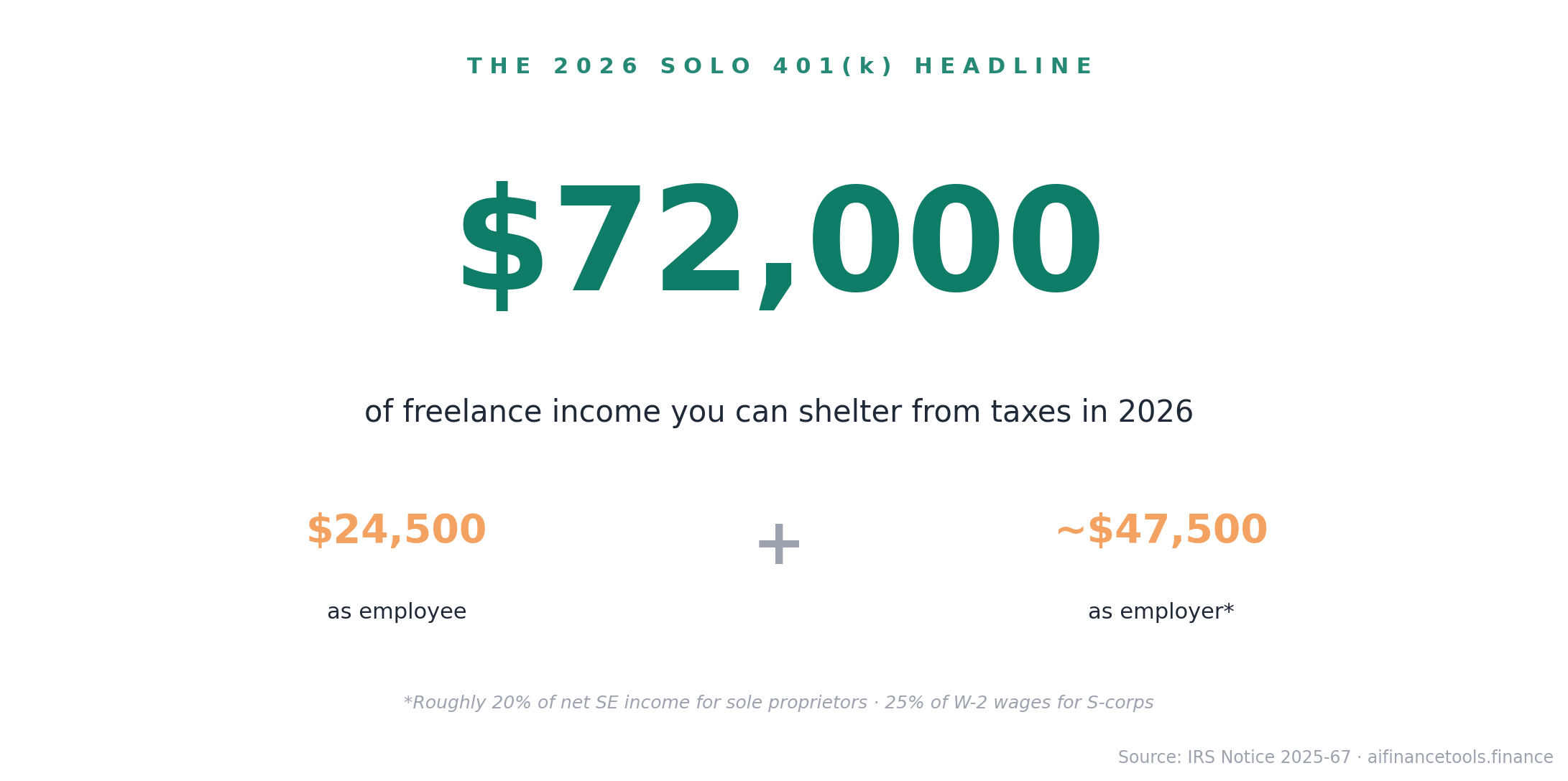

A solo 401k can shelter up to $72,000 of your freelance income from taxes in 2026. Here is who qualifies, how the math actually works, and when it makes sense to open one.

Earn $120,000 in net self-employment income, and you can put up to $72,000 of it into a solo 401k in 2026. Most of that drops straight off your taxable income. The IRS set the 2026 limit in Notice 2025-67. Almost nobody told you it existed.

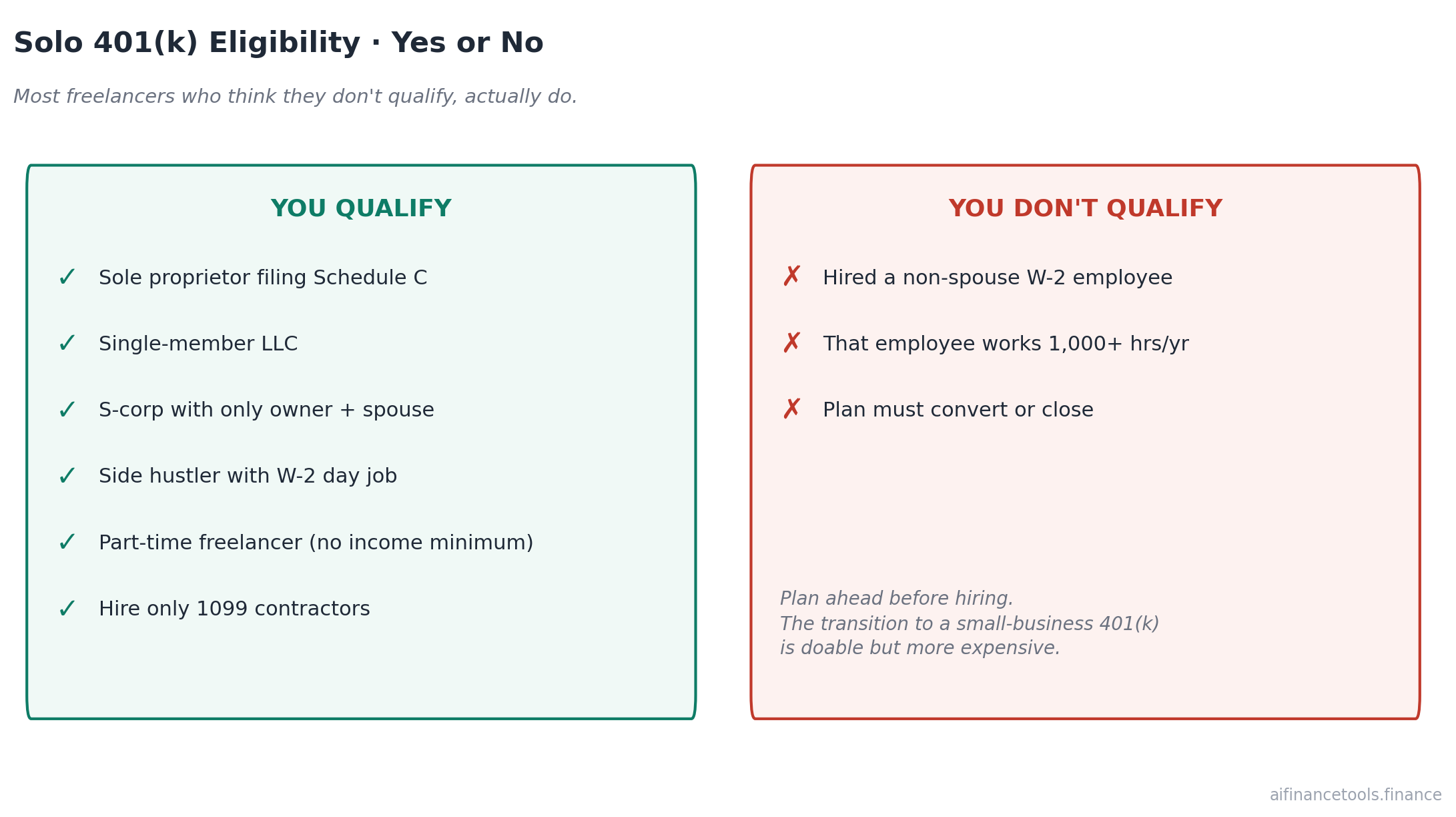

If you have been freelancing for two or three years and you assume everyone else has the retirement-account thing figured out, they don’t. Most freelancers I talk to have no idea this account is open to them. The ones who have heard of it usually assume it is for older business owners with employees, lawyers, and a full-time bookkeeper. Wrong on every count. If you file a Schedule C, earn at least a few thousand dollars in self-employment income, and have no full-time W-2 employees, you qualify.

