Stop getting hit with tax bills you didn’t see coming. Learn how to avoid tax liability shock by knowing what you owe, planning for it, and paying on time so April never blindsides you again.

It’s April 14th. You open your accounting software to file. The number on screen makes your stomach drop. To avoid tax liability shock, you need a system that runs all year, not a panic plan in April. You owe $8,000.

You don’t have $8,000. You spent it months ago. Rent. Tools. Groceries. The slow stretches when clients paid late. Now the IRS wants it back by tomorrow.

This is tax liability shock. It hits freelancers every April. You earned plenty of money during the year. Nobody explained how self-employment tax actually works once you stopped being an employee, or how a 1099-NEC or 1099-K turns into a tax bill three months later.

Here’s the problem in plain terms. As an employee, your company withheld taxes from every paycheck before you saw the money. You never had to think about it. As a freelancer, the full amount lands in your account and feels like yours. A chunk of it isn’t. The IRS doesn’t send reminders through the year. They send a bill in April.

This is fixable. You don’t need an accounting degree. You need to understand how much you owe, when you owe it, and what you can legally knock off the top. The rest of this guide covers each piece.

Why Freelancers Pay More Tax Than Employees

Before you can plan for the bill, you need to understand why it’s bigger than you thought.

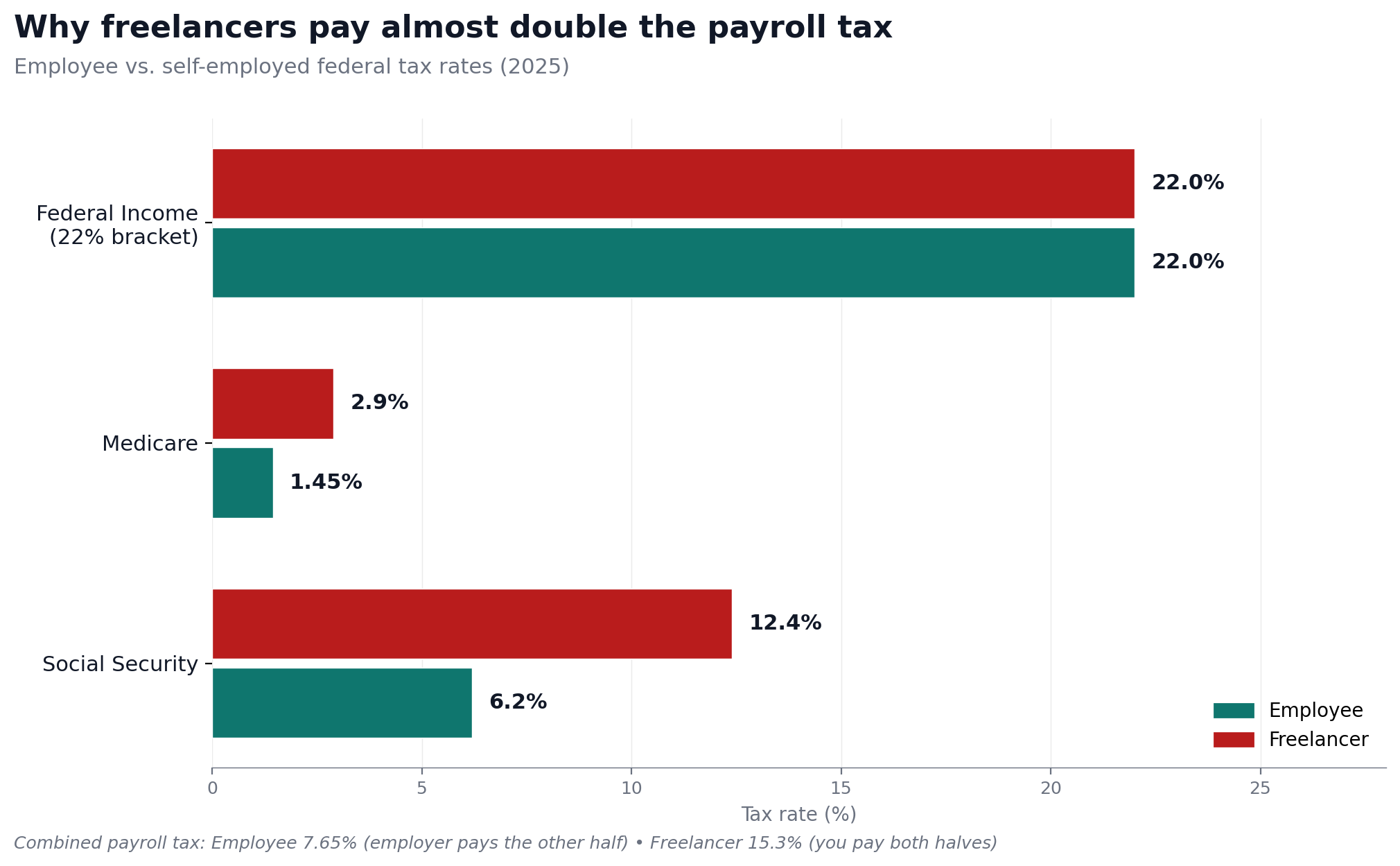

When you worked for a company, your employer covered half of your Social Security and Medicare taxes. You paid 7.65% out of each paycheck. They matched it. You never saw their share, because it never touched your account.

