated payment (30%) | January 15, 2027 | Final California installment for the year | Freelancers paying estimates |

| San Francisco business registration renewal | Last day of February (March 2 for the 2025 cycle) | Register and renew even when exempt from the gross receipts tax under $5M | Anyone doing business in San Francisco |

| Los Angeles business tax renewal | March 2, 2026 | File on time to keep the small business or creative artist exemption | Anyone doing business in Los Angeles |

One reminder that is not a date: California does not honor the federal QBI deduction. Whatever you deduct under Section 199A on your federal return, add it back on Schedule CA (540), because the state taxes the full amount. Budget for that gap so your California bill does not surprise you.

Frequently Asked Questions

Do freelancers in California have to pay the $800 LLC tax?

Only if you have formed an LLC, LP, or corporation. Sole proprietors who file a Schedule C do not owe it. Once you register an LLC, you owe the $800 minimum franchise tax every year, even at a loss, and there is no first-year waiver anymore. The AB 85 exemption that covered first-year LLCs expired at the end of 2023, so any LLC formed in 2024 or later pays from year one using Form 3522.

How much should I set aside for taxes as a California freelancer?

Plan to set aside more than the 25% to 30% national rules of thumb suggest, because California income tax stacks on top of the 15.3% federal self-employment tax and your federal income tax. For many freelancers earning $60,000 to $110,000, total set-aside lands somewhere around 30% to 38% of net profit. Run your own numbers with our set-aside guide rather than guessing, then adjust quarterly as income changes.

Does California have a self-employment tax?

No. The 15.3% self-employment tax is federal only, covering Social Security and Medicare. California taxes your net business profit as ordinary income through its regular brackets, which run from 1% to 12.3% plus a 1% surcharge over $1 million. So a California freelancer pays federal income tax, federal self-employment tax, and California income tax, but no separate state self-employment tax.

Why is my California estimated tax schedule different from federal?

California front-loads estimated payments on Form 540-ES at 30% in the first quarter, 40% in the second, 0% in the third, and 30% in the fourth. The IRS uses four equal 25% payments. If you copy the federal split, California can charge an underpayment penalty because the FTB tests each period separately, even when your annual total is correct. You owe California estimates once you expect to owe more than $500 after withholding.

Do I need a business license to freelance in Los Angeles or San Francisco?

Yes. Los Angeles requires a Business Tax Registration Certificate for anyone doing business in the city, and San Francisco requires annual business registration. In both cities you must file even when an exemption zeroes out your tax. Los Angeles exempts small businesses under $100,000 and creative artists under $300,000, but only if you file the renewal on time. Miss it and you lose the exemption and owe tax plus penalties.

Can I take the QBI deduction on my California taxes?

No. California does not conform to the federal qualified business income deduction under Section 199A, and it did not adopt the One Big Beautiful Bill Act that made the deduction permanent at 20%. You can claim it on your federal return, but California adds the full amount back, so your state taxable income is higher than your federal taxable income. Budget for that gap when you estimate your California payments.

Do I owe California taxes if I moved into or out of California this year?

If you moved during the year, you file as a part-year resident on Form 540NR. California taxes the income you earned while you were a resident, plus any California-source income you earned while you were a nonresident. If you live outside California but have California clients, the state can still tax the income sourced to it. Moving away does not erase tax on income you earned while you lived there, so prorate carefully and keep records of your move date.

Is AB5 still in effect for California freelancers in 2026?

Yes. AB5 has been law since January 1, 2020, and AB 2257 added exemptions in late 2020 that cover most knowledge-work freelancers, including writers, designers, photographers, translators, and editors. The ABC test still presumes worker status is employment unless the hiring business proves otherwise. The business-to-business exemption lets genuine businesses contract freely if twelve conditions are met, which is why some clients ask you to hold an entity and a business license.

Start by running the 5-minute LLC test above and confirming whether your city needs a business registration this year. Those two checks catch the most expensive surprises in this guide. For the national picture beyond California, see our state-by-state freelance tax guide.

This article is informational and not tax or legal advice. California tax law, rates, and city rules change, and your situation may differ. Verify current figures at ftb.ca.gov, your city’s finance department, and irs.gov, and consult a CPA or tax professional before making decisions.

About the author

Gareth Noble is the founder of Freelancer Profit. He’s not a CPA or a bookkeeper. He spent 20 years coaching teams at companies like Amazon, P&G, and Emirates before building this site, because he couldn’t find honest, thorough reviews of finance tools written for freelancers. Every guide is researched from real user reviews, BBB complaints, official documentation, and primary sources.