This guide covers what a solo 401k is, who can open one, the 2026 contribution limits with worked examples at $80k and $150k of income, and the income point where it stops making sense compared to a Roth IRA. No advisor speak. The math and the rules.

What is a solo 401k

A solo 401k is a retirement account for self-employed people who have no full-time employees. The one exception is a spouse who works in the business. The IRS calls it a “one-participant 401(k) plan.” Some providers brand it as a Solo K, an Individual 401(k), or a Uni-K. Same account, different label. All three names mean the same qualified retirement plan in the eyes of the IRS.

It works like a regular workplace 401k with one twist: you are both the employee and the employer. That dual role is the whole point. You contribute in both capacities, which is why the total limit ($72,000 in 2026) sits far above what a W-2 employee can put away through their day job.

How does a solo 401k work

A solo 401k has two contribution buckets. You fill them separately. The rules for each are different, and yes, this part takes a few minutes to wrap your head around.

Bucket 1: employee elective deferral

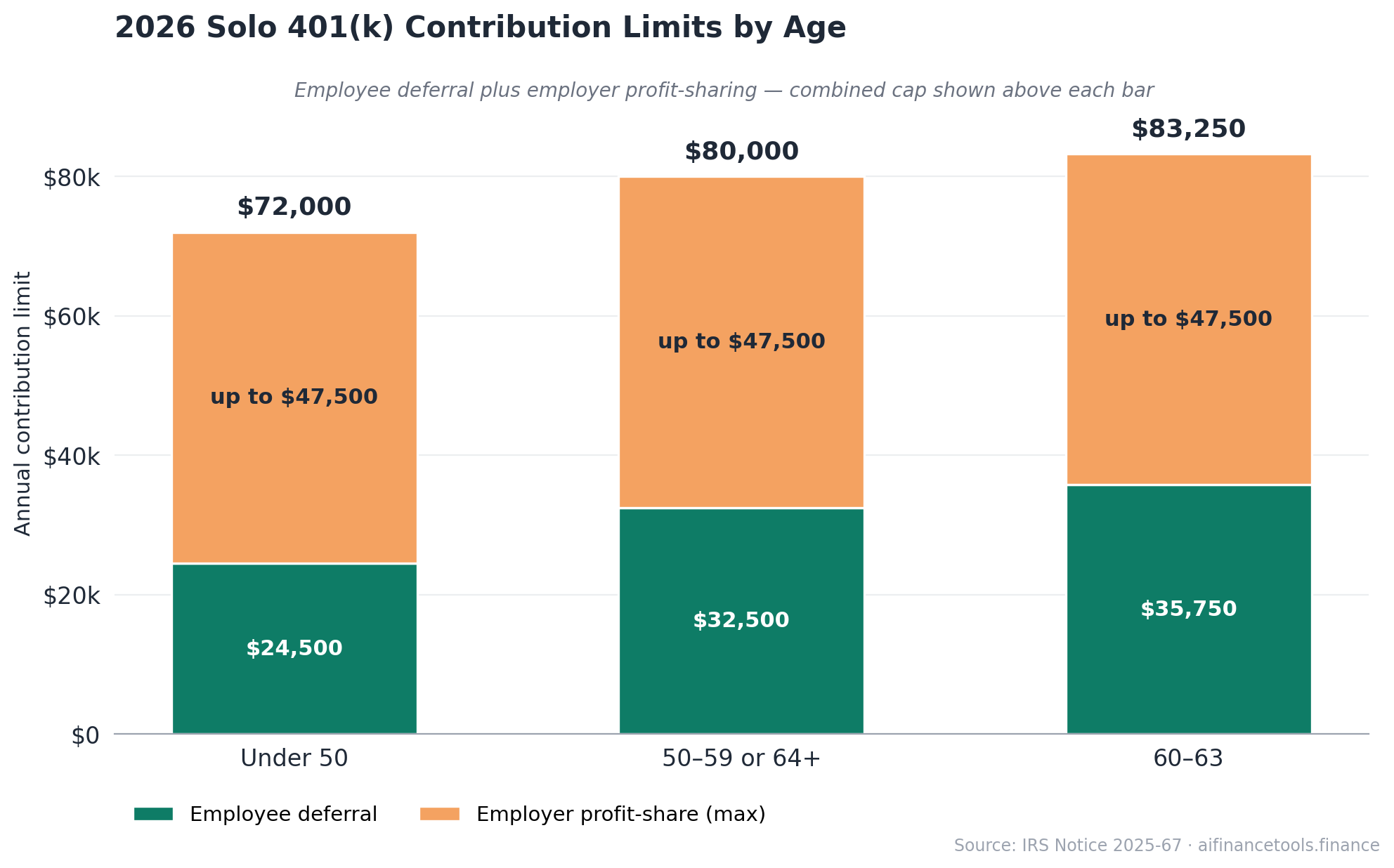

This is the same kind of contribution a W-2 employee makes from their paycheck. For 2026, you can defer up to $24,500 of your self-employment income, either pre-tax or Roth. If you are 50 to 59 or 64 and older, you can add an $8,000 catch-up, which takes your employee total to $32,500. If you are 60 to 63, the catch-up jumps to $11,250 under SECURE 2.0, and your employee total reaches $35,750.

One catch worth flagging early. The $24,500 limit applies across all 401k accounts you have. If you also work a W-2 day job and contribute $20,000 to that 401k, you only have $4,500 of employee deferral space left in your solo 401k. People miss this every year and end up filing corrections. Do not feel stupid if it surprises you. The IRS does not exactly send a memo.

Bucket 2: employer profit-sharing contribution

This is the contribution you make as your own employer. The IRS uses the term “earned income” to describe the compensation figure that drives the calculation. For sole proprietors and single-member LLCs, that means net self-employment earnings minus half of self-employment tax, and the employer contribution lands at roughly 20% of that. For S-corp owners taking a W-2 salary, it is 25% of that wage.

The reason it shakes out to 20% rather than 25% for sole proprietors is that the IRS calculates the percentage on net earnings after backing out the contribution itself. The arithmetic gets ugly fast. You do not need to do this by hand. Every solo 401k provider has a calculator that handles it.