The moment you went freelance, that changed. You now pay both halves. The full 15.3%.

Here’s the 2025 breakdown. Social Security tax runs at 12.4% on net self-employment income up to $176,100. Medicare tax adds 2.9% on all net income, with no earnings cap. Together that’s 15.3% in self-employment tax, before a single dollar of income tax shows up. An additional 0.9% Medicare surcharge applies once your self-employment income passes $200,000 single or $250,000 married, though most freelancers won’t hit that ceiling.

One note on the math. The IRS applies self-employment tax to 92.35% of your net self-employment income, not 100%. That brings the effective rate down to roughly 14.13% of gross. This calculation happens on Schedule SE when you file your Form 1040. You can also deduct half of your self-employment tax when you calculate adjusted gross income, which softens the hit further. Even with both adjustments, the final number still surprises most people.

Here’s what this looks like in practice for a freelancer earning $50,000:

| Tax Type | Employee | Freelancer |

|---|---|---|

| Social Security tax | 6.2% (employer pays other 6.2%) | 12.4% (you pay both halves) |

| Medicare tax | 1.45% (employer pays other 1.45%) | 2.9% (you pay both halves) |

| Total payroll tax | ~7.65% | ~15.3% |

| Federal income tax (22% bracket) | Withheld automatically | You pay this separately |

| Combined marginal rate (at 22% bracket) | ~29% | ~37% |

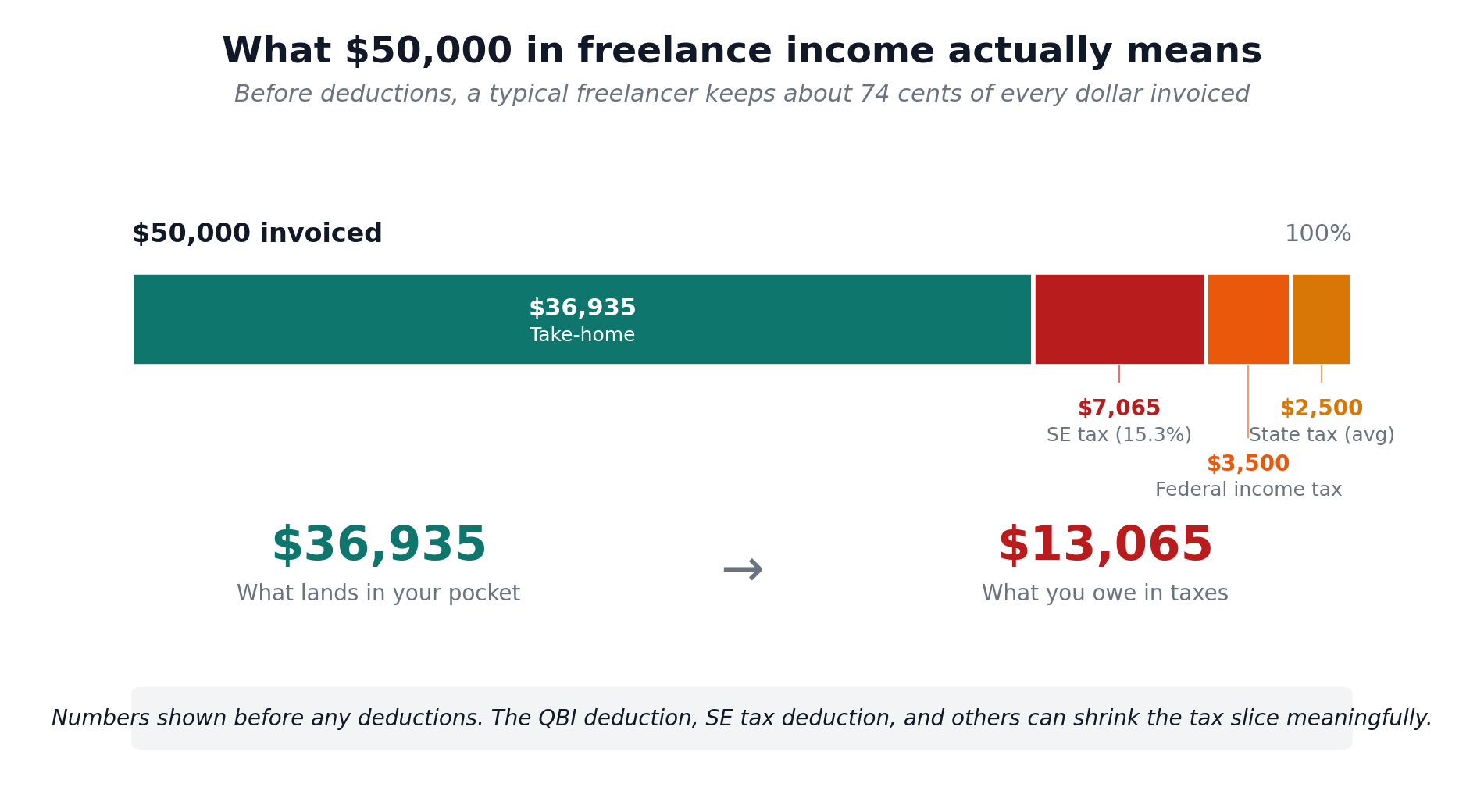

The gap between what an employee experiences and what a freelancer actually owes is where the shock lives. Earn $50,000 as a freelancer and you’re on the hook for roughly $10,000 to $12,000 in federal taxes alone before any state hit, split across two buckets: self-employment tax and income tax.