The combined cap

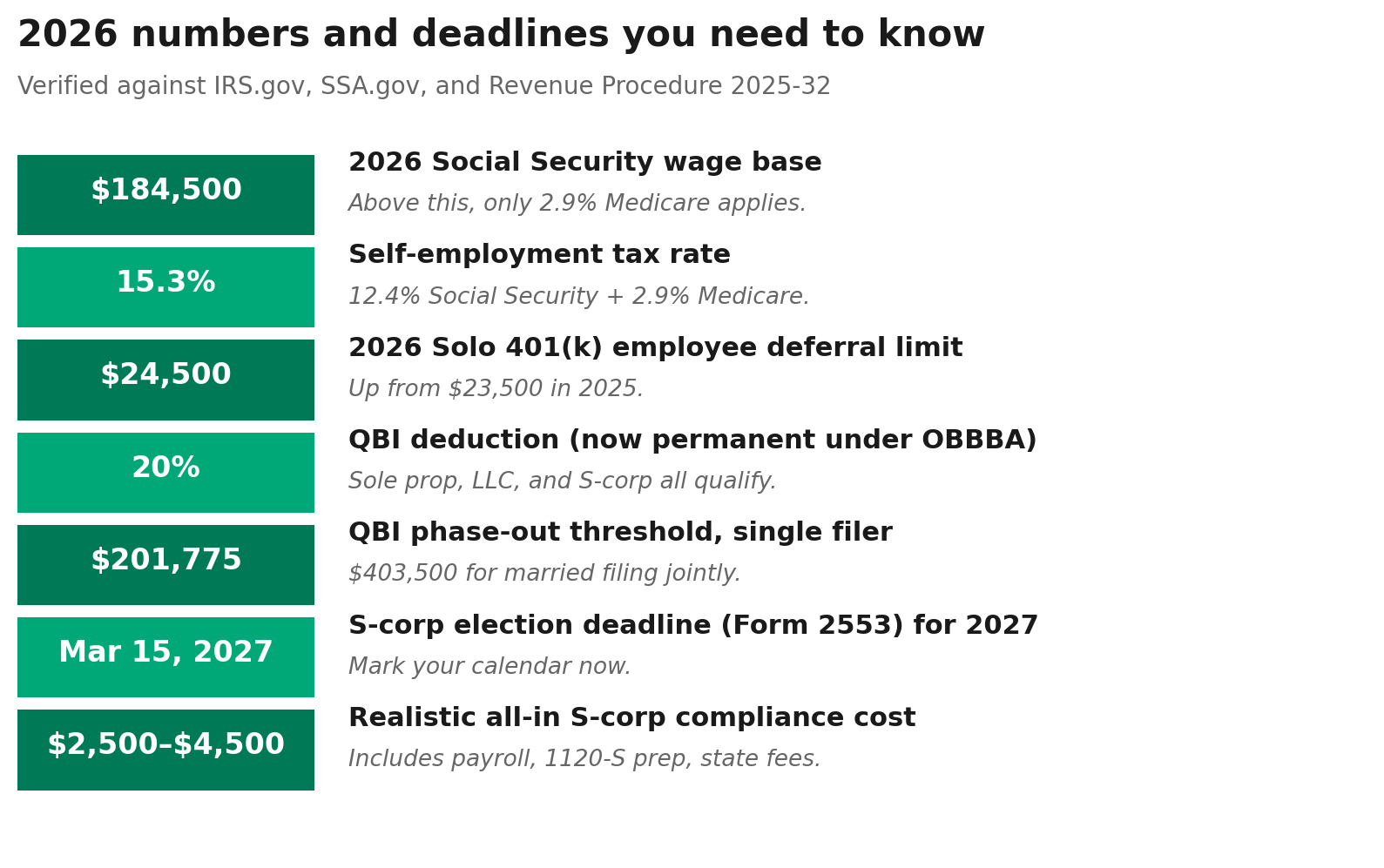

Your two buckets together cannot go past $72,000 in 2026. With the $8,000 catch-up that ceiling rises to $80,000, and with the $11,250 super catch-up it rises to $83,250. The IRS also caps the compensation it will look at when calculating contributions at $360,000 for 2026, so very high earners hit a ceiling before the math runs out.

Who can open a solo 401k

The eligibility rules are simpler than most people assume. If you have looked at this account before and decided “that is not for me,” there is a decent chance you were wrong. You qualify if you have self-employment income and no full-time W-2 employees other than your spouse.

- Sole proprietors filing Schedule C. Yes, even with no LLC.

- Single-member LLCs. Treated the same as sole proprietors for solo 401k purposes, unless you elected S-corp taxation.

- S-corporations with no W-2 employees besides the owner and a spouse. Contributions get based on your W-2 wages, not total business profit.

- Partnerships where the only partners are you and a spouse, or you are the sole working partner.

- Side hustlers with W-2 day jobs. If your freelance gig is genuinely your own business, you can open a solo 401k just for that income while still contributing to your day job’s plan.

- Part-time freelancers. No minimum income to qualify. The constraint is what the math lets you contribute, not whether you are eligible.

Here is the disqualifier. The day you hire a non-spouse employee who works more than 1,000 hours a year, the solo 401k is no longer viable. You either close it, convert it to a regular 401k that covers them, or wait out their eligibility window. 1099 contractors do not count. You can hire a dozen different freelancers as 1099 subcontractors and your solo 401k is fine.

Not sure which entity structure you are in? That is also normal. Read the freelancer entity comparison first.

Solo 401k contribution limits 2026

The official 2026 numbers come from IRS Notice 2025-67. The math worked out at two real freelancer income levels follows below. None of this works without clean books, so if you have not been tracking yet, tracking every business expense properly is the prerequisite to knowing your true net SE income.

- Employee deferral limit: $24,500

- Catch-up if age 50 to 59 or 64+: $8,000 (total employee deferral $32,500)

- Super catch-up if age 60 to 63: $11,250 (total employee deferral $35,750)

- Employer contribution: Up to 25% of compensation for S-corps. Roughly 20% of net SE earnings for sole proprietors.