Someone who earned $100,000 as an employee and switched to freelancing at the same gross income suddenly owes an extra $14,130 in self-employment tax alone. That shortfall is what lands in April and ruins your week.

How Much to Set Aside to Avoid Tax Liability Shock

Pick a set-aside percentage and follow it without exception. That’s the most practical move you can make this week.

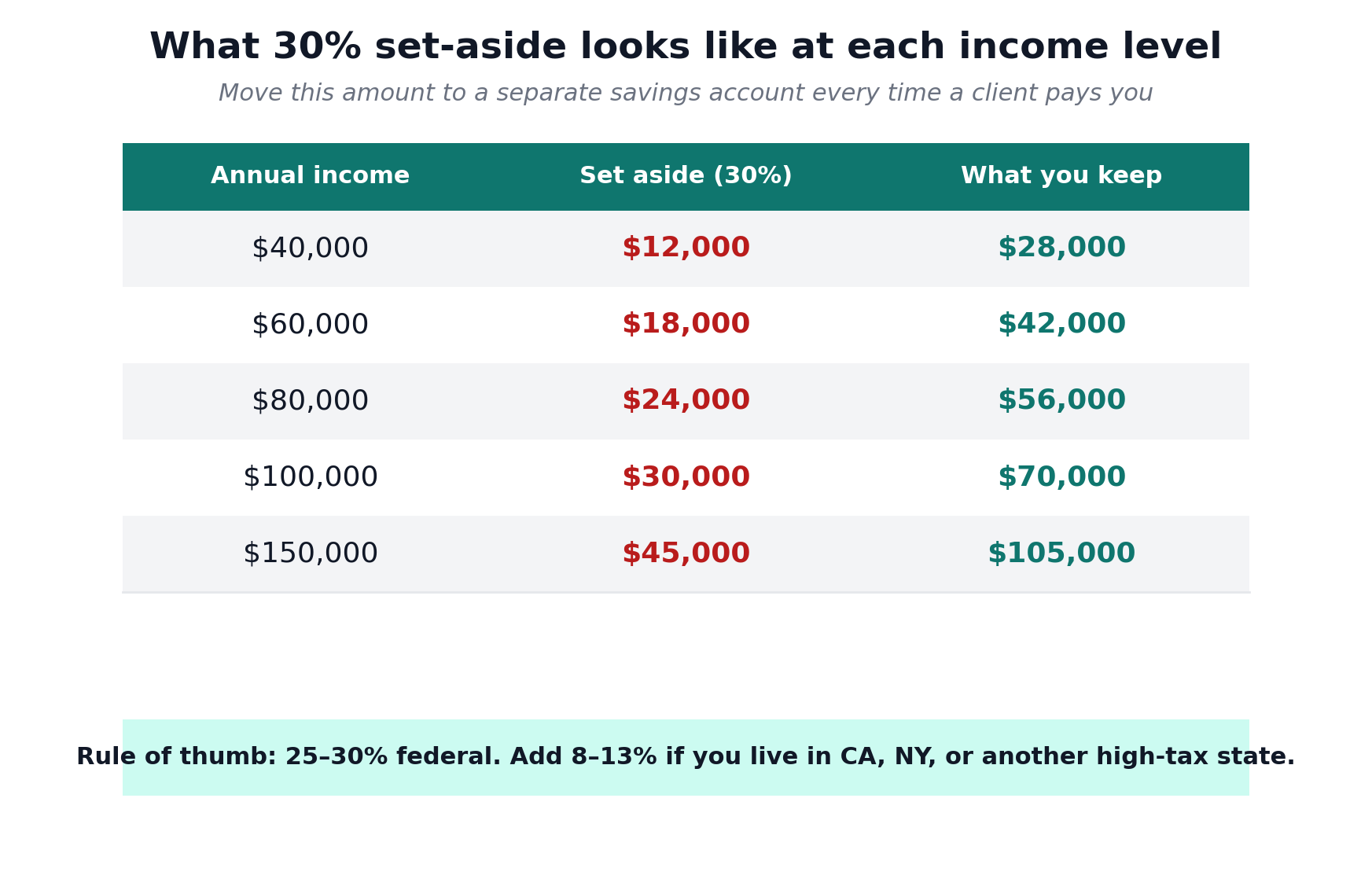

Set aside 25 to 30% of gross self-employment income for federal taxes. This covers self-employment tax at roughly 15.3%, plus federal income tax, which varies by bracket. State taxes add more on top. California, New York, and other high-tax states will want an extra 8 to 13%.

Lower-tax state and lower income bracket? 25% may cover you. California or New York at over $100,000? You may need closer to 40%. When the math is uncertain, set aside more. A tax refund is inconvenient. A tax bill you can’t cover is a crisis.