- Combined cap (under 50): $72,000

- Combined cap (age 50 to 59 or 64+): $80,000

- Combined cap (age 60 to 63): $83,250

- Compensation limit used in calculations: $360,000

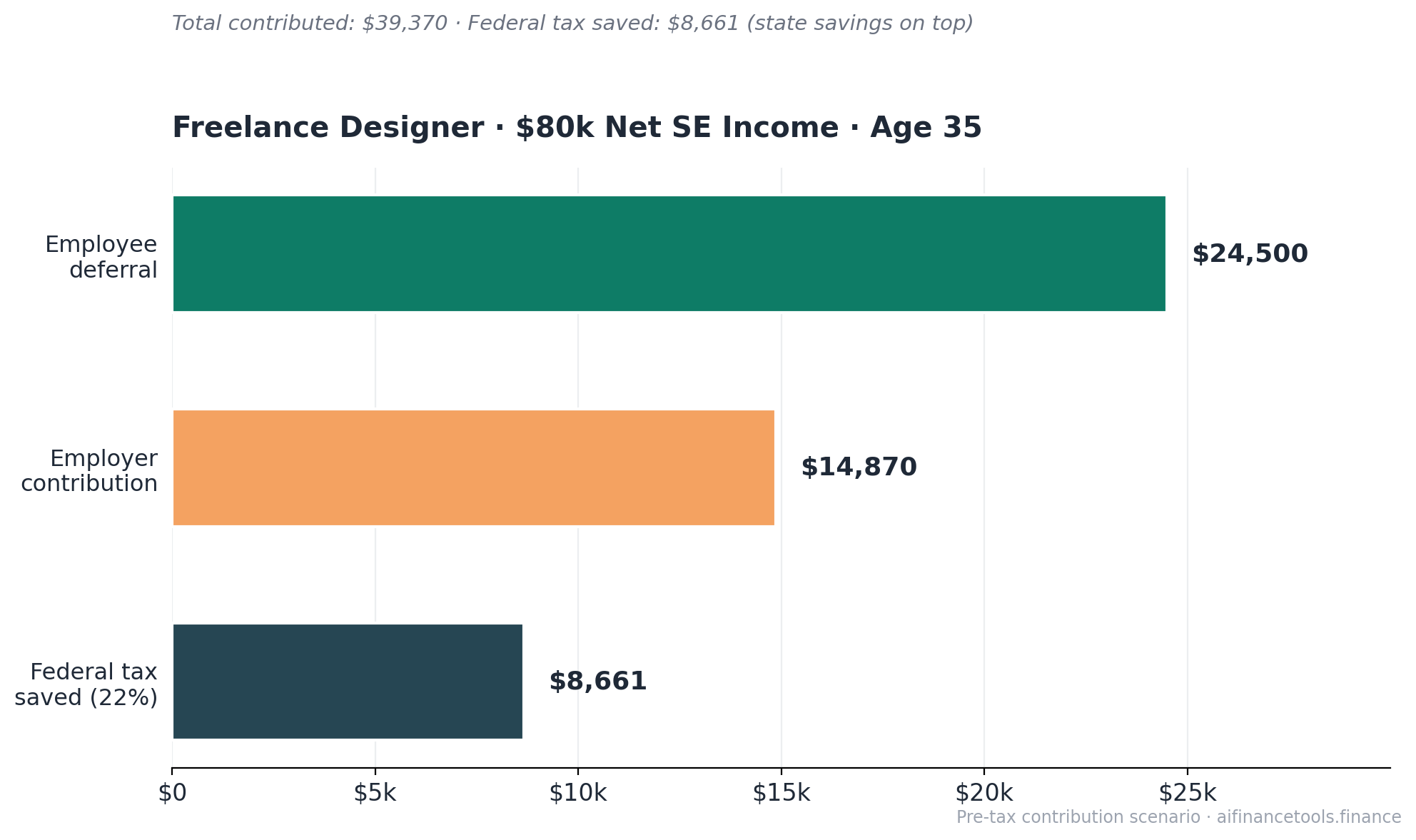

Worked example: freelance designer, $80,000 net SE income, age 35

A freelance designer files Schedule C with $80,000 in net self-employment earnings. After backing out half of self-employment tax (roughly $5,652), her base for the employer contribution is about $74,348. Twenty percent of that lands at roughly $14,870.

- Employee deferral: $24,500 (the full limit)

- Employer contribution: ~$14,870

- Total going into the solo 401k: ~$39,370

If she takes the whole contribution as traditional pre-tax, that reduces her taxable income by roughly $39,370 for the year. At a 22% federal marginal rate, that comes out to about $8,661 less in federal tax this year, plus state savings on top. The Roth option puts taxes in now and pulls money out tax-free in retirement. Same contribution limit, different timing. If reading “$8,661 in federal tax saved” makes you slightly upset that nobody told you about this in year one of freelancing, that is fair.

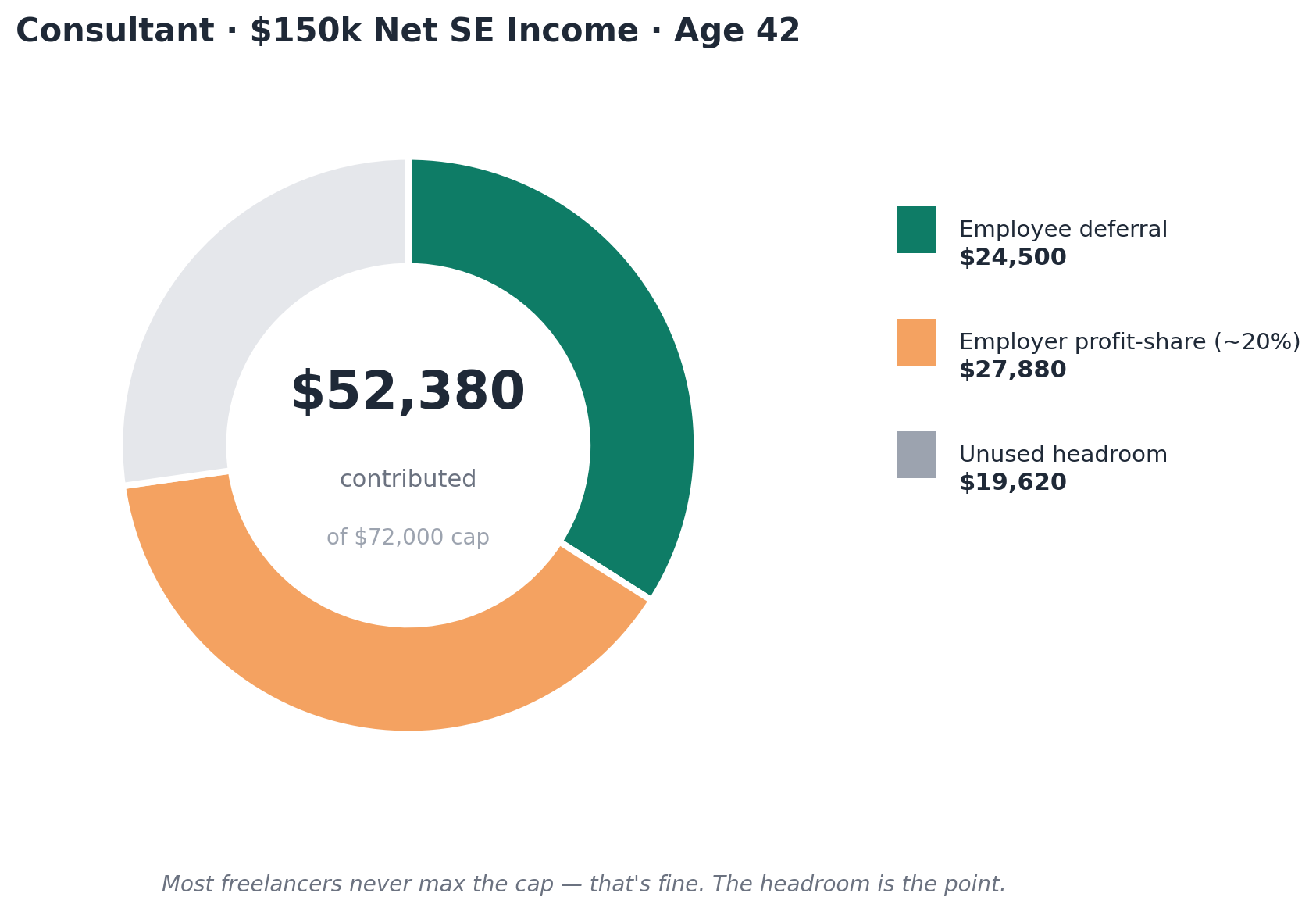

Worked example: consultant, $150,000 net SE income, age 42

A consultant nets $150,000 on Schedule C. Half of SE tax is roughly $10,597, leaving about $139,403 as the base. Twenty percent of that lands at roughly $27,880.

- Employee deferral: $24,500

- Employer contribution: ~$27,880

- Total going into the solo 401k: ~$52,380

Still well under the $72,000 cap. To max it out, he would need closer to $250,000 in net SE income. Most freelancers will never max a solo 401k. That is fine. The point is the headroom you have, not whether you fill it.

If you are still figuring out how much to set aside in cash before you can think about retirement, start with the freelancer tax set-aside calculator. Cash flow first, retirement second.

Solo 401k benefits

Why pick a solo 401k over a SEP IRA or a regular Roth? Four practical reasons. (Compare to a SEP IRA in our side-by-side Solo 401k vs SEP IRA guide.)