The mechanics matter. Don’t just note the number. Move the money. Every time a client payment lands in your account, transfer your set-aside percentage to a separate savings account that same day. Label it “Tax Reserve.” Don’t touch it. If your bank supports scheduled transfers, automate it so you never have to think about it.

Treating that money as available because it’s sitting in your account is the most common mistake freelancers make. That money isn’t yours to spend. It belongs to the IRS.

Quarterly Estimated Taxes: What They Are and Why Missing Them Costs You

Most freelancers know taxes are due in April. Fewer know about the four quarterly payment deadlines through the year, and the penalties for missing them.

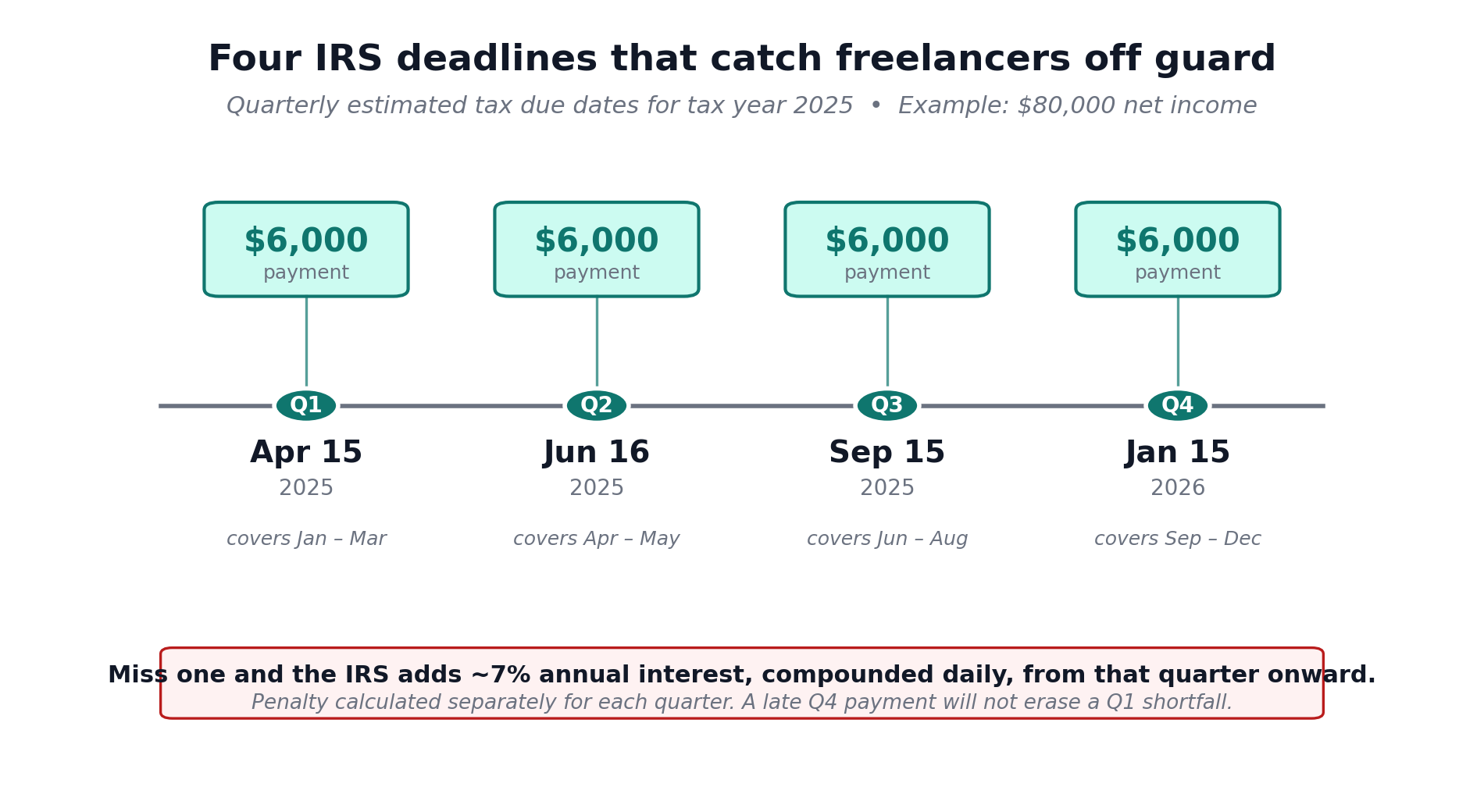

The IRS wants tax paid as income comes in. They don’t wait until April. Quarterly estimated payments are required if you expect to owe $1,000 or more in taxes for the year. The four due dates for 2025 are April 15, June 16, September 15, and January 15, 2026.

Miss a quarterly payment and the IRS charges underpayment penalties from the date you skipped, not from your April filing date. The penalty rate runs at roughly 7% annual interest as of early 2026, compounded daily. For someone owing $40,000 in annual tax who makes no quarterly payments, the penalty bill could top $1,400. That’s on top of what you already owe.

How to Calculate Your Quarterly Payment in 4 Steps

Step 1: Estimate your total net income for the year. If this is your first year freelancing, take your current monthly average and multiply by 12.

Step 2: Multiply your estimated net income by your set-aside percentage. At 30%, $80,000 in income works out to $24,000 in estimated annual taxes.

Step 3: Divide by four. Each quarterly payment in this example comes out to $6,000.

Step 4: Pay on the due dates. Use IRS Direct Pay at IRS.gov/payments, or the Electronic Federal Tax Payment System (EFTPS). Both are free, fast, and trackable. If you prefer paper, send your payment with the Form 1040-ES voucher for each quarter.

| Quarterly Payment | Due Date | Amount (on $80K income) |

|---|---|---|

| Q1 | April 15 | $6,000 |

| Q2 | June 16 | $6,000 |

| Q3 | September 15 | $6,000 |

| Q4 | January 15, 2026 | $6,000 |

The Safe Harbor Rule

If estimating your income feels unreliable, the IRS offers a “safe harbor” approach. You can base your quarterly payments on 100% of the tax shown on your previous year’s return (Line 24 from your prior Form 1040). As long as you pay that amount across the four quarters, the IRS won’t charge underpayment penalties, even if you end up owing more at filing.

For high earners, the threshold shifts. If your prior year adjusted gross income was over $150,000, you need to pay 110% of the prior year’s tax liability to qualify for safe harbor.

When Your Income Is Unpredictable

If your income swings month to month, fixed-quarter payments can leave you over- or under-paying. The IRS allows you to use the annualized income installment method (Form 2210, Schedule AI), which adjusts each quarterly payment to match what you actually earned that period. It takes more record-keeping. It can also cut your overpayment dramatically. Most accounting tools handle the calculation automatically.

Deductions That Reduce Your Bill Before You Pay It

Your taxable income is not your gross income. It’s your gross income after deductions. Most freelancers claim a small slice of the deductions they qualify for. That means paying tax on money they could have kept. For the full list, see our guide to tax deductions for freelancers.

The average freelancer misses $3,000 to $5,000 in deductions every year. On $10,000 of missed write-offs, you pay roughly $3,000 to $4,000 in tax you should never have paid. Here are the deductions with the biggest impact under current 2025 IRS rules.

1. The Qualified Business Income (QBI) Deduction

This is the most underused deduction available to freelancers. The One Big Beautiful Bill Act of 2025 made the 20% Qualified Business Income deduction under Section 199A permanent. If you operate as a sole proprietor, LLC, or S-corporation, you can deduct up to 20% of your qualified business income.

In practical terms: if you earn $80,000 in net self-employment income and qualify for the full QBI deduction, you deduct $16,000 from your taxable income before income tax is calculated. At a 22% tax bracket, that’s $3,520 you don’t pay.

For 2025, you generally qualify for the full deduction if your taxable income is $197,300 or less as a single filer, or $394,600 or less as a married joint filer. Talk to a tax professional if you’re close to those limits.

2. The Self-Employment Tax Deduction

You can deduct 50% of your self-employment tax from your gross income when calculating your adjusted gross income. This is an above-the-line deduction. You get it whether you itemize or not. On $80,000 of net self-employment income, your SE tax is roughly $11,300. You deduct half ($5,650) from your income before income tax is calculated. At 22%, that saves you $1,243.

3. Home Office Deduction

If you work from home, you can deduct a portion of your rent or mortgage, utilities, and insurance costs. The space must be used regularly and exclusively for business.

You have two methods. The simplified method gives you $5 per square foot up to 300 square feet (maximum $1,500). The regular method applies the actual percentage of your home used for business to your real home expenses. Run both and use whichever gives you the bigger number.

4. Health Insurance Premiums

If you’re self-employed and pay for your own health insurance, you can deduct 100% of premiums for yourself, your spouse, and dependents. This is an above-the-line deduction. For a freelancer paying $600 per month in health insurance, that’s $7,200 a year in deductions. At a 24% tax bracket, that’s $1,728 back in your pocket.

5. Retirement Contributions

Contributions to a Solo 401(k) or SEP-IRA reduce taxable income dollar-for-dollar. A freelancer in the 24% bracket who contributes $30,000 to a Solo 401(k) saves $7,200 in federal income tax for the year.

The Solo 401(k) allows an employee deferral of up to $24,500 for 2026, plus an employer profit-sharing contribution of up to 25% of net self-employment income, with a combined limit of $72,000. A SEP-IRA allows employer-only contributions of up to 25% of net self-employment earnings, with a 2026 cap of $72,000.

6. Vehicle and Mileage

The 2025 standard mileage rate is 70 cents per mile for business use of a vehicle. If you drive to client meetings, pick up supplies, or travel for any business purpose, log the miles. A freelancer who drives 5,000 business miles in a year deducts $3,500. Apps like MileIQ or the built-in mileage tracking in QuickBooks Self-Employed handle this automatically.

7. Business Software and Tools

Every software subscription you use for your work is deductible. Design tools, project management apps, cloud storage, communication platforms, accounting software, website hosting. Keep your receipts in a dedicated folder and reconcile them monthly. Our guide to tracking business expenses without spreadsheets covers the workflow.

8. Professional Development

Courses or continuing education that build new skills or maintain professional licenses are deductible. This covers online courses, books, industry conference attendance, and professional association memberships directly tied to your work.