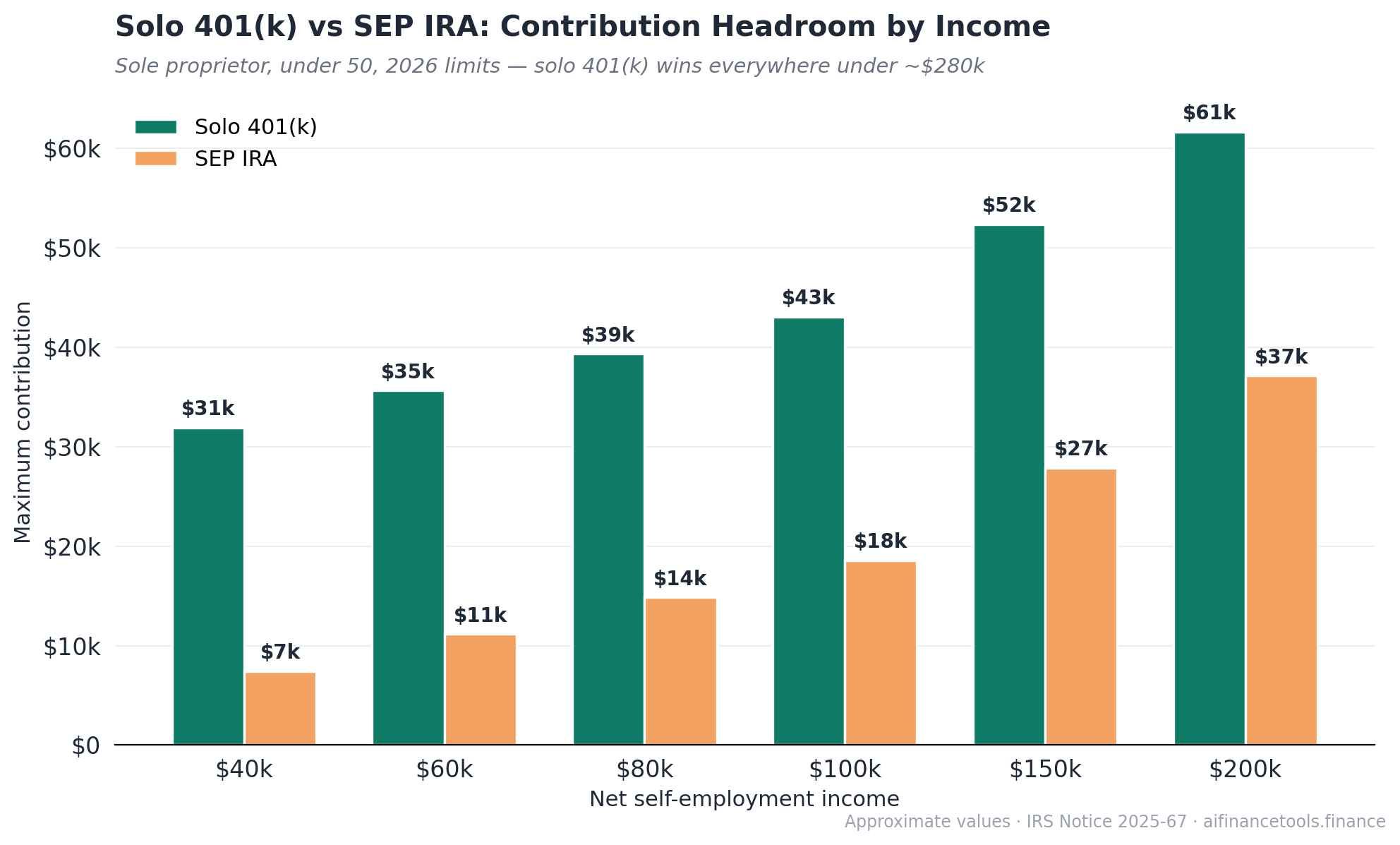

- Higher contribution room at moderate income. A SEP IRA only allows employer-style contributions of up to 25% of compensation. To hit a $70,000 SEP contribution in 2025, you needed about $280,000 in earnings. A solo 401k lets you stack the $24,500 employee deferral on top, so you can contribute meaningfully at $60,000 or $80,000 in income.

- Roth option that actually works. Most solo 401k providers now allow Roth employee deferrals. SEP IRAs technically allow Roth under SECURE 2.0, but provider support is patchy in practice. If you want tax-free retirement income, a solo 401k Roth is more reliable.

- Loan provision. You can borrow up to 50% of your balance, capped at $50,000, and pay yourself back over five years. SEP IRAs do not allow loans. This matters if you ever need a bridge during a slow quarter.

- Tax deduction now, or tax-free later. You pick. Pre-tax contributions reduce your current taxable income, which is one of the cleanest ways to avoid a tax liability shock at year-end. Roth contributions come from after-tax dollars but grow tax-free. You can split between the two in the same year.

Solo 401k vs SEP IRA: the short version

Most freelancers comparing self-employed retirement accounts come down to these two. The short version, since the full Solo 401k vs SEP IRA comparison for freelancers gets its own piece:

- Under $200,000 in net SE income: Solo 401k almost always wins because the $24,500 employee deferral lets you shelter more than a SEP IRA can at the same income.

- Multiple businesses or expecting to hire: SEP IRA wins on simplicity. No 5500-EZ filing ever. No issues if you eventually hire.

- Want the Roth option: Solo 401k. SEP IRAs technically allow Roth contributions now but most custodians have not built proper support yet.

If your income is north of $200,000 and you want to push past the $72,000 cap, that is where SEP IRAs, defined benefit plans, or after-tax solo 401k contributions come into the conversation. Most freelancers earning under $150,000 do not need to think about that yet.

Solo 401k drawbacks

This account is not free of friction. Three things to know before you open one. I am telling you these now because nothing is worse than finding out about a $250-a-day penalty after you have already missed the deadline.

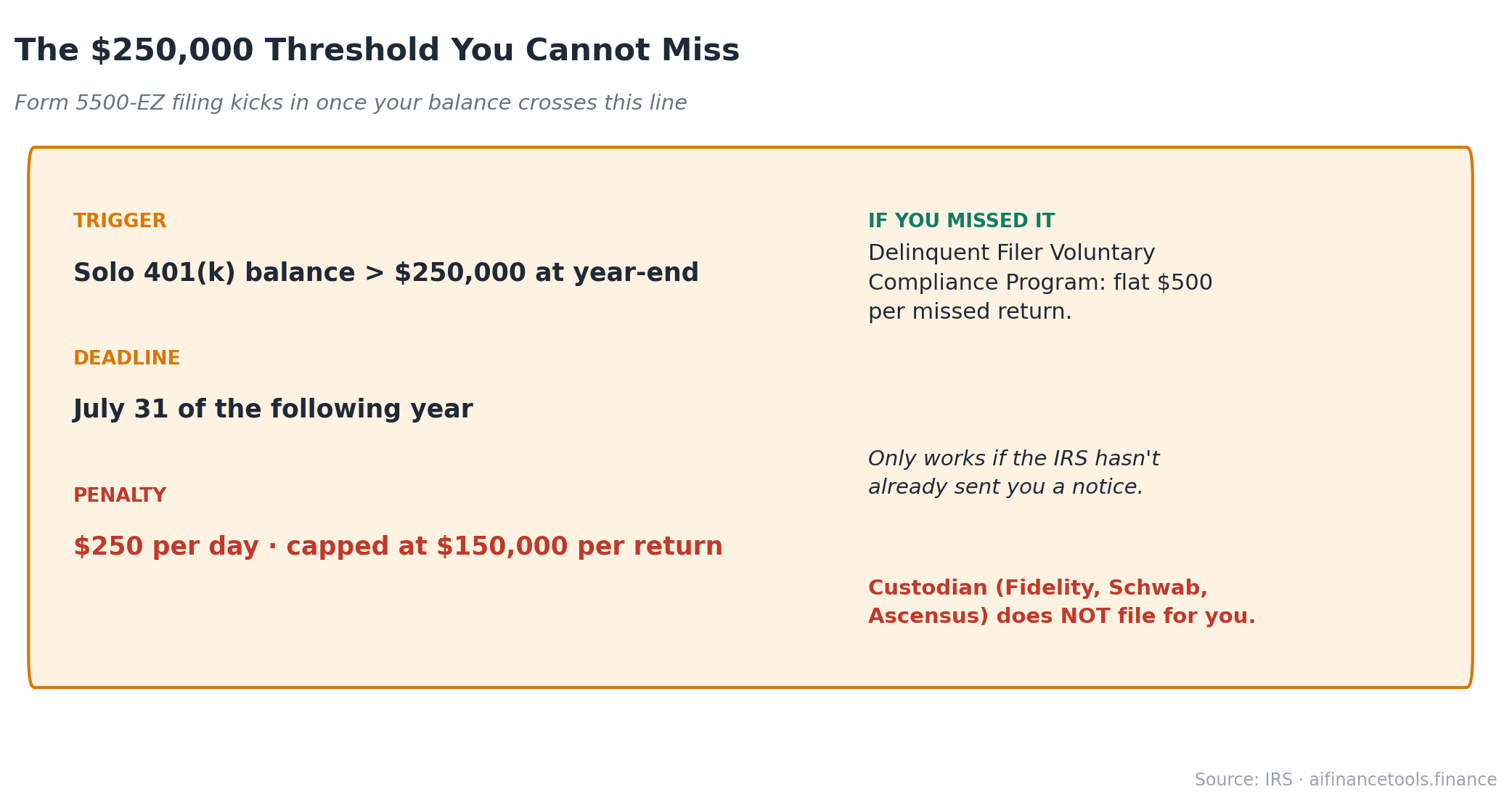

Form 5500-EZ once your balance hits $250,000

Once the total assets in your solo 401k go past $250,000 at the end of a calendar year, you must file Form 5500-EZ with the IRS by July 31 of the following year. Miss the deadline and the penalty runs $250 per day, capped at $150,000 per return. Your custodian (Fidelity, Schwab, Ascensus) does not file this for you. You do.

The form itself is short. The penalty for forgetting it is brutal. If you blow past the deadline, the Delinquent Filer Voluntary Compliance Program lets you fix it for a flat $500 per missed return, but only if the IRS has not already sent you a notice. Put it in your calendar the day you cross $250,000.

Setup paperwork

You need an EIN, which is free at IRS.gov and takes about 10 minutes. You need a written plan document, which the major brokers provide for free. You need to make a written employee deferral election by December 31 of the year you want it to count. The whole process takes about half an hour at Fidelity, Schwab, or Ascensus if your documents are ready.

Not allowed if you have full-time W-2 employees

The day you hire a non-spouse employee who works 1,000+ hours per year, the solo 401k stops being viable. Plan ahead if you are thinking about hiring. The transition to a regular small-business 401k is doable, but expensive.

New 2026 rule for high earners with W-2 income

Under SECURE 2.0, if you are 50 or older and had more than $150,000 in W-2 wages from your business in 2025, your 2026 catch-up contributions must be Roth (after-tax). This mainly affects S-corp owners paying themselves a high salary. Most sole-prop freelancers are unaffected because the rule technically applies to wages, not self-employment income, but the IRS has not fully clarified every edge case. If you fall into this group, make sure your plan document supports Roth catch-up contributions.