9. Professional Services

Your accountant’s fees are deductible. Your bookkeeper’s fees are deductible. If you hired a lawyer to review a contract, that’s deductible. If you use a contract template service, that’s deductible too. Most freelancers pay for these things and never claim them.

10. Business Meals

If you take a client out for coffee, lunch, or dinner to discuss business, you can deduct 50% of the cost. Keep the receipt and write a brief note on the back: who you met, the date, and what you discussed. Entertainment expenses like sports tickets are no longer deductible under current IRS rules, even if a client is in the seat next to you.

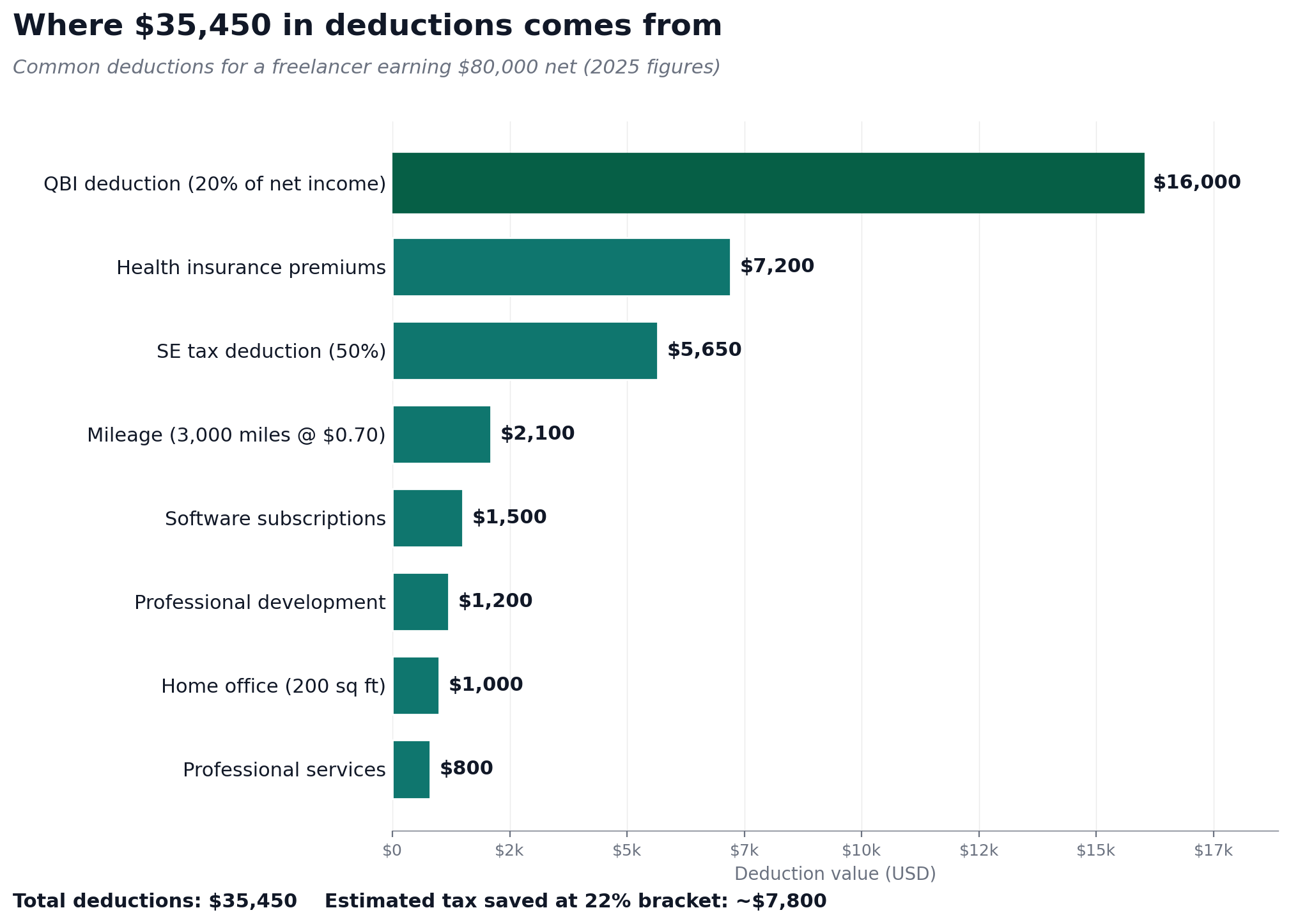

What These Deductions Are Worth in Real Numbers

A freelancer earning $80,000 who claims the following deductions:

| Deduction | Estimated Amount |

|---|---|

| QBI deduction (20% of net income) | $16,000 |

| SE tax deduction (50%) | $5,650 |

| Home office (200 sq ft simplified) | $1,000 |

| Health insurance premiums | $7,200 |

| Software subscriptions | $1,500 |

| Professional development | $1,200 |

| Mileage (3,000 miles at $0.70) | $2,100 |

| Professional services | $800 |

| Total deductions | $35,450 |

Those deductions cut taxable income to roughly $44,550. At a 22% marginal rate, you save about $7,800 compared to claiming nothing.