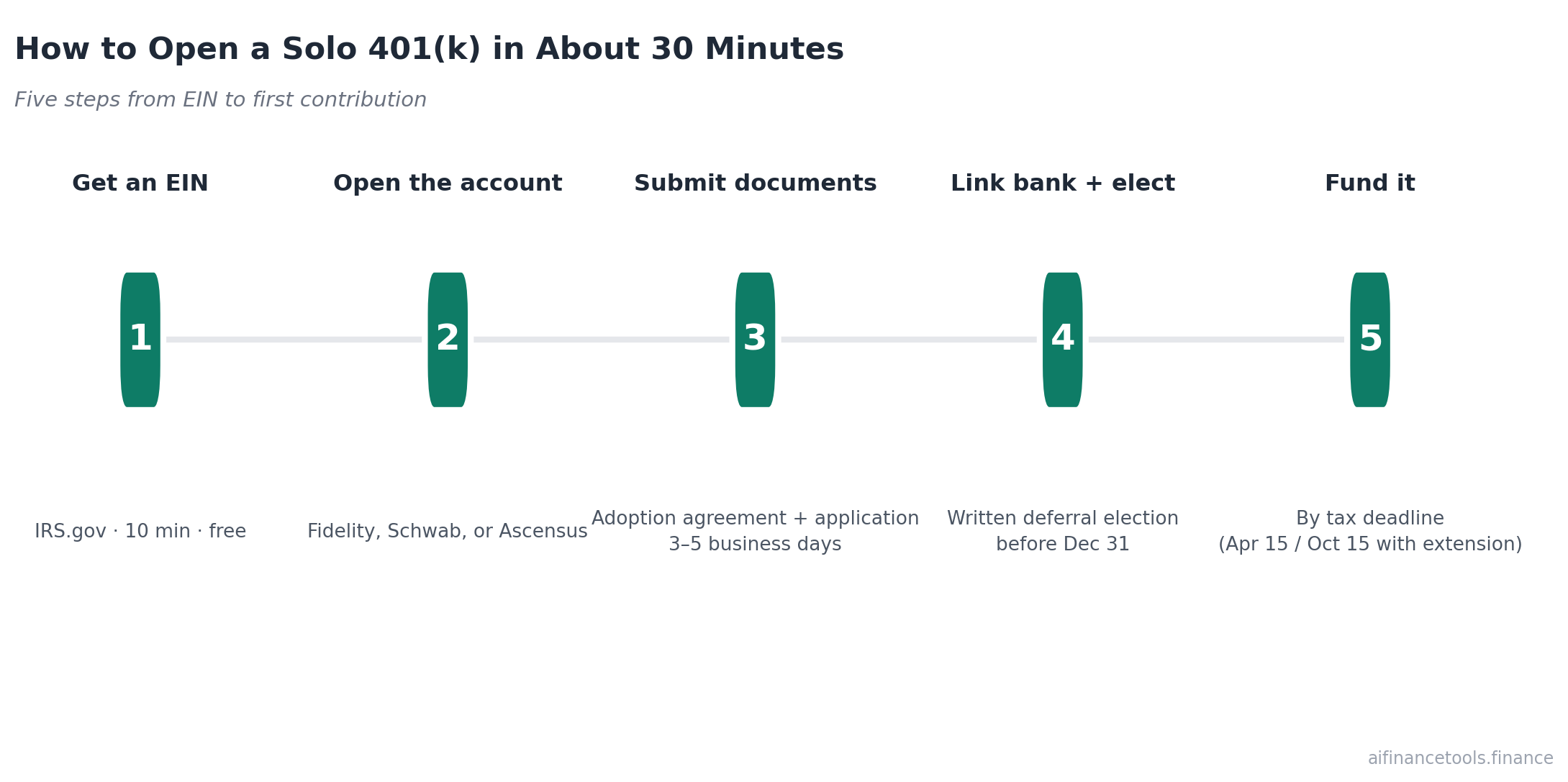

How to open a solo 401k in 30 minutes

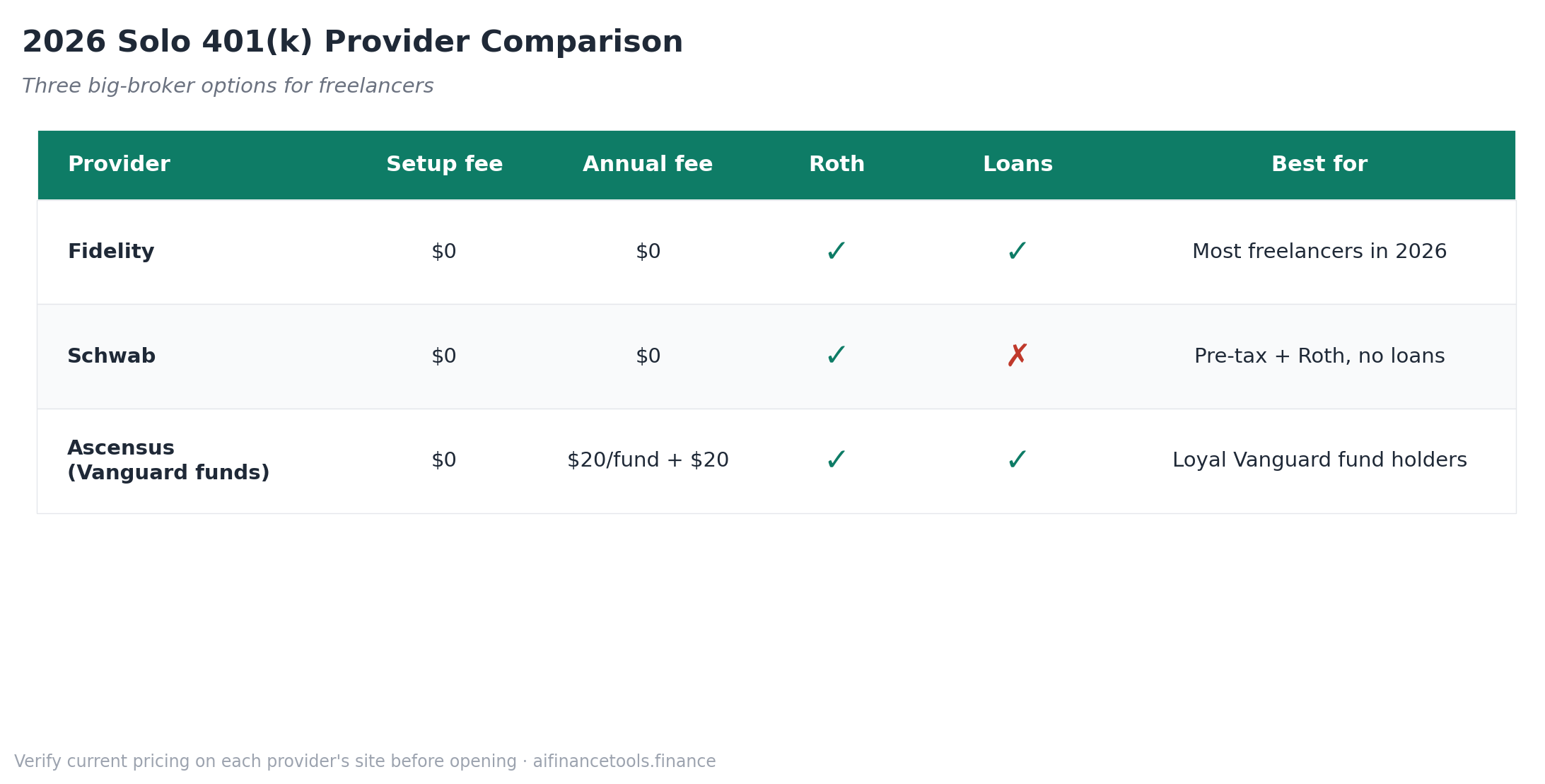

The big brokerages all offer solo 401k accounts with no setup fee and no annual fee. Fidelity is the most freelancer-friendly because its standard plan supports Roth contributions, allows electronic contributions from a linked bank account, and does not charge for the basic setup.

- Step 1. Get an EIN at IRS.gov if you do not already have one. Free, online, 10 minutes.

- Step 2. Open a Fidelity Self-Employed 401k account. You will fill out an adoption agreement (the plan document) and an account application. They give you both as PDFs.

- Step 3. Sign and submit the documents. Fidelity processes them in 3 to 5 business days.

- Step 4. Link a bank account. Make a written deferral election before December 31 if you want to contribute for the current year as an employee.

- Step 5. Fund it. Employee deferrals from self-employment income can be funded by your tax filing deadline (April 15, or October 15 if you extend). Employer profit-sharing has the same deadline.

Schwab and the Ascensus Individual(k) (formerly Vanguard’s plan) offer similar accounts. Schwab supports both pre-tax and Roth contributions and has no setup or annual fees, but the plan does not allow participant loans, which is the main limitation if you ever want to borrow from your balance. Vanguard exited the solo 401k business in 2024. What used to be the Vanguard plan is now an Ascensus Individual(k) holding Vanguard funds. Ascensus charges $20 per Vanguard fund per year plus a $20 custodial fee, which adds up if you hold several funds. For most freelancers in 2026, Fidelity is the cleanest option.

Specialized providers like Carry, Solo401k.com, and Rocket Dollar charge $300 to $1,500 in setup fees but allow self-directed investing in real estate, private equity, and crypto inside the account. Skip these unless you actually need the alternative-asset features.

Solo 401k for self employed: when does it actually make sense?

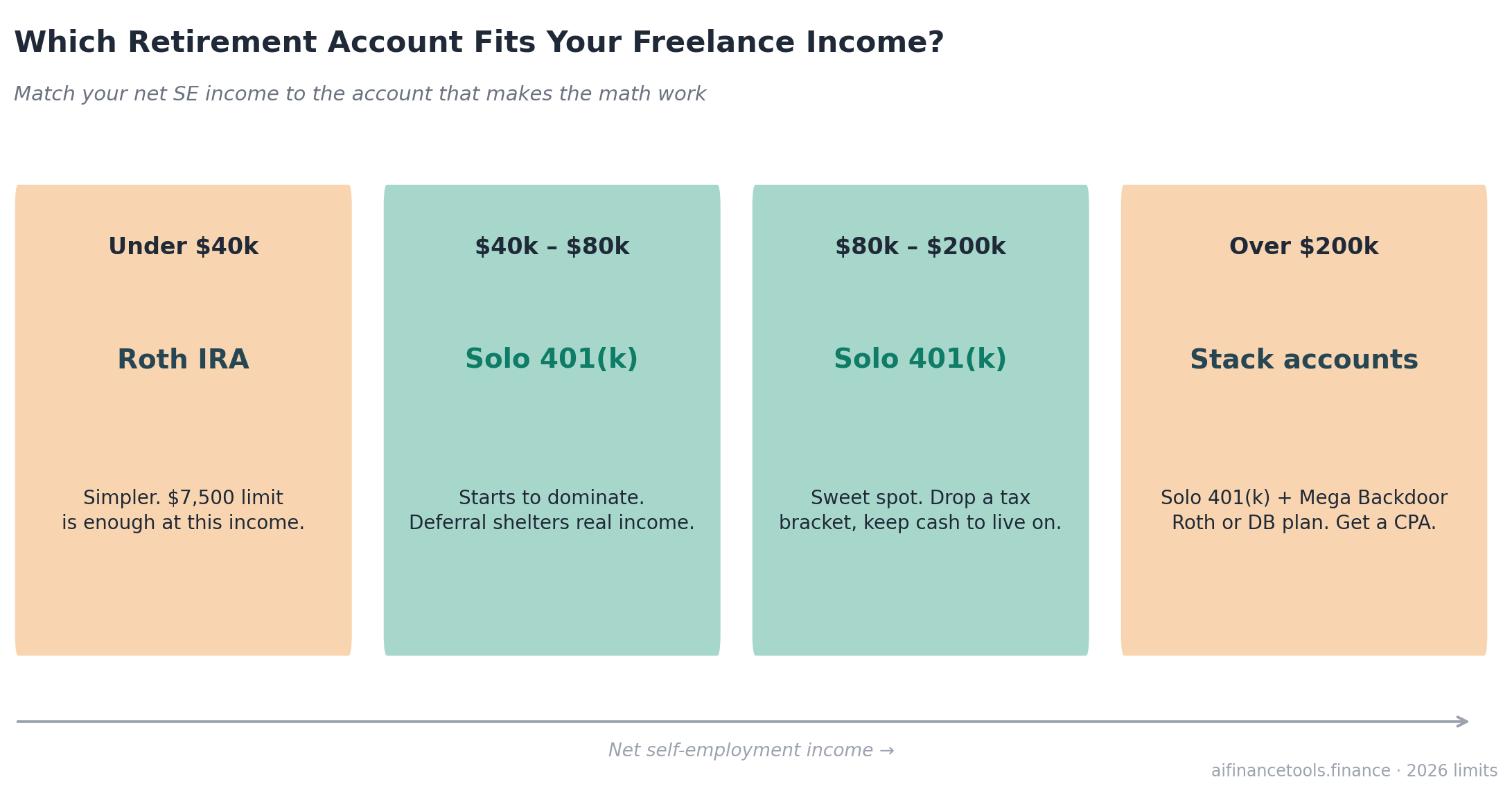

Here is the part most articles skip. A solo 401k is not the right account for every freelancer. Below a certain income, the simpler Roth IRA does the job and you skip the Form 5500-EZ filing risk altogether.

Under about $40,000 net SE income: stick with a Roth IRA

If your freelance income sits in the $20k to $40k range, a Roth IRA is enough. The 2026 limit is $7,500, or $8,600 if you are 50+. You will rarely max it at this income, and the Roth’s flexibility (you can pull contributions back out without penalty) genuinely helps when you need to manage cash flow as a freelancer during slow quarters.

$40,000 to $80,000: the sweet spot for a solo 401k

The solo 401k starts to dominate at this earnings level. The $24,500 employee deferral lets you actually shelter meaningful income, which a SEP IRA cannot match (a SEP would only allow about $7,400 to $14,870 at these incomes). If you can afford to set aside $10,000+ for retirement, open a solo 401k. The pre-tax version can also reduce your quarterly estimated tax payments for the rest of the year.

$80,000 to $200,000: where the solo 401k pays off the most

At this income range, the dual-bucket structure lets you defer tens of thousands per year while you are in your peak earning years. A freelance illustrator making $90,000 in their late 30s can shelter roughly $40,000 a year, drop a federal tax bracket, and still have take-home cash to live on.

Over $200,000: time to consider stacking accounts

If you can max the $72,000 solo 401k cap and still want to defer more, you are in defined-benefit-plan or after-tax solo 401k territory. At this income, strategies like the Mega Backdoor Roth (after-tax contributions converted to Roth inside the plan) become worth the extra plan complexity. That is a conversation for a CPA who specializes in self-employed retirement planning, and at this income level paying for one is worth it.

Get the freelancer tax-saving checklist

If retirement contributions are one piece of your tax plan, you also want to be claiming every legitimate Schedule C deduction you qualify for. Get the free checklist that walks through deductions most freelancers miss, the quarterly tax timeline for 2026, and the income thresholds that change which retirement account makes sense.

Frequently Asked Questions

Can a freelancer open a solo 401k?

Yes. Any freelancer with self-employment income who has no full-time W-2 employees other than a spouse can open one. You do not need an LLC, an S-corp, or a minimum income level. A sole proprietor filing Schedule C qualifies the same as a single-member LLC. The application process at Fidelity, Schwab, or Ascensus takes about 30 minutes once you have an EIN.

Do you need an LLC for a solo 401k?

No. The IRS does not require any specific business structure to open a solo 401k. Sole proprietors filing Schedule C are eligible. So are single-member LLCs, S-corps, partnerships, and C-corps where the only workers are the owner and a spouse. The entity choice affects how you calculate your contribution (S-corps base it on W-2 wages, sole proprietors base it on net SE earnings) but not whether you qualify.

What are the solo 401k contribution limits for 2026?

For 2026, you can contribute up to $24,500 as an employee deferral. On top of that, you can add an employer profit-sharing contribution of up to 25% of compensation, or roughly 20% of net SE earnings for sole proprietors. The combined cap is $72,000 if you are under 50, $80,000 if you are 50 to 59 or 64+, and $83,250 if you are 60 to 63. The IRS only counts compensation up to $360,000 when calculating these contributions.

When should freelancers open a solo 401k?

Open one when your net self-employment income is at least $40,000 per year and you have the cash flow to actually contribute. Below $40,000, a Roth IRA is simpler and the contribution limits are not really constraining you. Above $40,000, the solo 401k starts to matter because the $24,500 employee deferral lets you shelter income that a SEP IRA cannot reach at the same earnings level. Open the account by December 31 of the year you want contributions to count.

Solo 401k vs traditional 401k: what is the difference?

The contribution rules are nearly identical. Both have a $24,500 employee deferral limit for 2026 and a $72,000 combined cap. The differences are administrative. A traditional 401k is sponsored by an employer, has a third-party administrator, runs nondiscrimination testing, and covers all eligible employees. A solo 401k has no testing because there is only one participant (you, plus optionally a spouse). You also do not face employer-style fiduciary obligations until your balance reaches $250,000 and Form 5500-EZ kicks in.

Can you have a solo 401k and a regular 401k at the same time?

Yes, but the $24,500 employee deferral limit applies across all 401k accounts combined. If you contribute $20,000 to your day job’s 401k, you only have $4,500 of employee deferral space left in your solo 401k. The employer contribution side is separate, so you can still receive a match at your day job and make profit-sharing contributions to your solo 401k. This setup is common for side hustlers who want to shelter freelance income on top of W-2 income.

What happens to my solo 401k if I hire someone?

If you hire a full-time W-2 employee (1,000+ hours per year) who is not your spouse, your solo 401k is no longer eligible. You have a few options: convert it to a regular small-business 401k that covers the new employee, terminate the plan and roll your balance into an IRA, or restructure how you work with the new hire (1099 contractors do not affect eligibility). Plan this before you make the hire, not after.

What is the deadline to set up a solo 401k for 2026?

You must establish the plan and make a written employee deferral election by December 31, 2026 to count contributions for the 2026 tax year. The actual money does not have to hit the account by then. Employee and employer contributions for self-employed individuals can be funded up until your tax filing deadline including extensions, so April 15, 2027, or October 15, 2027 if you file Form 4868 for an extension. Open the account well before December to avoid processing delays.

Once the solo 401k decision is sorted, the next question most freelancers ask is which broader retirement account fits their situation, including the SEP IRA comparison. That is covered in the entity structure guide alongside the tax-account question.

This article is informational only and is not tax, legal, or investment advice. Tax laws change. Verify current IRS limits at IRS.gov before making contributions, and talk to a CPA or qualified financial advisor about your specific situation. The 2026 figures cited come from IRS Notice 2025-67.

About the author

Gareth is the founder of Freelancer Profit, a Dubai-based entrepreneur with a business consulting and leadership coaching background. He built the site to give freelancers honest, affiliate-free reviews of finance and tax tools, every one researched from official documentation, current pricing, and hundreds of real user reviews across Trustpilot, the BBB, and the app stores. It’s independent research, not professional tax advice, so check your own situation with a CPA.