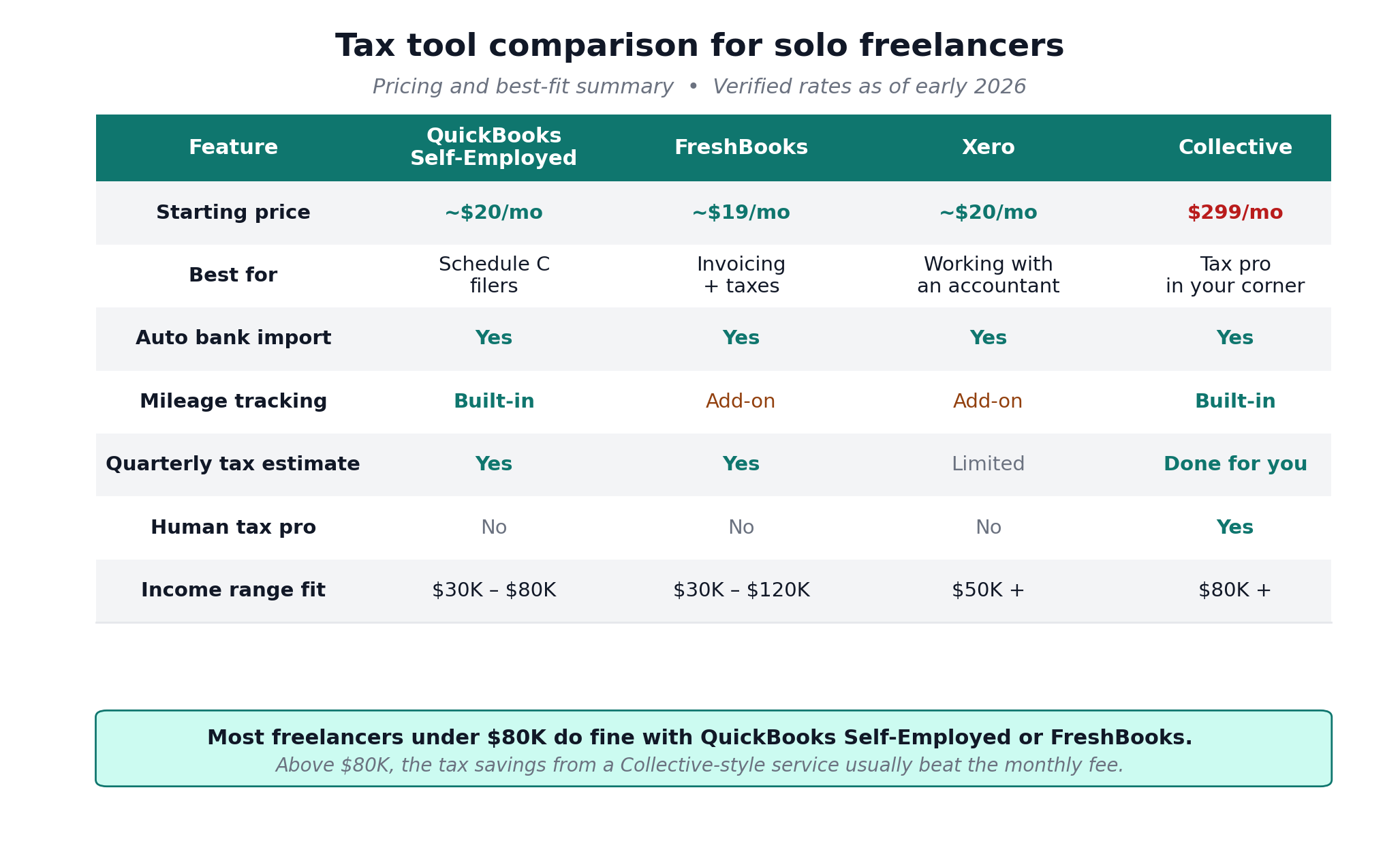

Tools That Do the Tax Math for You

Doing this by hand works, but it’s slow and easy to mess up. The right tool pulls your bank transactions automatically, categorizes expenses, estimates your quarterly payments, and tells you what you owe before April surprises you. For a wider comparison, see our roundup of the best accounting software for freelancers.

QuickBooks Self-Employed

Best for: Freelancers who want a tool built specifically for their tax situation.

QuickBooks Self-Employed was built for people who file a Schedule C. Connect your bank account and it imports and categorizes transactions automatically. The mileage tracker runs in the background on your phone. The tax estimate feature calculates your quarterly payment based on income to date and shows a running total of what you’ll owe. At filing time, the TurboTax integration moves your Schedule C data straight across.

Pricing sits at around $20 per month.

FreshBooks

Best for: Freelancers who want invoicing, expense tracking, and tax management in one place.

FreshBooks covers the full picture: invoicing, expense categorization, cash flow, and tax liability in one dashboard. The expense import connects to your bank and flags deductible items. The tax summary report shows your income, expenses, and estimated liability at a glance. Where FreshBooks pulls ahead of QuickBooks Self-Employed is on the invoicing side. If you’re chasing payments and juggling clients, FreshBooks does both jobs. We compare it against the rest in our best invoicing software for freelancers review.

Pricing starts at around $19 per month, with most freelancers on the Plus plan at around $33 per month.

Xero

Best for: Freelancers who work with a bookkeeper or accountant, or anyone who needs professional-grade reporting.

Xero is the tool accountants usually recommend, because it’s built for their workflow. Unlimited users on every plan means your bookkeeper and accountant can both have access at no extra cost. The tax reports are detailed and export cleanly for professional filing. The learning curve is steeper than FreshBooks. Expect to spend time getting oriented, or lean on your accountant to set it up.

Pricing starts at $20 per month, though most freelancers need the $47 per month Growing plan.

Collective

Best for: Freelancers who want human tax professionals in their corner, not just software.

Collective combines accounting software with access to real tax professionals who review your situation, plan your quarterly payments, and optimize your deductions. They also handle S-Corporation elections for eligible freelancers, which can cut self-employment tax meaningfully once you earn above roughly $60,000 to $80,000 per year.

Pricing starts at $299 per month, which makes most sense for freelancers earning $80,000 or more annually, where the tax savings from professional planning often beat the cost.

Should You Hire a Tax Professional?

Software handles the mechanics well. A good tax professional looks at your specific situation and finds strategies the software won’t flag.

If you’re earning over $50,000 a year, a CPA or enrolled agent who specializes in self-employed clients will usually save you more than they cost. They know the QBI deduction phase-outs, the S-Corporation election threshold, the retirement account strategies, and the documentation requirements that protect you if you’re ever audited.

The cost for a freelancer tax return with a CPA usually runs $300 to $700 depending on complexity. On a $100,000 income, a professional who saves you an extra $2,000 through proper deduction planning has paid for themselves three times over.

If your situation is straightforward, software plus this guide gets the job done. If your income keeps climbing, if you have clients in several states, or if you’re weighing an S-Corporation election, a professional conversation pays for itself fast. Pair it with a system to manage feast-and-famine cash flow and you stop reacting to your money.

Get Your Free Tax Deduction Checklist

I’ve put together a 47-item Tax Deduction Checklist that covers every deduction freelancers commonly miss. The obvious ones like home office and mileage are in there. So are the smaller ones that quietly add up. Print it out and go through it before you file. Better yet, go through it in January so you’re tracking the right things all year.

Frequently Asked Questions

When should I make my first quarterly payment?

If you expect to owe $1,000 or more in taxes for the year, your first payment is due April 15. If you’re just starting out and your Q1 income was modest, work out your estimate carefully. A low first-quarter payment won’t trigger penalties as long as your total payments meet the safe harbor threshold by year-end.

What if I miss a quarterly deadline?

Pay as soon as you realize it. The IRS charges interest from the missed quarterly deadline at the federal short-term rate plus 3 percentage points. That works out to roughly 7% annual interest as of early 2026, compounded daily on the underpaid amount. The longer you wait, the more it costs, and the penalty is calculated separately for each quarter, so a big Q4 payment doesn’t erase a Q1 shortfall. Paying late still beats not paying at all.

Can I deduct my home office if I rent?

Yes. You don’t need to own your home to claim the home office deduction. Use the simplified method at $5 per square foot up to 300 square feet, or work out the actual percentage of rent and utilities tied to the workspace. The only requirement is that the space is used regularly and exclusively for business.

What if my income is wildly different every month?

Use the annualized income installment method (Form 2210, Schedule AI), which adjusts each quarterly payment based on actual income earned during that period. Most accounting tools can calculate this for you. Otherwise, take last year’s total tax bill as your baseline and split it across four equal payments.

Should I hire an accountant or just use software?

For a straightforward freelance situation with a single income stream and standard expenses, good software handles the job. Once you earn above $60,000, work in multiple states, look at an S-Corporation election, or make sizable retirement contributions, a tax professional earns their fee quickly. Many freelancers use software all year and pay an accountant just to file the return and review their strategy.

What records should I keep and for how long?

Keep all receipts, invoices, bank statements, and mileage logs. As a general rule, keep records for three years from the filing date, and seven years if you claim a loss. A dedicated folder per year, physical or digital, makes this painless if you maintain it through the year.

What is the QBI deduction and do I qualify?

The Qualified Business Income deduction allows most sole proprietors, LLCs, and S-corporations to deduct 20% of net business income from their federal taxable income. The One Big Beautiful Bill Act of 2025 made this deduction permanent. For 2025, the full deduction is available if your taxable income is below $197,300 as a single filer. Most freelancers earning under that threshold qualify automatically.

Start Here

Tax planning isn’t something you do in April. You set it up once and forget about it. Once those systems exist, they barely need your attention. You can focus on client work.

Open a separate savings account today. Transfer 28 to 30% of your last client payment into it right now. That’s your first tax reserve. Mark the four quarterly due dates in your calendar. Pick one of the tools above and start tracking income and expenses from this week.

Put in 30 minutes now and you’ll never sit in front of an $8,000 surprise in April again.

Tax rules change. The figures in this guide reflect 2025 IRS guidelines. Verify current rates and limits at IRS.gov or with a qualified tax professional before filing. This guide is for informational purposes and does not constitute tax advice.

About the author

Gareth is an entrepreneur based in Dubai and the founder of Freelancer Profit. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide here is researched from real user reviews, official documentation, and expert sources.